Fundamentals of Interest Rate Swaps

A casual walkthrough of how interest rate swaps actually work — fixed vs. floating rates, notional principal, and why companies would sign up for this in the first place.

OK let’s get swaps sorted out.

First, the textbook-y definition, just to throw it out there:

“An over-the-counter derivatives contract between two companies that exchange cash flows in the future, on terms agreed in advance.”

Here’s the thing that’ll click as we go further: a forward is a contract for cash flows at one point in the future. A swap? Cash flows at multiple points in the future, periodically.

So, basically — couldn’t you call a swap a continuous forward?

In this Chapter 7 we’re doing interest rate swaps and currency swaps. Tons of other kinds exist too, but those are wayyyy later — chapter 22-ish.

OK then. Let me build up interest rate swaps step by step. (Opening monologue mode, engage.)

So, fundamentally, an interest rate swap is just an exchange of a fixed rate and a floating rate, and whoever does it gets to change the nature of their own liability.

Like, if a company enters a swap, it agrees to pay a contracted fixed-rate interest for several years, and during that same period, it receives floating-rate interest on the same principal.

You might be sitting there going, “wait, couldn’t it go the other way too?” or “the counterparty is doing the exact opposite of this, right?” — yeah, all of that’s correct.

The floating rate used in this swap is LIBOR. (LIBOR is apparently the benchmark rate of international finance, or so they tell me.)

Let me get more concrete so swaps actually feel like a thing.

Say Company A and Company B sign a 3-year swap. The terms:

A pays B 5% per annum on a $100 million principal (semi-annual compounding), and B pays A "6-month LIBOR" on that same $100 million principal. That’s the contract.

Meaning interest gets exchanged every 6 months.

After the first 6 months, A pays B $2.5 million (do the math — half of 5% of $100M is $2.5M, yep).

Say 6-month LIBOR at signing was 4.2%. Then B pays $100M × (0.042 / 2) = $2.1 million.

Now 6 months have passed since signing, and on that day 6-month LIBOR was 4.8%.

Another 6 months go by…

A still pays B $2.5 million as always. But B — because the "6-month LIBOR" from 6 months prior to *this* payment date was 4.8% — pays $100M × (0.048 / 2) = $2.4 million.

And this just keeps going, on and on, all the wayyy out to year 3!!!

Oh, but there’s something I left out:

In real life, an interest rate swap doesn’t actually involve both sides handing over the full interest amounts in raw cash like I described above. Only the difference between the two interest payments changes hands. Apparently.

And the $100 million principal? It only exists as the basis for calculating interest — it doesn’t actually move at all, right???

So that principal gets called the “notional principal”!

But why on earth would companies enter into such a weird-looking contract?

It’s not like both of them just suddenly went insane and wanted to play rock-paper-scissors with their balance sheets, right????

Here’s why this swap actually happens:

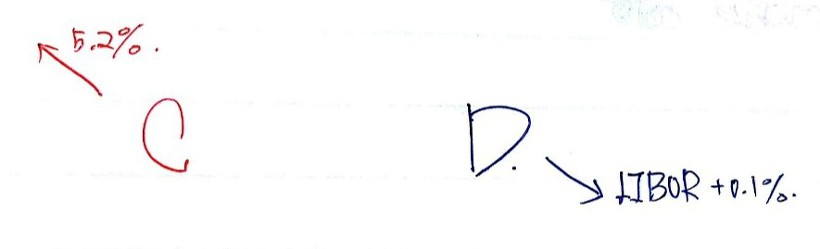

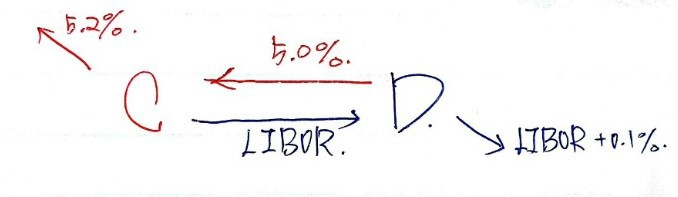

Company C had no choice but to raise funds at a fixed rate, so it borrowed at fixed 5.2%. Company D had no choice but to do floating, so it borrowed at LIBOR + 0.1%.

But both C and D, on second thought:

C doesn’t actually want to be paying back fixed-rate interest, and D doesn’t actually want to be paying floating-rate interest either…..

When C and D meet, in this exact state:

OK so — going back to what I said way up at the top, the part about a swap “changing the nature of an asset from fixed to floating, or floating to fixed” — I think you can see what that means now.

But here another question pops up:

Why didn’t they just do what they wanted from the start? C raises floating on its own, D raises fixed on its own — done???????

Was it a change of heart??? Does “change of heart” fly in corporate management???? A change of heart??????

Nope, can’t be a change of heart…. so what is it.

Earlier I said “C had no choice but to do fixed” and “D had no choice but to raise floating.” Take that literally — even if C wanted floating, it couldn’t get it; same for D and fixed.

Because C had a ‘comparative advantage’ in fixed-rate funding, and D had a ‘comparative advantage’ in floating-rate funding.

And the reason that comparative advantage exists is — the people lending the money charge different rates depending on the borrower’s credit.

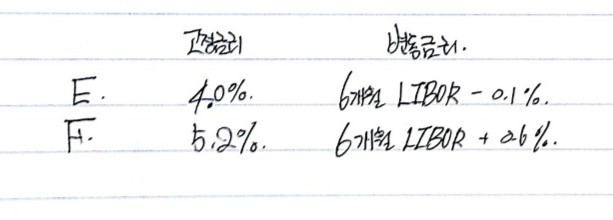

OK so picture Company E here, a company with great credit. Lenders see them as super creditworthy, so they get offered 4.0% fixed, or 6-month LIBOR − 0.1% floating.

And say Company F has worse credit than E — so F gets quoted 5.2% fixed, or 6-month LIBOR + 0.6% floating.

Now think from F’s side.

Company F, eyeing Company E, is going:

“On fixed we’re behind by a full 1.2%, but on floating we’re only behind by 0.7%!!! So floating it is — that’s how we close the gap with E!!!! gogogo!!!!!”

Meanwhile, Company E….. (for this example, everybody has to be more evil than strictly necessary…)

“Ugh, Company F is such a stubborn little pest, why aren’t they going extinct already??? Why??? Do we have to step in and crush them ourselves???????

OK fine — we want floating, but if we go floating we’re only 0.7% better than them. Let’s go fixed instead, where our edge is a fat 1.2%, and blow the gap wide open!!!!!

We’ll bury Company F by widening the spread!!! Never let them climb up!!!

No — better yet, we’ll climb up faster and kick the ladder out!!!! Show them the power of a megacorp pulling the ladder up behind it!!!!!”

So now the situation looks like:

It’s gotten that bad!!!??

But — ironically — these two then meet??????

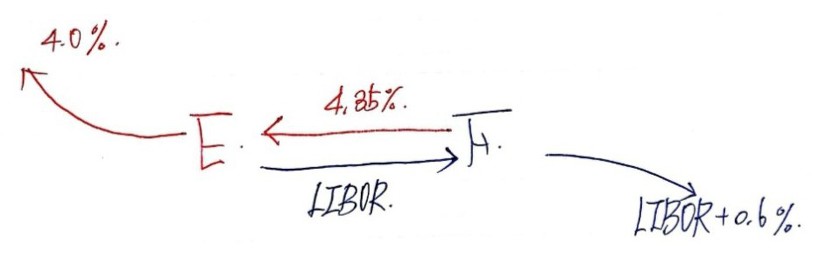

If those two go and do a ‘fair’ swap ( — how to make it fair, coming up next — )

It comes out like this….???

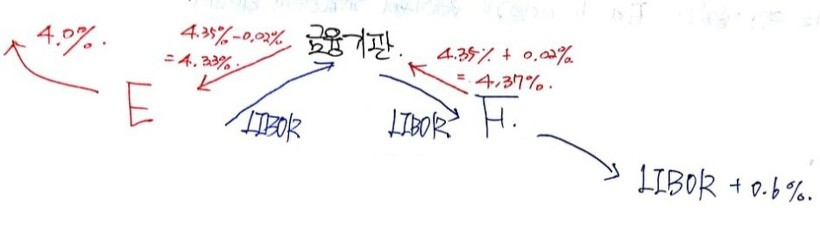

Look at it for a sec. The floating-rate borrowing that Company E was so desperate for? It comes out to LIBOR − 0.35%, which is actually cheaper than the LIBOR − 0.1% they were originally offered.

And Company F successfully converted to fixed-rate borrowing like it wanted, and they end up paying an effective 4.95%, which is cheaper than the 5.2% they were originally offered….

Whoa…. so the reason swaps have to exist was comparative advantage….

(Heads up — there are people who push back on the “comparative advantage is why swaps exist” view. It’s not gospel.)

I already hinted this was a ‘fair’ swap, so let’s stare at the numbers and figure out why it’s fair, so we can use this going forward, heh.

If you look closely, both Company E and Company F improved by exactly the same amount — 0.25% each.

Where does that come from?

Rate spread in the fixed market: 1.2% Rate spread in the floating market: 0.7% Subtract: 1.2% − 0.7% = 0.5%

Ahhh I see — each side improving by 0.25% means:

“(spread in fixed market) − (spread in floating market) = 0.5%”

and half of that — both sides get 0.25% each!!!!!!

Now another thing to chew on:

How would any company actually find another company that is exactly!! the polar opposite of itself…

Yeah — actually, unlike A and B, C and D, E and F, who I had signing swaps directly with each other as counterparties, that’s not really how it goes in the wild.

Each company signs the swap with a ‘financial institution’ sitting in the middle, and on the other side of that financial institution — the company doesn’t even know if there’s a counterparty company over there or not;;;

In exchange, the financial institution scoops a margin of about 2–4 bp (0.02% ~ 0.04%). Apparently?

So once a financial institution wedges itself between E and F like this:

It comes out like this!!!!!! Even with the financial institution in the middle, both E and F still benefit (a bit shaved, sure), and the financial institution also benefits!!!!!

But the FI being in the middle isn’t just a haircut for nothing.

For one — that whole chore of having to find a matching counterparty company yourself? Don’t have to do it anymore.

And more importantly: even if one side defaults, the financial institution eats the whole thing. They’d scramble to re-match the busted side so cash flows still keep flowing to the non-defaulting side, right?

So those 2–4 bp leaking off to the financial institution? That’s the price for those services.

But then — from the financial institution’s side — is it actually easy to find two perfectly opposite companies and play matchmaker in the middle????

Nope. So financial institutions just put together their own menu of swaps and run a business off it. Apparently.

Companies then look at the menu and go:

“Ah, the swaps available to us aren’t unlimited — what’s on the menu is what’s on the menu.”

“Now how do we make this work for us?!?!?!” — and that part’s up to each company, right?

The fact that financial institutions go and stand up this kind of structure in the market — that’s called “acting as a market maker.”

Market makers post a table that looks something like this:

and they go ahead and enter swaps off of it (even when there’s no company on the other side yet).

* The average of the bid fixed rate and the ask fixed rate is what determines the “swap rate.”

Originally written in Korean on my Naver blog (2016-10). Translated to English for gdpark.blog.