Swaps: Practice Problems

Working through classic swap design problems — comparative advantage, LIBOR discounting, and currency swaps — with the actual numbers worked out step by step.

quiz 1.

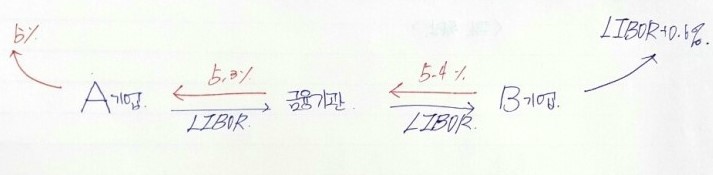

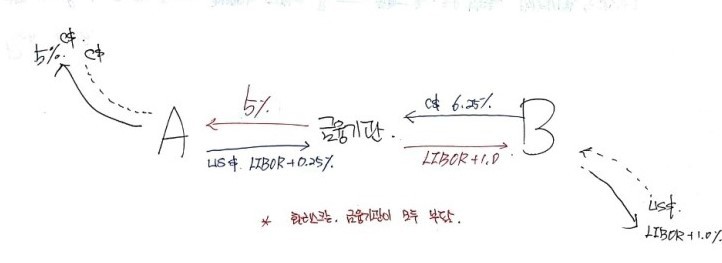

Companies A and B both want to borrow $20M for 5 years. Here’s what the market quotes them:

| Fixed | Floating | |

|---|---|---|

| Company A | 5.0% | LIBOR + 0.1% |

| Company B | 6.4% | LIBOR + 0.6% |

A wants floating. B wants fixed. The bank in the middle wants 0.1% per year for itself. Design the swap so A and B walk away with equal benefit.

OK so notice the setup — A has a comparative advantage in the fixed market, but it wants floating. B has a comparative advantage in the floating market, but it wants fixed. That mismatch? That’s exactly what makes a swap possible.

Look at the gaps: 1.4% per year between the fixed quotes, 0.5% between the floating quotes. So the total pie up for grabs through the swap is $1.4 - 0.5 = 0.9\%$ per year.

The bank skims 0.1%, leaving 0.8% for the two companies. Split evenly → 0.4% each.

Which means: A ends up borrowing floating at LIBOR − 0.3%, and B ends up borrowing fixed at 6.0% per year.

quiz 2.

A $100M interest rate swap has 10 months left. Under it, 6-month LIBOR gets exchanged for 7% per year (semiannual compounding). The current average bid-ask for swaps of all maturities exchanged against 6-month LIBOR is 5% per year (continuous compounding). 6-month LIBOR was 4.6% per year two months ago.

What’s the swap worth to the floating payer? And to the fixed payer? Use LIBOR discounting.

OK so 4 months from now, we receive $0.5 \times 0.07 \times 100\text{M} = 3.5\text{M}$ and pay $0.5 \times 0.046 \times 100\text{M} = 2.3\text{M}$. (Day count, ignore.)

Then 10 months from now, we receive another $3.5M and pay floating based on whatever LIBOR turns out to be 4 months from now.

Value of the fixed-rate bond inside the swap:

Value of the floating-rate bond inside the swap:

So from the floating payer’s perspective, the swap is worth $102.718 - 100.609 = 2.109$ million dollars. From the fixed payer’s side, flip the sign — it’s $-2.109$ million.

And here’s the cool part — you get the same number if you decompose the swap into a portfolio of forward contracts.

From the floating payer’s view, the first forward is: pay 2.3M, receive 3.5M, in 4 months. Its value:

The forward rate is 5% per year continuous (or 5.063% semiannual), so the second forward is worth:

Total: $1.180 + 0.929 = 2.109$ million dollars. Same answer. Nice.

Quiz 3.

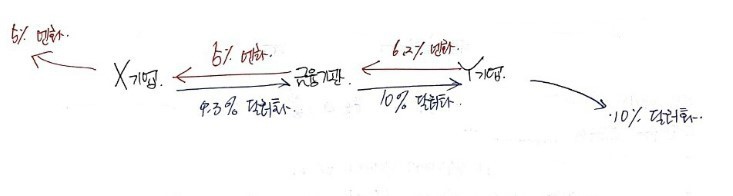

Company X wants to borrow USD at a fixed rate. Company Y wants to borrow JPY at a fixed rate. At today’s exchange rate, the amounts they need are roughly the same. Quotes:

| Yen | Dollar | |

|---|---|---|

| Company X | 5.0% | 9.6% |

| Company Y | 6.5% | 10.0% |

Bank wants 50bp (0.05%, wait no — 0.5%) for itself. Design the swap so both companies benefit equally and the bank eats all the FX risk.

X has the comparative advantage in yen but wants dollars. Y has the advantage in dollars but wants yen. Classic swap setup.

The yen gap is 1.5%. The dollar gap is 0.4%. So the total benefit going around is $1.5 - 0.4 = 1.1\%$ per year.

Bank takes 0.5%, leaving 0.6% for X and Y → 0.3% each.

So X ends up borrowing dollars at $9.6 - 0.3 = 9.3\%$, and Y ends up borrowing yen at $6.5 - 0.3 = 6.2\%$.

Quiz 4.

Explain the swap rate. And the relationship between the swap rate and the par yield.

The swap rate at a given maturity is the average of the bid and ask fixed rates that a market maker is willing to exchange for LIBOR in a standard plain-vanilla interest rate swap of that maturity.

What “standard” means — number of payments, day count — varies by country. In the US, payments on a standard swap go semiannually, the day count for LIBOR is actual/360, and for the fixed side it’s actual/365.

And the swap rate at a given maturity is the LIBOR par yield for that maturity. They’re the same thing.

Quiz 5.

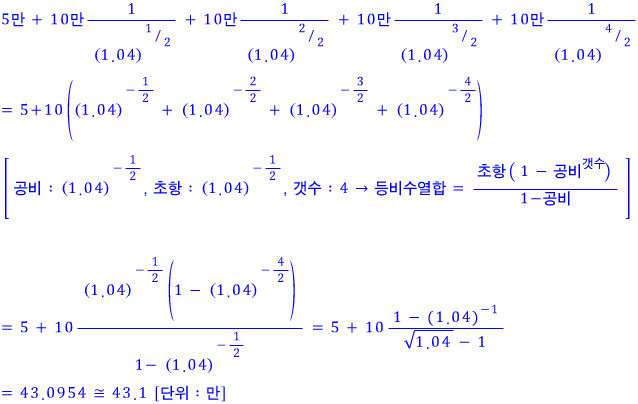

A currency swap has 15 months left. Once a year, it exchanges 10% interest on £20M for 6% interest on $30M. Term structure is flat in both UK and US. If the swap were entered into today, the going rates would be 4% for dollars and 7% per year for pounds. Annual compounding. Current spot is 1.5500 dollars per pound.

What’s the swap worth to the trader paying pounds? And to the trader paying dollars?

In this swap, the cashflows exchanged are $20 \times 0.1 = £2.0\text{M}$ and $30 \times 0.06 = \$1.8\text{M}$.

Value of the pound-denominated bond inside the swap:

Value of the dollar-denominated bond inside the swap:

So from the pound-payer’s view, the swap is worth $32.061 - 22.182 \times 1.55 = -2.322$ million dollars. From the dollar-payer’s view, flip the sign → $+2.322$ million dollars.

And again — same result if we treat the swap as a portfolio of forwards.

The continuous-compounding equivalents of 4% and 7% are 6.766% (wait — that’s the dollar one being 3.922% and pound being 6.766%, actually let me line that up: dollar 3.922%, pound 6.766%). The 3-month and 15-month forward exchange rates are:

And the values of the two forwards corresponding to principal:

Adding it all up:

$$-1.266 - 1.135 + 0.079 = -2.322 \text{ million dollars}$$Same answer. Beautiful.

quiz 6.

Explain the difference between credit risk and market risk in financial contracts.

Credit risk = the chance the counterparty defaults on you.

Market risk = the chance market variables (rates, FX, etc.) move against you.

Here’s what makes swaps tricky though: the credit risk on a swap depends on the market variables. Your counterparty’s default only hurts you when the swap is currently worth something positive to you. If the swap is underwater for you, them defaulting is… fine, actually.

quiz 7.

A treasurer signs a contract to “borrow at a competitive fixed rate of 5.2%.” Their explanation: they borrowed at 6-month LIBOR + 150bp and swapped LIBOR away at 3.7%. So $-(\text{LIBOR} + 1.5\%) + \text{LIBOR} - 3.7\% = -5.2\%$. Locked in at 5.2%, right?

What is the treasurer missing?

The rate isn’t actually fixed.

Because — what happens if the company’s credit rating drops? Then when they go to roll the floating-rate borrowing, they’re not getting LIBOR + 150bp anymore. Their effective fixed cost goes up.

Concrete example: if the spread on their floating leg widens from 150bp to 200bp, their “fixed” rate just went from 5.2% to 5.7%. Not so fixed.

Prob 7.9

Companies X and Y want to invest $5M for 10 years. Quotes given to each. X wants fixed, Y wants floating. Bank takes 0.2% per year. Design the swap so benefits are equal.

Oh wow — this time it’s not borrowing, it’s investing. So those interest rates aren’t what we pay, they’re what we receive!

OK so let me think. If X receives the fixed 8.0%, it’s losing by 0.8 to Y on the fixed side, so X is better off taking LIBOR where there’s no spread between them.

Y on the other hand — if Y takes LIBOR, it can’t beat X. But if Y takes fixed, it beats X by a 0.8% margin.

OK.

Drew up to here.

For the gains to split evenly: $|(\text{fixed gap}) - (\text{floating gap})| = |0.8 - 0| = 0.8\%$, so each side gets 0.4%. And if the bank takes 0.2% (0.1% from each), then both companies still come out 0.3% ahead of where they started!

Prob 7.10

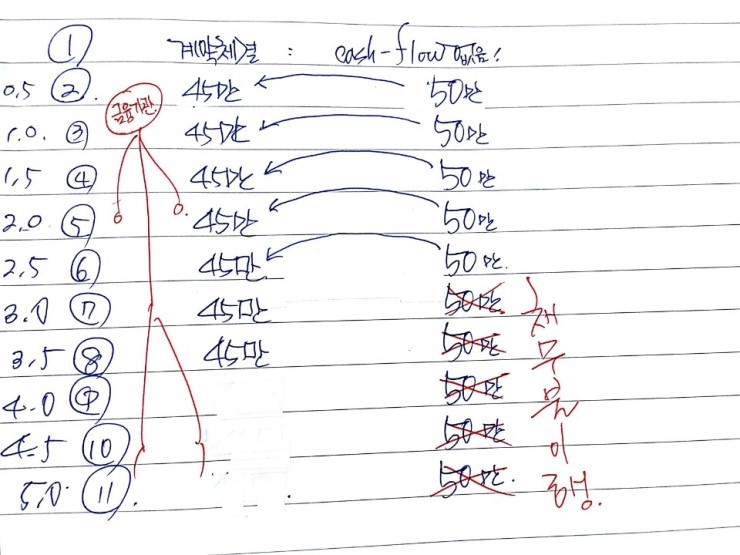

A financial institution enters a 5-year swap with Company X on $10M principal: receive 10% fixed, pay 6-month LIBOR. Payments every 6 months. X defaults during year 3. At default time, all maturities yield 8% per year (semiannual compounding). 6-month LIBOR was 9% per year up through the midpoint of year 3. What’s the FI’s loss?

Ugh… seriously, what is this. Why is there a default in here (sob).

OK. Each cash flow:

- Fixed leg: half of 10% on $10M → $500,000.

- Floating leg: 9% per year up through the midpoint of year 3 → $450,000 per cashflow.

Pretend the swap had run all the way to maturity:

Now PV everything back to year 3:

Prob 7.12

Companies A and B got these quotes:

| US$ | C$ | |

|---|---|---|

| Company A | LIBOR + 0.5% | 5% |

| Company B | LIBOR + 1.0% | 6.5% |

A wants US$ floating. B wants C$ fixed. Bank wants 50bp. If A and B share the benefit equally — what rates do they each pay?

This one looks easy — let me just rip through it.

For A to clearly beat B, A should borrow C$ fixed. For B to not get crushed by A, B should borrow US$ floating. But neither of them wants that. They said no.

So they swap. Total benefit available:

$$|(\text{fixed gap}) - (\text{floating gap})| = |0.5 - 1.5| = 1\%$$Half to each → 0.5% each.

In other words: A gets LIBOR — that’s 0.5% better than the LIBOR + 0.5% it would’ve paid without the swap. B gets 6% — that’s 0.5% better than 6.5%.

Now layer the bank’s 0.5% on top, 0.25% from each side. So we just shave 0.25% off each:

A pays LIBOR + 0.25% B pays 6.25%

Prob 7.18

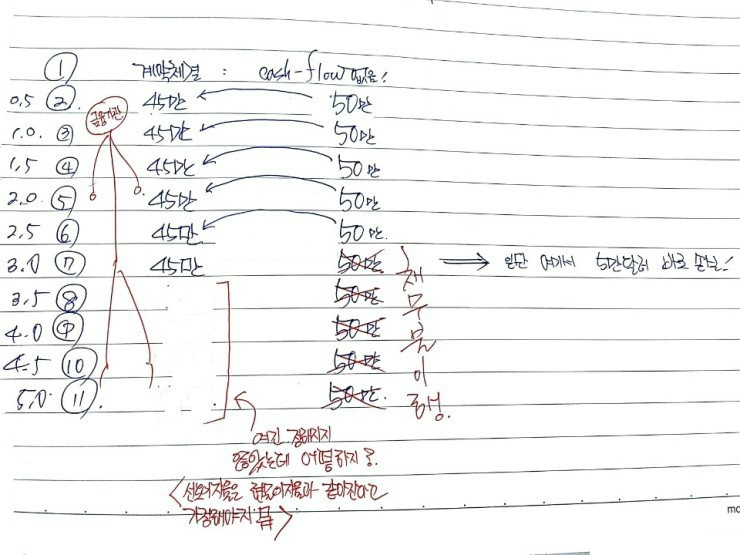

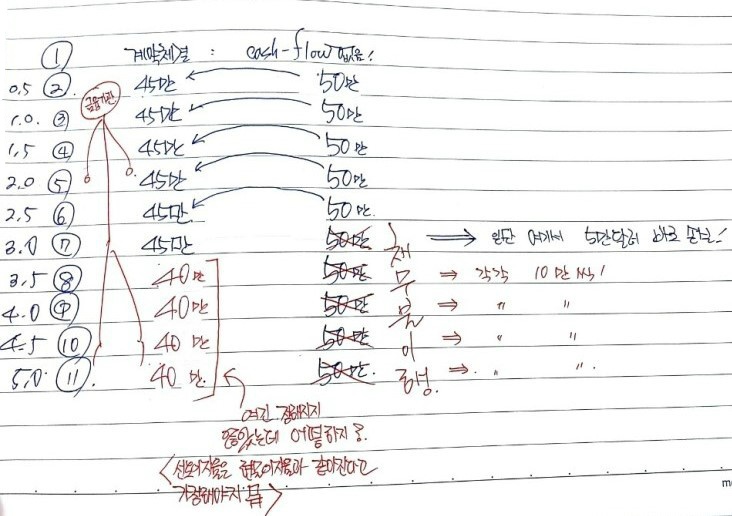

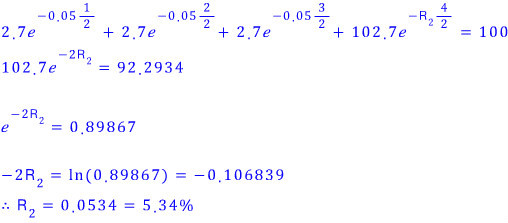

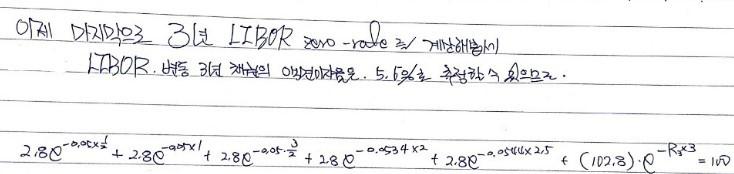

The LIBOR zero-coupon yield curve is flat at 5% per year (continuous compounding) out to 1.5 years. The 2-year and 3-year semiannual swap rates are 5.4% and 5.6%. Estimate the LIBOR zero rates at 2 years, 2.5 years, and 3 years. (Use the fact that the 2.5-year swap rate is the average of the 2-year and 3-year swap rates. LIBOR discounting.)

OK so the 0.5y, 1y, and 1.5y zero rates are all 5% — given.

The 2-year swap rate being 5.4% means: a LIBOR par bond at 2 years has a coupon rate of 5.4%. That means it trades at par, 100.

5.4% of 100 = 5.4, so a floating bond paying 2.7 each half-year prices at 100 with a yield of 5.4%:

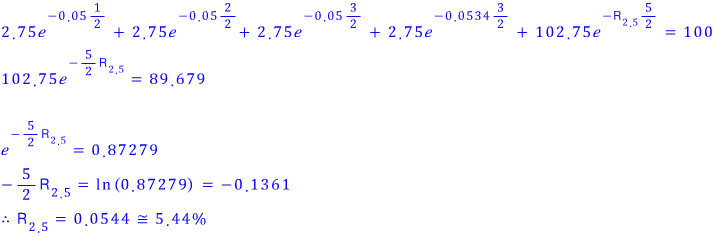

And since the 2.5-year swap rate is the arithmetic mean of the 2-year and 3-year, it’s $(5.4 + 5.6)/2 = 5.5\%$.

Same trick to back out the 2.5-year zero rate:

OK honestly, the 3-year one — typing this whole thing out in the equation editor is too much of a pain. Sorry. You’ll get the idea.

Originally written in Korean on my Naver blog (2016-11). Translated to English for gdpark.blog.