Interest Rate Futures

Working through quiz problems on T-bond accrued interest, conversion factors, Eurodollar futures P&L, convexity adjustments, and duration-based portfolio hedging.

Quiz 1.

A T-bond pays a 7% annual coupon on January 7 and July 7. On a $100 principal, how much interest accrues between July 7, ‘13 and August 9, ‘13? And if it were a corporate bond instead, how much then?

OK so for the T-bond — calendar basis. From July 7 to August 9 is 33 days. From July 7, ‘13 to January 7, ‘14 is 184 days. So:

$$7\% \times \tfrac{1}{2} \times \tfrac{33}{184} = \$0.6277$$For the corporate bond, we use 30/360. July 7 to August 9 → 32 days. July 7 to January 7 → 180 days. So:

$$7\% \times \tfrac{1}{2} \times \tfrac{32}{180} = \$6.222$$Wait, that’s wildly different. Yeah — the day-count convention actually moves the number, that’s the whole point of this chapter.

Quiz 2.

As of January 9, ‘13, a T-bond maturing October 12, ‘20 with a 12% coupon is quoted at 102-07. What’s the cash price?

From October 12, ‘14 to January 9, ‘15: 89 days. From October 12, ‘14 to April 12, ‘15: 182 days. Cash price = quoted price + accrued interest. Quoted price 102-07 means $102 + \tfrac{7}{32} = 102.21875$. So:

$$102.21875 + \tfrac{89}{182} \times 6 = 105.15$$Quiz 3.

What’s the conversion factor of a bond as defined by CME Group, and what’s it for?

The conversion factor is “the quoted price of the bond per $1 of face value as of the first day of the delivery month, computed under the assumption that the interest rate is 6% per annum on a semiannual compounding basis throughout the life of the bond.” When you compute it, you truncate the time to maturity and the time to coupon dates to the nearest 3-month chunk.

It’s used to figure out how much cash the short side of a bond futures contract receives at delivery. If the conversion factor is 1.2345, you get (most recent futures price × 1.2345) + accrued interest.

Quiz 4.

A Eurodollar futures price moves from 96.76 to 96.82. What’s the P&L on someone who bought 2 contracts?

Up 6 bp. Each bp is $25 per contract, so $25 × 6 = $150 per contract. Two contracts → **$300 profit**.

Quiz 5.

Why do we apply a convexity adjustment to interest rates derived from Eurodollar futures?

Say a Eurodollar futures is quoted at 95.00. That means the futures interest rate for the 3-month period is 5%. The convexity adjustment is the amount you have to subtract from this futures rate to turn it into an estimate of the forward rate for the same period.

Why? Because daily settlement on the futures contract makes the futures rate come in higher than the forward rate. We need to fix that.

Quiz 6.

What does duration tell us about the rate sensitivity of a bond portfolio? What are its limitations?

Duration tells us the effect of a small parallel shift in the yield curve on the portfolio’s value. The percentage drop in portfolio value ≈ (parallel shift in rates) × (portfolio duration).

Limitation: this only works for small and parallel shifts. That’s a big asterisk.

Quiz 7.

It’s January 30. You’re managing a $6 million bond portfolio. Six months from now, this portfolio will have a duration of 8.2 years. September-maturity T-bond futures are at 108-15, and the CTD bond’s duration in September will be 7.6 years. How do you hedge?

Each futures contract is worth $108\tfrac{15}{32} \times 1000 = \$108{,}468.75$. Number of contracts to short:

$$\frac{6{,}000{,}000}{108{,}468.75} \times \frac{8.2}{7.6} = 59.7 \approx 60 \text{ contracts}$$Close out at the end of the month.

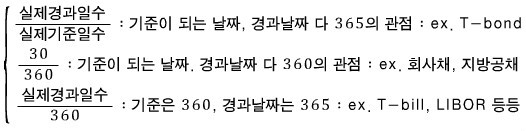

OK, looking at all those quizzes — the recurring theme is how you count days matters a lot. So the first thing we need to nail down is day-count conventions.

Apparently every product uses its own way to count days when quoting prices or computing interest. The two big philosophical camps: do you treat a year as 365 actual days, or do you cheat and call it 360 (with each month rounded to a tidy 30)?

But “two camps” doesn’t mean only two methods. There are actually three:

Let’s just plug in numbers and feel how each one behaves.

Bond face value $10,000, coupon 8%, coupons paid March 1 and September 1. We want the accrued interest from March 1 to July 3 under each convention.

1. Actual/Actual.

It would be a bit much to say none of the September $4 coupon has accrued by July 3 — some chunk of it definitely has. So we compute how much has piled up by July 3.

Reference period March 1 → September 1, i.e. through August 31:

$$31 \times 4 + 30 \times 2 = 184 \text{ days}$$So we earn $4 over 184 days. How many of those have already passed by July 3? March 1 through June 30 is 122, plus 2 more days into July → 124 days “between” March 1 and July 3.

So accrued interest is:

2. 30/360.

Same period. Reference window is just 180 days (six months × 30). For the elapsed days from March 1 → July 3: March, April, May, June each count as 30 → 120 days. Then it’d be weird to throw away those last 2 days, so we toss them in too. Total 122 days.

3. Actual/360.

Now I sort of get the rhythm so this one’s easy — just plug it in.

Now let’s learn how to read the quoted prices in a price table. For various reasons, prices in tables aren’t quoted in straight dollar units. There’s a separate step after that to get the actual cash price — but first you have to be able to read the quote, right?

OK let’s go.

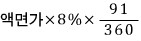

T-bills (short-term money market stuff).

Short-term money market instruments often just quote the discount rate. So if a 91-day T-bill has “8” written on it, that means an interest rate of 8%. And T-bills use that third method — actual/360. So the interest amount on this 91-day, 8% T-bill is:

Right!

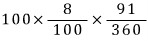

Say face value is 100. Quoted price 8, 91-day instrument. Interest income?

So what’s the cash price?

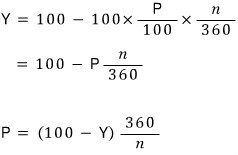

Let $P$ = quoted price, $n$ = maturity, $Y$ = cash price. Just swap in $P$ for 8 and $n$ for 91:

There we go. (And the reference is 100… forgetting that is fatal.)

T-bonds.

Not as easy as T-bills where you just slap a percentage on it. US T-bonds are quoted in dollars and 32nds of a dollar, on a $100 face basis (T-bills also used 100 as the basis). Looking at it cold there’s no way to know what that means…

If a T-bond with face $100,000 is quoted as 90-05, that means:

OK so now we know how the quote becomes a dollar amount. But that’s still not the actual cash price. How do we get there?

Cash price of T-bond = quoted price + “accrued interest since the last coupon date.”

So we just have to get the accrued interest. Not hard. Let’s do one example.

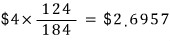

Find the cash price of a T-bond with maturity July 10, ‘28, coupon 11%, quoted price 95-16, as of March 5, ‘13.

Maturity July 10 → coupons paid January 10 and July 10. So a coupon was paid on January 10. We need accrued interest from January 10 to March 5.

T-bonds use actual/actual. Actual days from January 10 to July 10: $31 \times 3 + 30 \times 2 + 28 = 181$. OK.

Days between January 10 and March 5: $31 + 28 + 4 = 54$. (Counting dates is incredibly annoying, seriously.)

Accrued interest from January 10 to March 5:

(per 100)

Done! Now add to the quoted price. 95-16 = $95 + \tfrac{16}{32} = 95.5$.

$$95.5 + 1.64088 = 97.14088 \quad (\text{per } 100)$$Face was 100,000, so multiply by 1000 → cash price = $97,140.88.

Now T-bond futures at CME Group. These are futures on T-bonds with 15-25 year maturities. (Yes, there are also ultra-bond futures with even longer maturities, plus T-note futures at 10/5/2 years — not our subject here.)

The price quotation here is honestly a little annoying. I wish it were just like the spot market… but it’s almost the same, so it’s not bad.

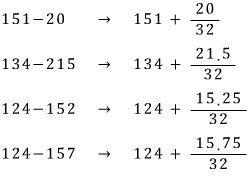

Quotes look like 151-20, 134-215, 124-152, 124-157, etc. That third digit after the dash looks weird, but here’s the deal: T-bonds are quoted in 1/32 units, 10-year T-notes in 1/2 of a 1/32, 5-year and 2-year T-notes in 1/4 of a 1/32. Hence the funky 3rd digit.

To not get confused:

- Two digits after the dash: straightforward, $\tfrac{\text{number}}{32}$.

- Three digits after the dash:

- If the third digit is 0, just use $\tfrac{\text{first two digits}}{32}$.

- If the third digit is 2 or 7, it’s $\tfrac{(\text{two-digit number}).(\text{third digit + 5})}{32}$.

So those quoted prices above work out to:

That’s the meaning! Oh, and don’t forget — based on $100!!

But the futures market has this distinctive feature: the conversion factor. The conversion factor determines how much cash the short-position trader receives.

Definition:

Cash received by short = (most recent futures settlement price × conversion factor) + accrued interest.

(1 futures contract is based on $100,000 face.)

So if the most recent settlement is 90-00, the conversion factor is 1.38, and the bond’s accrued interest is $3:

$$\text{Cash received} = (90 \times 1.38) + 3 = 127$$So the seller of 1 contract gets $12,700.

What does this mean…? Ugh… complicated… ;_;

Here’s the picture: the person who sold the futures contract has to deliver a bond when the delivery date arrives, and they get cash for it. But where do they get the bond? They have to buy it in the spot market. And the “standard 6% yield” the contract is built around almost certainly doesn’t exist out there in the wild…

In which case… how does delivery even work? ;_;

That’s why the conversion factor exists: (when certain internally-set criteria are met) it lets you use a non-standard bond by converting it to the standard via the conversion factor. Apparently.

I think we should compute one ourselves to actually feel what that statement means. ;_;

Said a bit more technically: “the conversion factor of a bond is the quoted price per $1 of face value as of the first day of the delivery month, computed under the assumption that the interest rate is 6% per annum on a semiannual compounding basis throughout the life of the bond.” OK let’s compute one. Let’s go let’s go let’s go let’s go.

Some simple rules first:

- Take the remaining maturity. Drop any leftover period less than 3 months. If what’s left is an integer multiple of 6 months, assume the first coupon comes 6 months from now and compute from there.

- If, even after dropping the sub-3-month leftover, you still can’t carve it into integer 6-month chunks, then assume the first coupon comes 3 months from now, and discount the subsequent coupons back to that 3-months-from-now point to compute the bond’s value.

Easier to see by example.

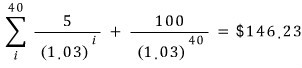

Example A. Coupon 10%, 20 years and 2 months remaining.

Drop the 2 months (it’s less than 3). Maturity becomes 20 years exactly, 40 semiannual periods. Discount all the cash flows starting 6 months from now back to today at the assumed 6% rate:

That comes out to some number, but since we want it “per $1,” divide by 100 → 1.4623. That’s the conversion factor.

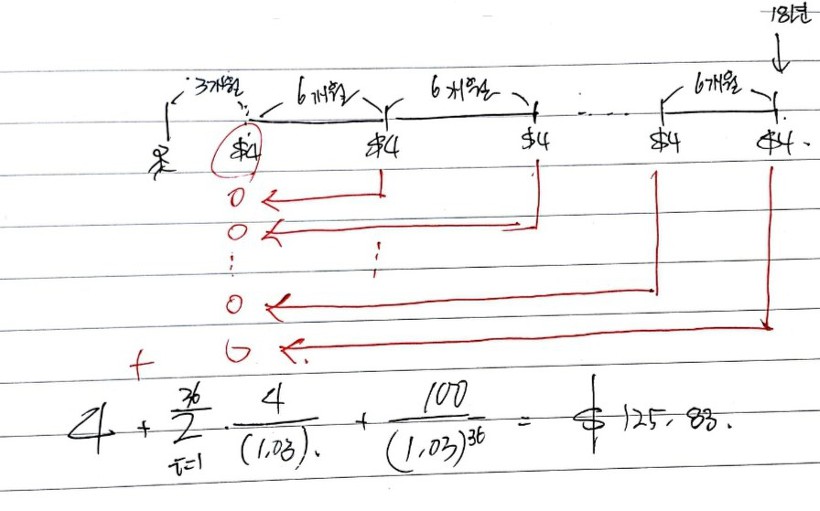

Example B. Coupon 8%, 18 years 4 months remaining.

Even after dropping 3 months (down to 18 years 1 month), we can’t get a multiple of 6 months. So we drop just 1 month and treat it as 18 years 3 months.

We get the first $4 in 3 months, then $4 every 6 months for 18 years after that. Compute the value as of 3 months from now:

(That’s not a “zero” I drew — I just used a circle out of laziness and did the arithmetic underneath. heh.)

So $125.83 is the value 3 months from now. We need to pull it back another 3 months — discount it forward 3 months at 6% on a semiannual-compounding basis:

Now we’ve pulled it back to today. But — the first cash flow we’d built in was $4 happening *now*. And it'd be a bit much to call a coupon happening 3 months out a "now" coupon. So we need to subtract $2 at this stage.

What we have so far: 121.98. Per $100 face. Convert to per $1:

1.2198. That’s the conversion factor.

(Incredibly complicated… but no need to stress — the exchange has a long table of these things, you just look it up. heh.)

So the cheapest-to-deliver bond falls out of all this naturally.

We buy in the spot market and deliver at futures maturity, right? The purchase cost is what we’ve been computing all along:

Purchase cost = spot quoted price + accrued interest.

And what we receive at delivery:

Received = (most recent futures settlement × conversion factor) + accrued interest.

So the short delivers, paying that purchase cost and receiving that delivery cash. The cost to me is spent − received:

$$\text{Delivery cost} = \text{spot quoted price} - (\text{most recent futures settlement} \times \text{conversion factor})$$The bond with the smallest delivery cost is the cheapest-to-deliver.

Interest Rate Futures — Eurodollar Futures

Now let’s see what’s actually traded in the interest rate futures world. The most actively traded interest rate futures contract in the US, apparently, is the 3-month Eurodollar futures at CME Group.

Quick definition: “Eurodollars” = dollars deposited outside the US. The Eurodollar interest rate is the rate at which non-US banks lend dollars to each other — i.e., LIBOR.

The 3-month Eurodollar futures contract is described as “a futures contract on the interest paid by a borrower who borrows $1 million in Eurodollars for 3 months.” Maturities go out to 10 years; delivery months are March, June, September, December.

So sitting quietly in ‘16, you can lock in a 3-month rate for ‘26…? That’s why we say it lets you “speculate on the rate you’ll be exposed to for some future 3-month window, or hedge the exposure.”

But people find Eurodollar futures hard, and the reason is the settlement price is the opposite of everything else. ;_;

For Eurodollar futures, settlement price is 100 − R (where R is the 3-month Eurodollar LIBOR at that moment). So if on October 15, ‘16, the 3-month Eurodollar rate (quarterly compounding) is 0.5% per annum, the quote is 99.500.

Another distinctive feature: daily settlement is structured so that a 1 bp (0.01%) move in the futures price = $25 P&L per contract.

The buyer profits $25 when the futures price rises 1 bp; the seller profits $25 when it falls 1 bp. Since price = 100 − R, when R rises the futures price falls — so the long takes a hit when rates rise (wait, that’s backwards). OK let me re-do that — when R rises, price falls, so the short profits. When R falls, price rises, so the long profits. Makes sense.

Now, actual price of one contract. CME defines it like this:

Q: the price shown on the table.

R is the 3-month rate annualized, so multiply by 1/4 to de-annualize, subtract from 100, multiply by 10,000 (the contract size). Since it’s a pain to read the table, back out R, do 100−R, multiply by 10,000… I think the takeaway is “just plug in the number from the table directly.” heh heh.

Let’s do an example… ;; (mega mental breakdown incoming, because I still have no idea what any of the above actually means ;;).

Hoo… ;_; here we go.

Starting September 16, ‘15, you want to lock in the rate for borrowing $100 million in Eurodollars for 3 months. The September ‘15 Eurodollar futures price is 96.500 — meaning you can fix the annual rate at 3.5%. Hedge by buying 100 contracts.

If on December 16, ‘15, the 3-month Eurodollar rate becomes 2.6% per annum, the final settlement price is 97.400. So the gain (at $25 per bp per contract):

$$100 \times 25 \times 100 \times (97.40 - 96.50) = \$225{,}000$$(The way I read this: the leading 100 is because the contract size is $1M and we're hedging $100M → 100 contracts. The 25 is the $25 per 1 bp. But $1 \text{ bp} = 0.01%$, while $97.40 - 96.50 = 0.9$ is in *percent* units, not 0.01% units. So the extra ×100 after the $25 converts “per 0.01%” into “per 1%.” So $25 per bp = $2,500 per 1%. Same thing.)

Anyway, the gain from the price move is $225,000.

Plus the interest you actually earn investing at 2.6% for 3 months: $100{,}000{,}000 \times \tfrac{1}{4} \times 0.026 = \$650{,}000$.

Total: $875,000.

Which is exactly what you’d earn if the annual rate were locked at 3.5%:

$$100{,}000{,}000 \times \tfrac{1}{4} \times 0.035 = \$875{,}000$$So Eurodollar futures effectively let you fix the rate at 3.5%! From this angle, it looks just like an FRA (forward rate agreement)!

For maturities up to 1 year, Eurodollar futures are basically identical to FRAs — so the textbooks say. But as maturity stretches out, the differences widen.

The biggest difference comes from daily settlement. With Eurodollar futures, final settlement happens at $T_1$ based on the realized rate at each point between $T_1$ and $T_2$. With an FRA, final settlement happens at $T_2$ based on that same realized rate. That’s the gap…

But since the core idea — settling on a totally future interest rate ahead of time — is so similar, the scholars built a bridge between them:

- σ: standard deviation of changes in the short rate, in annual units

- $T_1$: futures maturity

- $T_2$: maturity of the underlying interest rate

- All rates continuously compounded.

(https://www.math.nyu.edu/~alberts/spring07/Lecture4.pdf)

Go look at this link if you want — various derivations of the convexity adjustment in there. heh.

Now we should talk about duration, but I covered duration in detail before. So I’ll assume you know it and skip ahead.

http://gdpresent.blog.me/220718454071

What I studied in Basic Investment Theory #16: Duration, Modified Duration

One thing to add: that earlier post was based on annual compounding with one coupon a year. But in derivatives we use continuous compounding most of the time. Under continuous compounding, duration and modified duration collapse to the same thing — the difference vanishes. ;_;

The numerical difference disappearing means it’s not technically wrong to write either one, but I think we should still be aware they mean different things, and move on.

Hoo~ OK let’s keep going.

Since we just did duration, let’s talk about bond portfolios.

We can compute duration for an individual bond. So how do you compute duration for a portfolio of bonds?

Probably feels obvious… Even though it’s a portfolio, since it’s all bonds, the portfolio’s duration is just the weighted average of individual bond durations, weighted by each bond’s investment weight in the portfolio.

So can we use this portfolio duration the same way we used individual-bond duration?

Of course not.

But — we can, if we make one extreme assumption: that all bonds in the portfolio “respond identically to a $\Delta$ shift in interest rate, regardless of maturity.”

Under that assumption, you can use duration on a bond portfolio exactly the way you used it on an individual bond. The portfolio-of-bonds gets treated as a single bond.

Now… we already studied bond yields enough to know that bond prices respond to rate moves very differently depending on maturity. So this assumption is honestly absurd lol.

But the reason for stretching that hard is so we can at least mention duration matching, a hedging strategy.

Duration matching is supposedly extremely important for financial institutions like banks. Recall the duration intuition: “on average, how many years until all the future cash flows arrive?” Now think about a bank.

A bank’s main business is taking deposits from a bunch of people and making loans to other people, living off the spread, right?

Let’s go to the extreme: imagine a bank that only makes long-term loans. Deposits come in all flavors — short-, medium-, long-term. So the timing when money has to leave the bank (deposit withdrawals) and the timing when money comes back in (loan repayments) don’t line up.

What does the bank have to do? Duration matching. Apparently.

The reason this content sits in chapter 5 (interest rate futures) is that the tool used for duration matching is interest rate futures. (For reference!)

But in reality this duration-matching strategy isn’t really used. heh heh heh heh. Because… that absurd assumption from earlier.

There’s apparently an upgraded version called GAP management strategy, but that’s beyond the scope of this book and won’t be covered. (Yeah, I didn’t want to do it either.)

OK so when we do use interest rate futures for duration matching — how many contracts do you use? Let me throw down the formula first:

The meaning of this formula will land hard once we work through practice problems, so I won’t yap about it here.

The idea: if a $\Delta$ shift in rates causes a loss in your portfolio, you take an interest rate futures position that moves opposite to that loss to hedge. If you lose when rates fall, you want a futures position that profits when rates fall. In interest rate futures, the buyer profits when rates fall (because falling rates → rising futures price). So that company would go long interest rate futures. The opposite situation → short.

This whole thing is called the duration-based hedge ratio. That’s literally what it is.

We said this is barely used in practice, because of the extreme assumption. heh heh heh. But for very very small, basically nonexistent shifts, it’s good enough as a hedge. Even if it’s kind of meaningless…

Oh, and: for long durations you typically use T-bond or T-note futures (long durations themselves), and for short durations you use T-bill or Eurodollar futures (short durations). (Also feels obvious, heh heh.)

Let’s just do an example on the duration-based hedge ratio and move on.

Q.

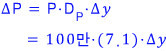

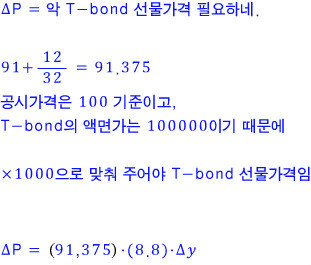

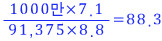

It’s August 2. A fund manager is running $10 million of government bonds and is worried about big rate moves over the next 3 months. They decide to hedge with December-maturity T-bond futures.

T-bond futures specs:

- Quoted price 93-02 ($92,062.50)

- Face $100,000

- So 1 contract = $93,062.50

Portfolio duration 3 months from now: 6.8.

Cheapest-to-deliver bond is a T-bond with 20-year maturity and 12% coupon. Current yield 8.8%, duration at maturity 9.2 years.

What position should the manager take?

→ Long $10M of bonds. If rates rise, prices fall → loss. So they want a position that profits when rates rise. In interest rate futures, prices fall when rates rise — so they want to be in a position that profits when futures prices fall → short.

How many contracts?

Prob 6.8.

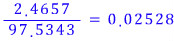

The quoted price of a 90-day T-bill is 10.00. What’s the continuously compounded return earned by an investor in this T-bill over 90 days? (real/365 basis.)

Cash price first:

So the investor invests 97.5343 and earns 2.4657, meaning:

Convert to continuous compounding:

Annualize on real/365:

(By the way, I write those side notes in blue pen, but the SC app barely picks up blue. Doesn’t pick up red well either. ;; -- -- -- -_-)

Prob 6.9.

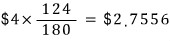

A government bond, 12% annual coupon, maturity July 27, 2024, quoted 110-17 as of May 5, 2013. Cash price?

110-17 in money: $110 + \tfrac{17}{32} = 110.53125$.

Now accrued interest. T-bonds use real/real. Day count, go go go.

Coupons on January 27 and July 27.

January 1 to June 30: $28 + 31 \times 3 + 30 \times 2 = 181$ days. So January 27 to July 26 is 181 days.

Now, January 27 to today (May 5):

- January 1 to April 30: $28 + 31 \times 2 + 30 = 120$ days.

- January 1 to May 4: 124 days.

Subtract 26 → days “between” January 27 and May 5 = $124 - 26 = 98$ days.

Accrued interest for 98 days:

So cash price = $110.53125 + 3.24862 = 113.77987$.

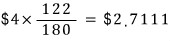

Prob 6.11.

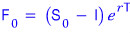

As of July 30, 2015, the cheapest-to-deliver bond for the September 2015 T-bond futures has coupon 13% per annum, and delivery is expected on September 30, 2015. Coupons on February 4 and August 4 each year. The term structure is flat (so the future rate stays constant) and the rate is 12% per annum on semiannual compounding. Conversion factor 1.5, current quoted price 110.

Find the quoted futures price.

We need the futures price. Formula:

right?

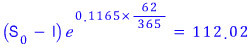

S is the current spot price, computed from the quoted price. Current cash price on July 30 is $110 + \tfrac{0}{32} + \text{accrued interest}$, so we just need accrued interest to get S. Done.

Dammit, counting dates again.

February 4 → August 4 = 181 days.

February 4 → July 30: from February 1 to July 31 is 181 days; subtract 3 from February and 2 from July → days “between” February 4 and July 31 is $181 - 5 = 176$.

Accrued interest:

So current cash price is $110 + 6.32 = 116.32$.

And we need to pull back the $6.5 coupon happening 5 days from now as accrued interest~~

Dammit, I have to convert to continuous compounding first, since the rate is 12% per annum semiannual:

Pulling back the $6.5 occurring 5 days from now as accrued interest:

That is:

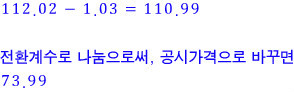

Now push to future value at September 30 → that’s the futures price. How many days do we push? Think about it carefully — 62 days.

Finally, hand back the accrued interest earned between August 4 and September 30. That’s 58 days’ worth.

Prob 6.13.

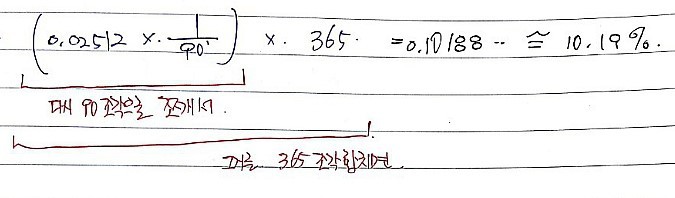

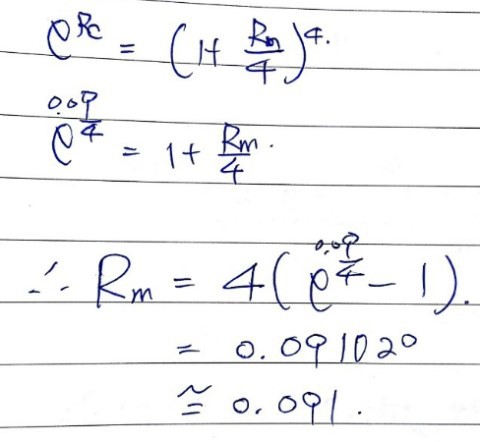

The 9-month LIBOR is 8% per annum, the 6-month LIBOR is 7.5% per annum. (Both real/365 and continuously compounded.) Find the quoted price of a 3-month Eurodollar futures contract maturing 6 months from now.

Eurodollar futures quote = 100 − R. So our goal is the futures interest rate.

The Eurodollar maturing in 6 months will be set by the 3-month LIBOR between months 6 and 9. The forward rate between 6 and 9 months:

OK OK.

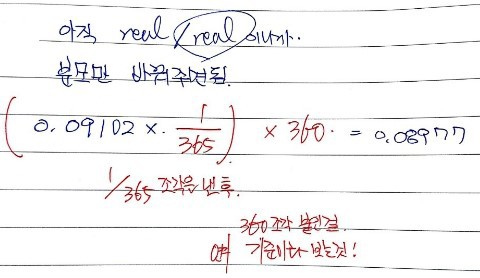

Those 8% and 7.5% — those were real/365 and continuously compounded. But LIBOR is quarterly compounding and real/360. So we need to convert this 9% (continuously compounded) over to quarterly compounding.

(Suddenly hit by typing laziness… ;_; sorry.)

So with the forward rate at 8.977%, the quoted price is $100 - R = 100 - 8.977 = \mathbf{91.023}$. Boom.

Prob 6.14.

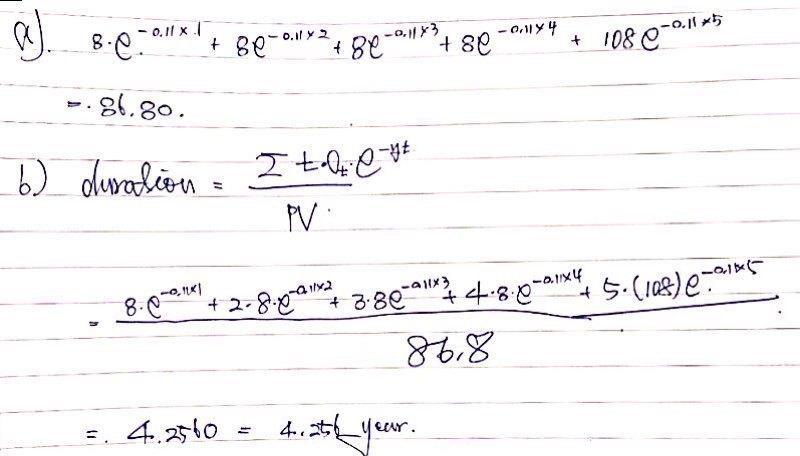

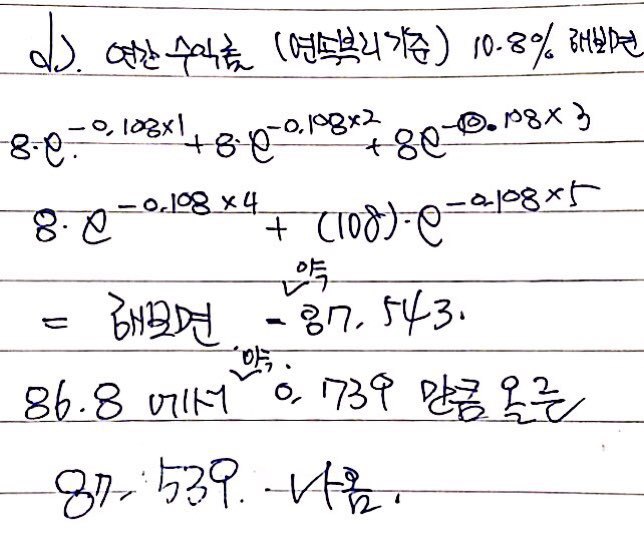

A 5-year bond, yield 11% per annum continuously compounded, paying 8% coupon at year-end (face $100).

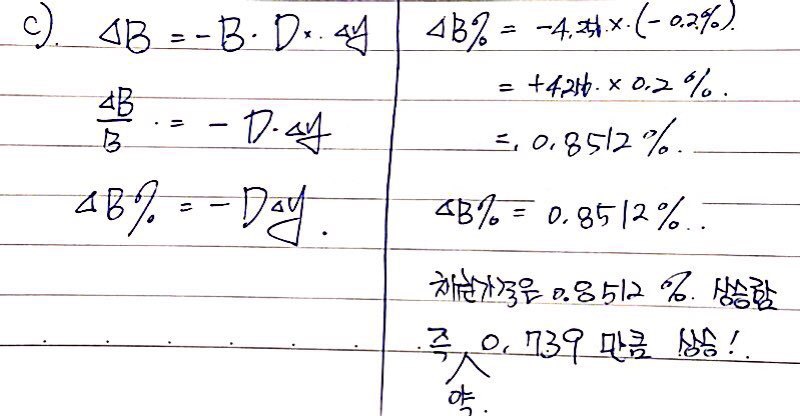

a. Bond price? b. Bond duration? c. Using duration, the effect of a 0.2% drop in yield on the price? d. Recompute the price at 10.8% and check it’s consistent with c.

Unless I’ve completely lost it, am I really going to type all of this out? lololololol

Prob 6.17.

It’s August 1. A portfolio manager runs a $10M portfolio. In October, the portfolio’s duration will be 7.1 years. December-maturity T-bond futures are at 91-12, and the CTD bond’s duration at maturity will be 8.8 years. How does the manager duration-match against rate moves over the next 2 months?

Price change of the portfolio at maturity in terms of duration:

The T-bond futures used for hedging:

We want $\Delta P = \Delta V$, so the duration-based hedge ratio is:

Number comes out to 88 contracts. Sell or buy?

The portfolio is bonds → loses when rates rise. The manager is nervous about that, so they want a position that profits when rates rise → short interest rate futures.

How many? 88 contracts.

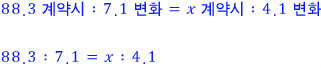

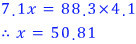

Prob 6.18.

In Prob 6.17, how does the portfolio manager change the duration to 3 years?

Same principle as moving β in stock portfolios back in the day.

Using 88 contracts shifts duration from 7.1 → 0. So how many contracts do you need to shift it not by −7.1 but by only −4.1, leaving the duration at 3.0?

You can frame it that way. Since the duration-based hedging strategy comes from a first-order linear relation:

Solve the proportion for the unknown contract count $x$:

Turns out you should use 51 contracts~~~~

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.