Structure of Futures Markets

A Q&A rundown of futures market basics — open interest, margin calls, stop vs. limit orders, and how hedgers and speculators get taxed differently.

Quick quizzes first

Q1. Open interest vs. trading volume — what’s the difference?

Open interest at a given moment is the total number of long contracts (or equivalently, short contracts) still sitting out there, unclosed. Trading volume over some period is just the total number of contracts that changed hands during that window. One is a stock (snapshot), the other is a flow (over time).

Q2. Local vs. futures commission merchant?

A futures commission merchant trades for clients and pockets a commission. A local trades on their own account.

Q3. July silver futures, short at $27.20/oz on the NYCE. Contract = 5,000 oz. Initial margin $4,000, maintenance margin $3,000. What price move triggers a margin call? What if you don’t meet it?

You’re short, so a margin call happens when you’ve lost $1,000. That's $1,000 / 5,000 = $0.20 per ounce of upward move. So if silver climbs to $27.40/oz, the call goes out. If you don’t meet it, the broker closes you out. Done.

Q4. Long crude oil futures (May 2014 contract) opened in Sep 2013, closed in Mar 2014. Open at $88.30/barrel, close at $90.50, and at end of Dec 2013 it was $89.10. Contract = 1,000 barrels. Profit? How is it taxed (a) as a hedger, (b) as a speculator? Year ends Dec 31.

Total profit: $(90.50 - 88.30) \times 1{,}000 = \$2{,}200$.

Of that, $(89.10 - 88.30) \times 1{,}000 = \$800$ was actually realized day by day from Sep through Dec 2013, and the remaining $(90.50 - 89.10) \times 1{,}000 = $1{,}400$ between January and March 2014.

- Hedger: the whole $2,200 gets taxed in 2014.

- Speculator: $800 in 2013, $1,400 in 2014. Mark-to-market all the way.

Q5. What’s a stop order to sell at $2? When would you use it? Same question for a limit order to sell at $2.

A stop order to sell at $2 says: once the market touches $2 or lower, sell at the best available price. You use it to cap losses on an existing long position.

A limit order to sell at $2 says: only sell at $2 or above. You use it to tell the broker “go short, but only if the price gets nice enough.”

Q6. Margin account at a clearing house vs. margin account at a broker — what’s different?

A clearing-house margin account is marked to market daily, and clearing-house members have to top it back up to the set level every single day. No grace.

A broker-managed margin account is also marked to market daily, but you don’t have to top it up every day. You only top it up — back to the initial margin — when the balance dips below the maintenance margin. (Maintenance is usually about 75% of initial.)

Q7. How do prices get quoted in the FX futures market vs. the FX spot market vs. the FX forward market?

In the futures market: USD per unit of foreign currency. For the British pound, euro, Australian dollar, and New Zealand dollar, spot and forward are also quoted that way. For most other currencies, though, spot and forward go the other direction — units of foreign currency per USD.

OK, on to the actual material.

Opening and closing futures positions

Futures contracts are organized around the delivery month. So when you place an order, it’s not “N contracts for N months from now” — it’s “N contracts for the month of August” (or whatever). That’s the framing.

But wait — does that mean the contract actually rides all the way to maturity and the goods physically show up in the delivery month?

Nope. Almost nobody holds to delivery. Basically everyone closes out their position before then.

You close a position by taking the opposite side of the one you opened. Say you went long 5 August corn contracts. Sometime before the end of July, you sell 5 August corn contracts and you’re flat.

How rare is actual delivery? Rare enough that traders forget the delivery process even exists. (Funny old story from Korea, back when derivatives were still kind of new — some company traded futures on 100,000 tons of oil, and one day the phone rings:

“Hi! You traded oil, right? This is Incheon Port. Come pick it up.”

lol lol lol lol lol like for real lol. Apparently it literally showed up at the dock.)

Contract specs

When you write a futures contract, the exchange has to nail down a bunch of things up front:

- the underlying asset

- the contract size

- the delivery date

- the delivery location

…and so on. One thing worth flagging — for things like the deliverable grade, or the delivery location, the short gets to make the call. (Yeah, the seller. Hold that thought.)

1. Underlying asset. For commodities like oranges or corn, the contract has grades. For oranges, quality is standardized by sugar content. Higher quality, higher price — obvious.

2. Delivery terms. The exchange specifies where delivery can happen, and for each commodity there’s a list of approved or recognized locations. For oranges, the recognized warehouses are in Florida, New Jersey, and Delaware. And like I said — when there’s a choice to make, the short picks.

3. Daily price movement limits & position limits.

Most exchanges set a daily price-move limit on futures. Meaning: in a single day, the price can only move by that much. If the futures price hits the upper or lower limit, trading in that contract halts for the day.

Why? To stop speculators from artificially yanking the price around. (Of course, sometimes a big move is just genuine market motion, not manipulation, so the exchange can also step in and change the limit. Whether the limit system is actually good for the market is a debate that will not end.)

The position limit is the cap on how many contracts a single speculator can hold. Same idea — stop any one person from having outsized influence on the market.

Futures prices converge to spot

As the delivery month approaches, the futures price drifts toward the spot price. Honestly — isn’t this obvious?

If futures > spot near delivery: people pile into spot (spot goes up) and sell futures (futures comes down). The two close in.

If futures < spot near delivery: people sell what they own at spot (spot comes down) and buy futures (futures goes up). Same convergence.

(This is just the law of one price wearing different clothes.)

How margin accounts actually work

OK, what’s a margin? Easiest way to think about it: collateral you put down before you sit at the table.

Like at a poker table — you stack chips in front of you before you play. (How sketchy would it be to play with someone who hasn’t shown they have any chips?) Same vibe in futures. Before you trade, you put up margin.

Every time you lose money, it gets pulled out of that margin account. And if your balance dips below a certain pre-set floor, you get a phone call:

“Hi, sorry, could you top up your margin account please?”

That call is the margin call. The whole system exists to prevent the “lol I have no money” outcome (a.k.a. default) when everything is said and done.

So step by step: when you sign up to trade through a broker, the broker makes you deposit funds in a margin account. The amount you have to put down at contract time is the initial margin.

Once you’re in, gains and losses get settled and recorded every single day. This is daily settlement (marking to market). It’s basically like the contract gets closed at the end of every day and re-opened the next morning at the new price.

Day after day, if your balance goes above the initial margin, you can withdraw the excess any time. But you can’t just let the balance bleed to zero — you have to stay above the maintenance margin, which is set a bit below the initial. If you fall through it, that’s when the margin call I mentioned hits, and you have to deposit a variation margin to bring the account back up to the initial level.

Maintenance is typically about 75% of initial. The more volatile the underlying, the higher they push the maintenance level.

What if you ignore the call? The broker liquidates your position. Bye~

Also — margin doesn’t have to be cash. You can deposit securities with the broker instead. Government bonds usually count for 90% of face value. Stocks vary, but figure roughly 50% of current market price.

Because of this whole margin system, exchange trading basically has no credit risk — unlike OTC. So does that mean OTC just runs on pure trust with nothing in place?

No no no no — not quite. Bilateral OTC contracts often involve collateral between the two parties. And before 2008, sure, you could think of OTC as essentially private bilateral deals. But after getting torched in 2008, everyone got jumpy, and now there’s also a clearing house whose job is to take all the day’s trades, sort them, and net out each party’s position. (Exchanges have always had this. OTC caught up the hard way.)

Orders

Market order.

Literally what the name says — buy or sell at whatever the market is doing. You call the broker, “I want to buy some of that~”

“Sure, $90.5 right now.” Done.

A few days later someone else calls: “I’d like to sell some of that~”

“You can sell it at $90 right now!”

The middleman pockets the $0.50 spread and the trade goes off at $90. That’s the mechanism.

(One catch: if your order is big, this falls apart. The quoted bid/ask is only good up to a certain size.)

Limit order.

You name a price. Say a long-side investor sets a limit price of $30. The order will only execute at $30 or below — i.e., only in the direction that’s good for you.

Stop order (or stop-buy order).

This one is the weird one — it goes against market logic. “Buy when the price goes up, sell when the price goes down.” Why would you do that? Because someone who’s short wants to cap their losses. The whole point isn’t profit — it’s damage control. So you trade in the unfavorable direction on purpose.

Stop-limit order.

Mash a stop and a limit together. When the stop price (or worse) is hit, the order instantly converts into a limit order. Bam.

cf.) When the two limits are the same price, it’s called a stop-and-limit order. heh.

A few more term definitions

Open interest. Number of outstanding longs (= number of outstanding shorts) — basically how many contracts are alive in the market right now.

Trading volume. Number of contracts that traded that day.

Settlement price. The price at which trades happened right before the close.

Normal market. Longer maturity → higher futures price. e.g., gold, live cattle.

Inverted market. Longer maturity → lower futures price (a.k.a. backwardation). e.g., wheat.

(In real life, of course, things don’t sort cleanly into one or the other. Plenty of contracts show both patterns at different parts of the curve, so good luck generalizing. T_T lol.)

Prob 2.11

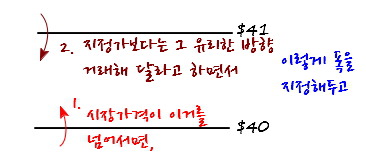

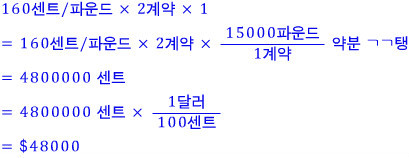

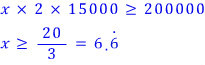

Investor goes long a July orange juice futures contract. Contract size = 15,000 lbs. Current futures price = 160 cents/lb. Initial margin $6,000/contract, maintenance $4,500/contract. At what price is there a margin call? And what does it take to withdraw $2,000 from the margin account?

This person has 2 contracts, so initial margin is $12,000 and maintenance is $9,000. They’re long, so a price drop is a loss.

That’s not the interesting bit. The interesting bit: from $12,000 down to $9,000 is a $3,000 loss → margin call. So what futures price gives a $3,000 loss?

Meaning: if the futures price drops by more than 10 cents per pound (wait — sorry, I mean a 10-cent drop on the implied per-contract math), the call goes out.

To pull $2,000 out? You need a $2,000 profit first.

A move of about 6.667 cents — i.e., the price climbing from 160 to 166.67 — and you can withdraw the cash.

Prob 2.13

Difference between a market-if-touched (MIT) order and a stop order?

A stop order (a.k.a. stop-loss order) names a specific price. If the market falls and hits that price → sell. If the market rises and hits that price → buy.

The reason it doesn’t follow normal market logic is, again, this isn’t about making money — it’s about not bleeding too much.

An MIT order: once a trade prints at the specified price or better, your order goes off at the best available market price. This one does follow market logic — you’re trying to do well, not just contain a loss.

Prob 2.14

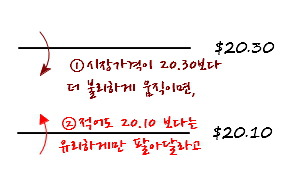

Describe a stop-limit order to sell at 20.30 with a limit price of 20.10.

Prob 2.15

End of trading. A clearing-house member is long 100 contracts and the settlement price is $50,000/contract. Initial margin is $2,000/contract. Next day, the member takes on the clearing responsibility for an additional 20 long contracts. That day, the futures price is $51,000/contract and the settlement price closes at $50,200/contract. How much margin does the member have to top up?

Easiest way is to think from the investor’s side and then flip it.

Daily settlement on the original 100: $(50{,}200 - 50{,}000) \times 100 = +\$20{,}000$ in profit.

The 20 new contracts that the member is now clearing — from the member’s perspective they’re taking on a long, so from the investor side it’s like clearing a short. Equivalent: the investor is opening a fresh long on 20 contracts.

So the investor pays initial margin: $2{,}000 \times 20 = \$40{,}000$ (−40,000).

That long was put on at $51,000 but the day closed at $50,200. Long at a loss:

$(51{,}000 - 50{,}200) \times 20 = \$16{,}000$ loss (−16,000).

Net for the investor: $+20{,}000 - 40{,}000 - 16{,}000 = -\$36{,}000$. The investor has to cough up $36,000.

From the clearing-house member’s perspective, that $36,000 is what comes *in* — meaning the member needs to deposit $36,000 of additional margin.

Prob 2.16

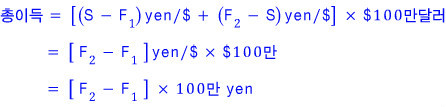

July 1, 2013: a Japanese company enters a forward contract to buy $1,000,000 on January 1, 2014. September 1, 2013: the same company enters a forward to *sell* $1,000,000 on July 1, 2014.

Describe the P&L of this strategy (in dollar terms) as a function of how the forward exchange rate moves from those two reference points.

First, let’s figure out which direction of move in the ¥/$ exchange rate is good for us and which is bad.

Contract #1 is a contract to buy dollars. We’re told to think in dollar terms, so I’ll work in ¥/$.

You can read ¥/$ as "the price of a dollar." High ¥/$ → dollar is expensive. Low ¥/$ → dollar is cheap.

If you’re the one buying dollars, which way do you want the rate to move? You want to lock in dollars when the spot rate is high — i.e., a high ¥/$ on the spot side is good for the person who already locked in a forward.

So: when the spot rate is high but the forward rate you locked in is low, that gap is your profit.

(“Phew, glad I locked that in! Spot is brutal right now!”)

(Same thing in risk terms: if you’re planning to buy dollars in a few months, the risk is the dollar getting too expensive — i.e., ¥/$ going up. To hedge that, you lock in a forward. The moment you feel “thank god I locked the forward” is exactly when F < S.)

So profit from contract #1 is $(S - F) \times \$1{,}000{,}000$.

Contract #2 is a contract to sell $1,000,000 — meaning you receive yen. Higher yen value is what you want, so you want ¥/$ to go down — dollar weak.

Then locking in a sale at an F that’s higher than the eventual S is the win.

(Risk-side again: if you’re planning to sell dollars (= buy yen) in a few months, your risk is the dollar falling too far / the yen rising too far. To block that, you want to lock F in high. Then when S has dropped low, you’re saying “phew, glad I locked the forward!”)

So profit from contract #2 is $(F - S) \times \$1{,}000{,}000$.

Total:

Prob 2.33

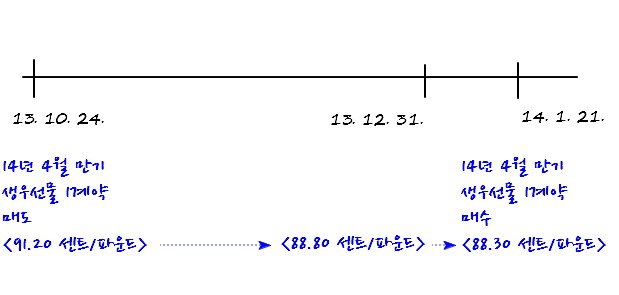

A company shorts 1 live cattle futures contract maturing April 2014, on October 24, 2013, and closes the position on January 21, 2014.

- Open price: 91.20 cents/lb

- Close price: 88.30 cents/lb

- End-of-2013 price: 88.80 cents/lb

- Contract size: 40,000 lbs

Profit? And how is it taxed (a) as a hedger, (b) as a speculator?

Picture it:

Profit: $(91.20 - 88.30) \text{ cents/lb} \times 40{,}000 \text{ lbs} = 116{,}000 \text{ cents} = \$1{,}160$.

If it’s a hedger, the whole $1,160 is taxed in 2014 (recorded as $0 profit for 2013).

If it’s a speculator:

- 2013: tax on $(91.20 - 88.80) \times 40{,}000$

- 2014: tax on $(88.80 - 88.30) \times 40{,}000$

Each year gets its own slice. Accounting follows the same principle.

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.