Determining Forward and Futures Prices

A quiz-style rundown of how forward and futures prices actually work — short selling, convenience yield, cost of carry, and why copper isn't gold.

quiz 1.

- When an investor short sells a stock, what actually happens?

Your broker borrows shares from another customer’s account and sells them on your behalf. To close out, you have to buy the shares back later.

The broker then puts the shares back into the account they were borrowed from.

While you’re short, you have to pay the broker any dividends or other income the stock pays. The broker forwards that to the customer whose shares were borrowed.

Sometimes the broker just can’t borrow the shares. In that case, you get force-closed — you have to buy back even at a price you don’t like.

quiz 2.

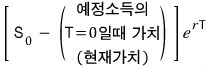

- What’s the difference between a forward price and the value of a forward contract?

The forward price today is the price you’ve agreed to buy or sell the asset at, at some future date.

The moment you enter the contract, the value of the contract is 0.

As time passes and the underlying moves around, the value drifts into positive (+) or negative (−) territory.

quiz 3.

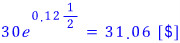

You want to enter a 6-month forward on a non-dividend-paying stock. The current price is $30 and the risk-free rate is 12% per annum, continuously compounded.

What’s the forward price?

quiz 4.

Stock index is at 350. Continuously compounded risk-free rate is 8% per annum, dividend yield on the index is 4% per annum. What’s the price of a 4-month futures contract?

quiz 5.

- The futures price of copper can’t be cleanly pinned down from the spot price the way gold’s can. Why?

Gold is an investment asset. If gold futures are priced too high, investors can sell futures and buy more gold to lock in a profit. If futures are priced too low, they can sell some of their gold and buy futures.

Copper is a consumption asset. If copper futures get too expensive, sure — you can buy copper and sell futures. But if futures get too cheap, the trick of “sell your copper and buy futures” doesn’t really work, because most people don’t sit on a pile of copper. So copper futures have an upper bound, but no real lower bound.

quiz 6.

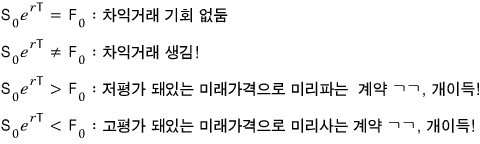

- Explain convenience yield and cost of carry. And the relationship between futures price, spot price, convenience yield, and cost of carry.

Convenience yield is the perk you get from actually owning the commodity — a perk that someone holding a long futures contract on it doesn’t get.

Cost of carry is interest cost + storage cost − any income the asset throws off.

If F is the futures price and S is the spot, then:

(c: cost of carry, y: convenience yield)

quiz 7.

- Why can a foreign currency be treated as an asset that pays a known yield?

A foreign currency earns interest at the foreign risk-free rate — but the interest is paid in that foreign currency. So when you express your return in your home currency, it shows up as a percentage of the foreign-currency value. Which means: it has the structure of a known yield. Done.

Forwards are way easier to price than futures because there’s no daily settlement messing things up. So the relationship between forward price and spot price is pretty clean to learn.

But — futures prices tend to converge to forward prices as maturity approaches.

So my plan: nail down forward pricing first, then carry that over to futures pricing. Then learn how forward and spot prices relate. Then on to the next chapter — let’s go!!!

- Short selling:

Selling securities you don’t own. <Doesn’t work for every investment asset — only some.>

Ex.

In April, an investor short sells 500 shares at $120. In July, the price has dropped to $100, so they close the short by buying 500 shares back. In May, the stock paid a $1/share dividend.

April: receive 500 × $120 = $60,000 from the short sale. May: pay 500 × $1 = $500 to cover the dividend. July: pay 500 × $100 = $50,000 to close.

Net profit: $9,500.

<Assuming no fee for borrowing the shares (T_T)>

OK so let’s see how the price of a “forward contract,” the supposedly-easy one, actually gets determined.

A few assumptions first:

- No transaction costs.

- Same tax rate on all net income.

- Borrowing rate = lending rate = the risk-free rate.

- Arbitrage opportunities get exploited.

1 through 3 are the “make the model dead simple” conditions. The way I think of it: the model gets built first under these, then later we relax them one at a time to make it more realistic.

Condition 4 is more of a “rip out by the roots” assumption — no arbitrage opportunity is just sitting there ignored. In real life, humans are emotional creatures more than rational ones… and people say even supercomputers don’t always act rationally… but, you know, we’re ignoring all that. heh

OK, let’s price a forward contract.

Which one?

The easiest possible one — a forward on an investment asset that pays no income in between. First!!!

Like a non-dividend-paying stock, or a zero-coupon bond.

Honestly we kind of did this earlier, so I’m not totally sure why it’s showing up again here (T_T)

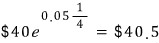

- Ex. Suppose the forward price to buy a non-dividend-paying stock 3 months from now is $43, and the current stock price is $40. What now?

The future value of $40 in 3 months is $40 · exp(0.05 × 0.25) = $40.5.

So the forward is overpriced.

What do we do? We borrow $40, buy the stock, and enter a forward to sell at $43.

3 months later, we get $43,

pay back the loan, and pocket a $2.5 profit. Easy.

What if the forward price were $39 instead?

Borrow shares and short them.

Enter a long forward at $39.

3 months later, buy at $39 via the forward, hand the shares back — profit of $40 − $39 = $1.

But wait — if instead we grow the $40 at the 5% risk-free rate for 3 months and *then* buy back the stock at $39 to return it, we get $1.5 of profit. That's better than $1!

So basically — whether the forward price is greater or less than

“the future value of the current asset price at the contract maturity”

decides whether the arbitrage move is to buy or to short sell.

So,

That’s the conclusion. Right?

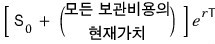

Now — instead of zero-coupon bonds, let’s think about coupon bonds.

What happens when the asset throws off coupons during the holding period?

Suppose there’s a coupon bond, a forward on it matures in September, and there’s a $40 interest payment 4 months from now.

(4-month risk-free rate: 3% per annum. 9-month risk-free rate: 4% per annum.)

The forward price quoted is 910. The bond is currently trading at 900. What strategy?

Spoiler: we want to buy the asset and sell the forward.

Borrow 900, buy the asset.

But $40 comes in 4 months later, right?

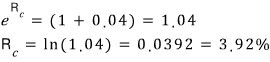

PV of that $40 = 40 · exp(−0.03 × (1/3)) = 39.6.

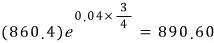

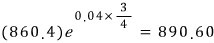

Net that 39.6 against the loan and treat it like we only ever borrowed 900 − 39.6 = 860.4.

Then the amount owed 9 months out is

and we sell the asset via the forward for 910.

Yay — 910 − 886.6 = 23.4 in arbitrage profit!!!

Putting it in one equation:

If this is bigger than the forward price → short sell. If this is smaller than the forward price → buy.

That’s the rule.

Let’s also do the case where the forward price is less than 886.6. Say it’s 870.

Borrow the asset and sell it.

The $40 coming in 4 months is worth 39.6 in PV — treat it as already returned. Enter a long forward to buy at 870 in 9 months. Grow the remaining 860.4 at the risk-free rate for 9 months.

After 9 months that money has grown to

Use 870 of it to buy the stock back via the forward, and the remaining 886.6 − 870 = 16.6 is yours. yay~

Now what about the case where, instead of a fixed income from holding the asset, we get a fixed percentage?

A forward on an asset that pays out 2% of the asset price once over 6 months. Current price S = $25, continuously compounded risk-free rate 10%, forward price quoted at $30. What now?

2% over 6 months = 4% per year. 4% paid once a year — what does that come out to as a continuously compounded rate?

(Converting to continuously compounded basis right now)

So actually,

we can think of this much as already “existing right now,” right?

Sub it into the formula from earlier:

which can also be written as

But hidden in here is the implicit assumption that “the thing being multiplied in the exponent is the same S on both sides.” That is, because the income flowing in (some number) is proportional to S.

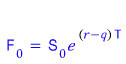

So under the “known yield” assumption, the forward price packages up a little more cleanly:

(q is that percentage). Tidy.

But honestly, the underlying principle is

— that’s the whole thing. To me this version of the formula is the more important one.

By the same logic, for a stock index:

(d must be dividend)

Same exact reasoning as above, so… no need to re-derive it.

Quick taste of something.

Forward vs futures.

Theoretically, a forward contract and a futures contract with the same delivery date have the same price.

But in practice, they don’t. Why?

Because of interest rate uncertainty.

If the underlying asset price S has a positive (+) correlation with interest rates, futures price > forward price by a hair.

If the correlation is negative (−), futures price < forward price by a hair.

- But why????????????

Daily settlement.

Suppose the correlation is positive and S is rising.

With futures, that gain shows up immediately, drip drip drip, through daily settlement.

But if S going up means r going up too, then the gains we just pocketed early get to grow at a now-higher r.

From the buyer’s perspective, that’s even sweeter than if we hadn’t accounted for it. So from the seller’s perspective, they can charge a slightly higher price up front. Which means futures > forward. OK?

Conversely, if the price is falling — even though forward and futures both lose the same money, futures still feel a bit better because the small interest accruing inside the margin account kind of softens the blow. Like it’s quietly compensating you for some of the loss. Right!! OK.

That said — even with all that, futures and forwards with short maturities are basically identical in theory. Because we’ve already left out taxes, transaction costs, margin accounts, etc. from the model anyway…

So for now, futures ≒ forward!

(There’s one product where this approximation falls apart pretty badly — Eurodollar futures — and we’ll get to that next chapter.)

Currency forward and futures contracts.

Notation first.

S: the dollar spot price of one unit of foreign currency. F: the dollar forward (or futures) price of one unit of foreign currency.

(→ Since we’re quoting one unit of foreign currency, this is the American convention. So it’s $/¥, not the ¥/$ you’d see from, say, a Korean perspective.)

Foreign currency holders earn interest at the foreign risk-free rate. We define

as the foreign risk-free rate over period T, continuously compounded (the f is for foreign), and r as the domestic risk-free rate. ok.

Here we go!

So now we hit FX, and just like electromagnetism has Maxwell’s equations and classical mechanics has F = ma, FX has — interest rate parity.

This is the equation, and it falls right out of an embarrassingly simple principle.

(Same exact principle we used way up there! — no arbitrage opportunities! — right?)

Suppose you hold 1,000 units of foreign currency. You want to convert to dollars after period T.

Approach 1: leave the 1,000 units of foreign currency parked abroad to grow. After period T, that becomes

units of foreign currency. You also lock in a currency futures right now to convert that amount to dollars later.

Since F is dollars per unit of foreign currency, F has units of $/¥. So

has units of $. Good.

Approach 2: convert the 1,000 to dollars right now at spot price S, and grow the dollars at the domestic risk-free rate.

S has units $/¥, multiply by 1,000 units of foreign currency, units come out $.

Yep, units are $. Grow that at the domestic risk-free rate over period T:

These two money games — both starting from 1,000 units of foreign currency — must land in the same place after period T!!!

(If they didn’t, hello arbitrage.)

That is,

heh.

So here too, the moral is the same:

if this holds, an arbitrage opportunity opens up!!!

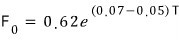

Example 5.6.

Australia’s annual rate is 5%, the US’s is 7%. Spot exchange rate S = $0.62/A$.

But the 2-year forward exchange rate is being quoted at $0.63/A$.

Theoretical F:

= 0.6453

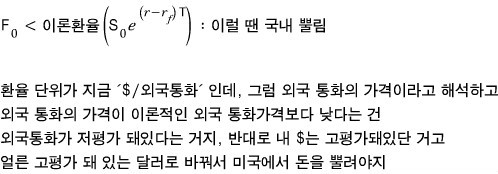

Wait whaaat. The market forward price is lower than the theoretical forward price?!

Time to go to work:

- Enter a long forward — but how much should we buy? Need to calculate.

- Borrow A$1,000 in Australia at 5% for 2 years.

- Convert that to USD at spot — get $620. Park it in the US at 7% for 2 years.

- After 2 years, $620 has grown to 620 · exp(0.07 × 2) = $713.17.

- We need to repay 1000 · exp(0.05 × 2) = A$1,105.17 in Australian dollars. Lock that in at the forward rate of 0.63 — that costs us $696.25.

- So out of $713.17, we hand over $696.25, and the remaining $16.92 is our net profit.

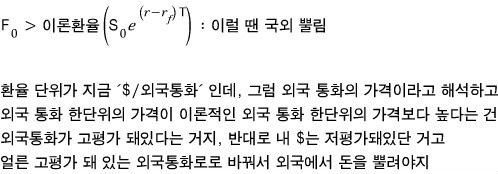

What if the forward price were 0.66 — higher than theoretical??

Underlying principle, again:

OK so what if the forward is 0.66, higher than theoretical?

Forward exchange rate being overvalued means the foreign currency is, relatively speaking, overvalued. So the move is: grow money in the (overvalued) foreign country and bring it back. Arbitrage profit.

- Borrow money where it’s “cheap” — borrow $1,000 in the US.

- Amount owed in 2 years: 1000 · exp(0.07 × 2) = $1,150.27.

- Take the $1,000 to Australia and convert at spot — get A$1,612.9.

- Grow at 5% in Australia, and lock in a short forward at 0.66 to convert back to USD in 2 years.

- After 2 years, A$1,612.9 has grown to (1612.9) · exp(0.05 × 2) = A$1,782.53.

- Convert at the 0.66 forward rate.

- We get (1782.53) × 0.66 = $1,176.47.

- Pay back $1,150.27 — pocket $26.2 in net profit. heh heh heh.

Good good.

Now from currency to real assets!

If currency has ‘interest,’ real assets have things like — for gold — the gold lease rate. Right?

Big gold holders like central banks lend gold out and charge a lease rate on it… (T_T)

Some amount per ounce per period or whatever.

But notice the direction is flipped compared to interest. When you deposit money at a bank, money flows <you → bank>, and interest flows back <you ← bank>.

With the gold lease rate, you give the gold <you → bank>, and also pay the gold lease rate <you → bank>. Both flowing the same way.

Stuff like this gets bundled together as ‘storage costs.’

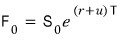

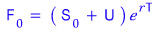

So when we price forward and futures contracts:

For currency it was

For real assets it’s the same principle — except the “interest-like” term flows the other way. So:

That’s how the theoretical forward price comes out.

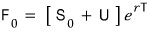

The ‘present value of all storage costs’ is usually written as U, so:

And if storage cost is proportional to S (a known-yield kind of structure):

Yeah, that case shows up too.

Shall we just bang out another example?

Ex. 5.8

Gold futures, 1-year maturity, no intermediate income, storage cost $2 per ounce, spot $1,600, r = 0.05. (Storage costs paid at year-end.)

Futures price quoted at $1,700.

Check theoretical first!

Whoa. Futures at $1,700? Overvalued!

So we sell futures (short the overvalued thing). To do that:

- Borrow $1,600 — owe 1600 · exp(0.05 × 1) = $1,682.03 in a year.

- Use the $1,600 to buy one ounce of gold spot, and enter a short futures.

- A year later, sell at the contracted $1,700, repay the $1,682.03.

- Net so far: 1700 − 1682.03 = $17.97. Right?

- But when we deliver the gold, we also have to pay $2 storage.

- So final net profit: $15.97.

- Done done done.

Done with real assets??

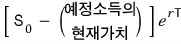

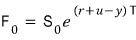

One more thing — and this one’s basically just FYI.

For real assets, holding the thing for 2 years and holding a futures contract that lets you start holding it 2 years from now — these are not the same thing!! Not the same!!!!

Because “real assets have value in being immediately consumable.” The technical phrase: “future availability.”

So sometimes we need to factor in the convenience yield. The idea: contractually owning something later is worth less than physically owning it now. So we have to discount the theoretical value a bit.

We write it as theoretical value × exp(−yT), and the forward / futures price morphs into

If storage cost is proportional to S:

Prob 5.9

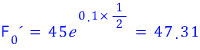

You enter a 1-year long forward on a non-dividend-paying stock. At entry, S = $40, r = 10% per annum continuously compounded.

a) What’s the forward price and the initial value of the contract? b) Six months later, S = $45, r is still 10%. What’s the forward price now and what’s the value of the original contract?

S = 40, so the forward price for the 1-year forward is

Initial value: zero (no-arbitrage).

b) So I’m contractually buying at 44.21 a year out. Six months later — recompute the forward price for the remaining 6 months from the new spot:

Wait — I’m locked in to buy at 44.21, right?

Oh ho! I should take a short position at 47.31 here.

So in 6 months I buy at 44.21 (from the original contract) and sell at 47.31 (from the new short). At maturity that’s a guaranteed gain of 47.31 − 44.21 = 3.1.

PV that — pull it back by half a year:

Done!!

Prob 5.10

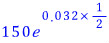

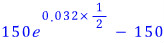

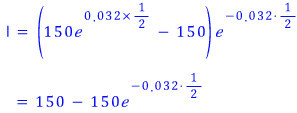

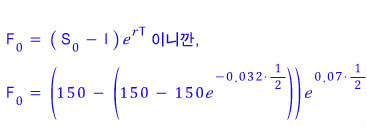

Risk-free rate: 7% per annum continuously compounded. Dividend yield on the stock index: 3.2% per annum. Current index = 150. What’s the futures price 6 months out?

This is the “future income while holding” case.

Idea: PV all the future cash flows that come from holding, sum them up, subtract from S, then take the future value of what’s left. That’s the forward price. Right?

So let’s think about the dividend cash flows.

“Dividend yield is 3.2% continuously compounded” means: the yield from dividends, if you imagine them being paid continuously and compounded continuously, comes out to 3.2%. OK OK.

Hold 150 worth of index, half a year passes, just from dividends:

That’s how much it grows to. The amount that grew due to dividends:

That’s the future amount from dividends. Pull it to present at 3.2% continuously compounded:

Now compute the forward:

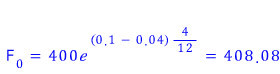

Prob 5.12

Risk-free rate 10% per annum continuously compounded. Stock index dividend yield 4% per annum. Current index 400. Futures price for 4-month delivery is 405.

- What arbitrage opportunity is there?

Need to compute the theoretical forward price for the index.

We already derived the formula above in detail, so this time I’ll just use it. Plug-and-chug.

We had:

^^

Plug in:

So 405 is undervalued! Buy in advance!

“Long forward position” — let’s go!!

4 months later, gain of 408.08 − 405 = 3.08. heh heh heh.

Prob 5.15

Silver spot: $30/ounce. Quarterly storage cost paid in advance: $0.48/ounce. Continuously compounded interest rate, all maturities: 10% per annum.

- What’s the 9-month futures price for silver?

Nice. This one’s clearly asking us to use

OK.

So let’s carefully compute U.

(Storage cost of $0.48 per quarter — and paid in advance.)

Yep, calculated.

Now use the formula. (No need to re-derive — we did all that above.)

Prob 5.17

A company wants to hedge a future foreign currency cash outflow with a forward contract. Assume no FX risk.

If they hedge with a futures contract instead, what risk does the daily settlement process expose them to? What’s the nature of that risk?

Specifically — does the company benefit more from futures or from a forward in each of these cases:

a) Foreign currency value drops sharply during the contract. b) Foreign currency value rises sharply during the contract. c) Foreign currency value first rises, then falls back to its starting point. d) Foreign currency value first falls, then rises back to its starting point.

- (OK so — foreign currency is a future cash outflow, so the natural hedge is a short position locked in now. But “we currently hold the foreign currency” is the framing — so the question becomes whether it ends up overvalued or undervalued during the period… two cases.)

First, the nature of the risk in futures settlement is that — even if the final P&L is the same — whether you make money early or lose money early matters.

Why? Early gains hit your margin account immediately through daily settlement. Anything above the initial margin you can withdraw. And who’s gonna leave that money sitting still? You’re gonna reinvest it elsewhere.

So the actual return on a futures position isn’t really just from the futures — your return on whatever you reinvested those cash flows into gets mixed in too…

Now case a): foreign currency drops during the contract → bad. Early loss. To avoid the loss-getting-amplified-by-reinvestment effect, you’d rather not deal with daily settlement. Answer for a): forward.

Case b): you want the early gains so you can reinvest them. Answer for b): futures.

Same logic for c) and d). Answer for c) is futures, answer for d) is forward. Right?

Look — if d) were futures, you’d take losses early via daily settlement, and then earn interest on a now-depleted base. Versus c), where you bank gains early through daily settlement and then earn interest on a bigger base. The c)-as-futures version is clearly better.

So c) → futures, d) → forward.

And the answer for me is you………………………

Sorry. Terrible joke.

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.