Options

A casual intro to options — call vs. put, why theoretical prices even matter, and how Black-Scholes blew the whole market wide open.

So the derivatives course I’m taking is basically split into “before midterm” and “after midterm.”

Before: No Options. After: Options. That’s literally the whole organizing principle lol.

Which means from here on out it’s options, options, options…

So I gotta talk about options now,,,

Real talk — I actually mentioned options once, way back in an old post…

So I’m gonna do some copy-paste action… sorry sorry

I just don’t wanna say the same stuff twice (T_T)

Pulling content from here: Financial Engineering Programming I Studied #1.

Why do we even need a theoretical option price?

Like… before this whole theory got worked out (around the 19th century), people were obviously already trading options.

And those folks managed to trade just fine without knowing a thing about “theoretical prices.”

Answer: back then the market was tiny. After the Black-Scholes model dropped, the options market exploded. HUUUUGELY.

And then people started using the theoretical price as a kind of compass for trading…

Anyway! That’s the historical setup, and that’s why we need the theoretical price (the compass).

Actually, the reason Black-Scholes even came about is — people who were trading options were like…

“OK, the option triggers later, but what I wanna know right now isn’t book value, it’s the present value, you feel me?????”

“What the heck do we do about that~~~~~?” And while sitting with that question, Black and Scholes went ping~~ — “wait, what if we did it like this?~~” (with a whole pile of underlying assumptions, of course) — and that’s apparently how it was born.

OK so options. Two flavors: call options and put options.

And what on earth are those things?

Let’s think about it like this.

Calls and puts are rights. Cool, rights, but rights to do what?

The right to be able to say something.

Call option: “Hey! I’m gonna buy at the price we agreed on!”

Put option: “Hey! Sell at the agreed price!!!!!!!”

Each option gives you the right to say one of those things, respectively.

The thing you have the right to buy/sell is called the underlying asset, and the agreed-on price is called the exercise price (or strike price).

heh

If you’re holding a call, even if the underlying price moons~~, no need to sweat. You just trigger the call (the right) and buy at the agreed price!

(I picture the call holder yelling “I’M THE ONE WHO CONTROLS THE PRICE I CAN BUY AT!!!!!!!!!!!!!!!” while exercising lol)

Flip it for a put. Even if the price tanks hard, no need to sweat. You can trigger the put (the right) and sell the underlying at the agreed price, so you don’t have to sell at the crashed price, right????

OK, that’s the basic vibe.

Now I

wanna throw out this picture.

But — if I just chuck this picture at you with no warm-up, anyone seeing options for the first time is gonna be… a little lost.

So I’m pulling text from this old post too lolololol lolol I feel a tiny bit bad lolol

But I really don’t wanna re-describe this kind of basic stuff.

Trust me, way harder content is coming next, so don’t be disappointed —

Pulling from Financial Engineering Programming I Studied #1.

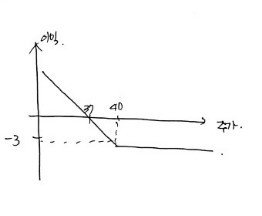

Earlier I just said “the value of an option,” but actually the value of an option apparently splits into two big buckets.

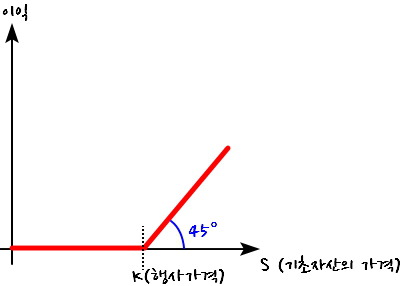

First — intrinsic value!!!

It’s simple.

The value of the gain you’d get from the option at maturity!!! That’s intrinsic value.

The intrinsic value of a call is (current underlying price) − (exercise price). That’s your profit, so that becomes the intrinsic value, right?!?!

But if the current underlying is less than the exercise price, then the option gives you exactly zero gain, right????

Like — say some underlying is sitting at 10,000 won and the call’s exercise price is 12,000 won. There’s zero reason to ever say “I’ll buy it at 12,000 won!” — like, why would you?

But if the exercise price is 8,000 won, then yeah — “Market price is 10,000 won but I’ve got the right to buy at 8,000. I’M BUYING AT 8,000!!!”

That’s what you’d say, right???? OK OK.

So the intrinsic value of a call is S − K or zero.

- The point being, intrinsic value doesn’t change continuously — it snaps to one or the other! (S = underlying price, K = exercise price)

Flip it for a put: intrinsic value of a put is K − S or zero, right!!!

If we put S on the x-axis and profit on the y-axis and graph it, starting with the call:

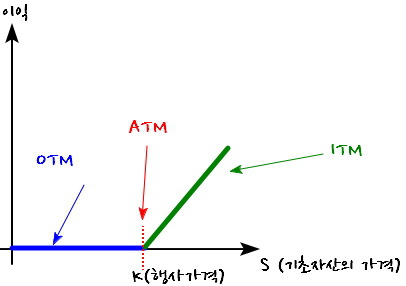

It looks like that — the shape depends on whether the underlying is past K or not!

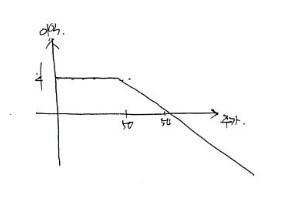

Right now, if the underlying price is

- below K → out-of-the-money (OTM, the no-profit zone)

- above K → in-the-money (ITM, the profit zone)

- exactly at K → at-the-money (ATM, right on the boundary)

Apparently those are the terms people use to describe the state.

The picture above is for a call.

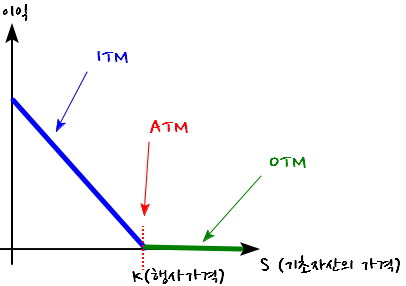

For the put case, you can totally figure it out yourself, so I’m not gonna blabber about it.

There you go, heh.

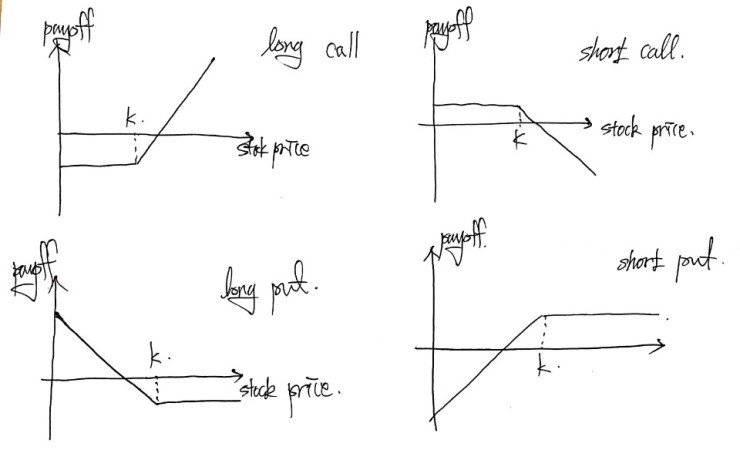

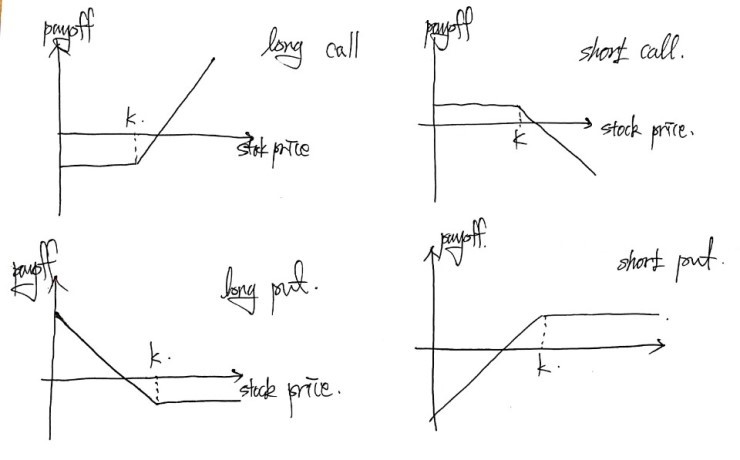

Now, the payoff at maturity for: buying a call (long), selling a call (short), buying a put (long), selling a put (short) — i.e., the picture of “intrinsic value”:

Can I confidently throw this picture out now????

Gain on a call: $\max(S_T - k, 0)$

Gain on a put: $\max(k - S_T, 0)$

The fact that it works out like this… just writing those two lines is basically all the explanation needed, right???

What’s max(), you ask? It’s a function — pulls out the bigger of the two values.

OK, before we move on, let’s mention a few details. Nothing too heavy.

First! Where does one even go to buy these option-type derivatives??

Chicago Board Options Exchange, NASDAQ OMX, NYSE Euronext, International Securities Exchange, Boston Options Exchange, and on and on…

Also — one option contract = the right to buy or sell 100 shares of stock.

(Stocks are apparently traded in lots of 100 anyway… it’s not that options are weirdly special.)

Also, are options only on stocks?!?!?

NO NO NO NO NO

There are also currency options, where you bet on foreign currency in units of 10,000 (for the yen it’s 100,000 (one hundred thousand) units).

Currency options get covered in chapter 15.

Not just currency — there’s also index options where, just like with futures, you bet on an index.

S&P 500, S&P 100, NASDAQ 100, Dow Jones Industrial Average… and on and on.

Oh, and then there’s the whole American vs. European options thing…

These details are so absurdly varied I can’t possibly cover them all comprehensively.

But — since European options have to exist first before American options can exist on top of them,

people apparently say: “Oh? They’re selling American options? → Then European options on this thing definitely also exist.”

Depending on the product, sometimes American options exist, sometimes they don’t,

and if American options do exist, then since European has to exist first, that means European is also there…?

Anyway, what I’m trying to say is — there are a heckin’ lot of kinds of options.

And honestly, beyond the ones I just mentioned, there are options with truly bizarre shapes and weird-as-hell conditions out there…(T_T)

But from here on, instead of those exotic ones, the goal is to draw the big picture? of options using the most standard kind — stock options, where the underlying is stocks.

Index options and currency options will come up later… heh.

The next chunk of content explains the cycle in which options are traded,

and there’s stuff like — if the stock price is between $5 and $25, the strike intervals are $2.50; between $25 and $200, the strike intervals are $5; above $200, the strike interval is $10 — that kind of thing.

I recommend you just skim that part on your own ;; heh ; heh

(I’m correctly avoiding it because I might say something wrong, given that I have literally never worked in the industry.)

OK a few more terms, let’s go.

First, option class.

Simply: “all the call options and put options on the same underlying asset.” That’s an option class.

So when a new option on a new underlying gets listed, you can say “a new option class has been added?!?!?!”

There’s also option series.

This one is: “options within the same option class that also share the same exercise price and same expiration date” — bundled together as

an option series, apparently.

Oh, and ITM, ATM, OTM should technically be covered here, but I already covered them above, so we move past.

Dividends & Stock Splits

To not get confused, let’s just pretend OTC (over-the-counter) options don’t exist for this discussion. Way too many cases.

Hmm — it seems options traded on current exchanges do not adjust for cash dividends.

(Except in extreme cases where the dividend exceeds 10% of the stock price.)

OK OK OK.

So no cash dividend adjustments — but adjustments are made for stock splits and stock dividends, apparently.

First, a stock split: it means splitting your existing shares into a larger number of shares. If they say “3-for-1 stock split,” that means 1 share → 3 shares, apparently.

Whoa!!! So the value of my shares triples?!?!?!

Nah — no no, of course not.

Because the number of shares I hold tripled, the value of each individual share has to become 1/3 of what it was — for things to come out even-steven.

(cf. Why do stock splits even happen? According to Naver’s encyclopedia, they’re used for things like: bringing an excessively-high stock price down to a level retail investors can actually buy in, in order to bump up the number of individual shareholders; or when the price has run up due to good earnings, lowering it back to a tradable range so the stock keeps moving, and so on.)

OK, let’s generalize.

Instead of 3-for-1, let’s do n-for-m.

Then m shares → n shares. So my share count becomes n/m times what it was.

So by what factor does the price need to change to keep things even?

m/n times! Right?

So when the exchange “adjusts” the option, what they’re actually doing is: multiply the option’s exercise price by m/n, and multiply the number of shares per contract by n/m. Then there’s no net change before vs. after the split, right????

That’s how the adjustment works, apparently.

Once you get this principle, the stock dividend adjustment works the same way.

A stock dividend is just issuing additional shares to existing shareholders, and it has zero impact on the company’s actual assets or earning power — so it’s basically the same thing as a stock split!!!!

Like — a 20% stock dividend is literally the same as a 6-for-5 stock split.

So the strike becomes 5/6 times, and the number of shares per contract becomes 6/5 times… let’s nail it down with a problem.

Quiz 9.6

A company has announced a 2-for-1 stock split. Explain how the terms of a call option with an exercise price of $50 will change.

The exercise price becomes $25, and the option holder gets the right to buy twice as many shares.

Prob 9.17

Consider an exchange-traded call option contract to buy 500 shares. The exercise price is $40 and expiration is in 4 months. Explain how the option terms change in each case.

a. A 10% stock dividend is paid.

: A 10% stock dividend is basically a 110:100, i.e. an 11:10 split.

So the contract to buy 500 shares becomes (11/10)×500 = 550 shares,

and the exercise price has to change to (10/11)×40 = 36.3636.

b. A 10% cash dividend is paid.

: In most ordinary cases, options apparently aren’t adjusted for cash dividends.

c. 4-for-1 stock split.

: Since 1 share becomes 4 shares,

the contract size goes from 500 → 2000 shares,

and the exercise price drops from $40 to 1/4 of that, which is $10~~~~

Margin

In stock and futures trading, you maintain a margin account. That guards against the chance that this guy might default, which protects the investor on the other side.

Same idea exists in options trading too, apparently.

But the way the margin account is operated has some differences — naturally, right??

First off — in stocks and futures, you could borrow money to fill the margin account.

(You don’t have to top up the margin account purely from your own pocket — borrowing some to fill it is generally OK.)

But in the case of purchasing options, borrowing to fund the purchase is prohibited, apparently.

The reasoning is that the option itself already contains a ton of leverage, so adding more on top is a no-go.

(For options with more than 9 months to maturity, up to 25% of the option value is apparently allowed — but file that as a side note.)

And honestly, there’s not much else to say about investors who buy options.

Why? Because these guys only hold a right, no obligation, right?

Meaning there’s no possibility of default in the first place. (No initial margin or maintenance margin like with stocks or futures.)

But — flip it. What about the position of the party issuing the option?

These guys take on an actual obligation, so a margin account has to be maintained and managed.

How the margin account gets operated is case-by-case, so it really has to be looked at case by case.

For the case-by-case details you’d be better off going straight to something like the CBOE site,

and here let’s just study the case of issuing a naked option.

Before getting into how the margin account works for naked options — what on earth is a naked option!!!!

It got translated into something like “exposed option,” but I’ll just call it a naked option.

Honestly… the true meaning of a naked option only really hits you in the very next chapter.

But I have to say something about it here, so… hmm…

For now I’ll just say:

“It’s an option in the case where you only have that one option and nothing else.”

That’s all I’ll say and we’ll move on.

When only the option exists, the initial margin gets set as the larger of the following two calculations, apparently.

<naked call option>

i) 100% of the option proceeds + 20% of the underlying price − the amount by which the option is OTM

ii) 100% of the option proceeds + 10% of the underlying price

<naked put option>

i) 100% of the option proceeds + 20% of the underlying price − the amount by which the option is OTM

ii) 100% of the option proceeds + 10% of the exercise price

That’s weird. Only for the put case, calculation ii) is based on the exercise price?

Anyway, that’s apparently how it’s done…

That sets the initial margin.

The fact that anything above the initial margin can be withdrawn — same as stocks and futures.

And the fact that if the account drops below the maintenance margin, you get a margin call — same too, apparently.

(As for what level triggers the margin call, that’s case-by-case… apparently you have to find out depending on the situation.)

OK, let’s actually do one of those calculations ourselves!!!

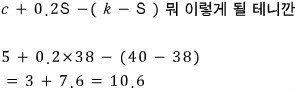

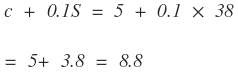

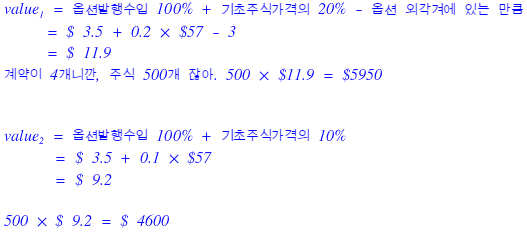

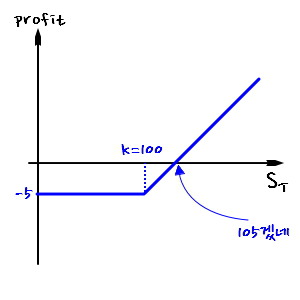

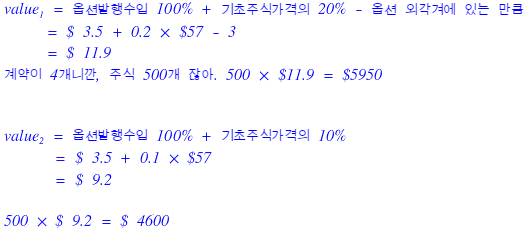

Ex. 9.5

An investor issues 4 naked call option contracts. Option price = 5, k=40, S=38.

i) First calculation:

ii) Second calculation:

(I tried using a formula tool this time, and it looks way cleaner!!! Gonna keep using it from here on.)

Now — since we said 4 contracts:

(That was the per-share calc, so multiplying each by 400 should do it.)

Let’s also try a naked put under the same conditions:

Prob 9.22

A U.S. investor has issued 5 naked call option contracts. Each option price is $3.5. Exercise price = $60, current stock price = $57. How much initial margin is required??

Calculation #1 is the larger value, so set the initial margin to that — done!

We’ve covered how the initial margin gets set!

OK, one truly final thing.

Exercising an Option

Holding an option means holding the right to exercise it, right?

So who exactly do you tell “I want to exercise~”?

The counterparty to the trade???? Hold on — in many cases you don’t even know who the counterparty is?

Right… you tell your broker, apparently.

The broker who gets that info notifies a clearing member,

and that clearing member randomly picks a member who holds a short position, apparently.

Because an opposing investor gets assigned this way, when it happens, it’s described as being “assigned.”

<Some brokers automatically exercise options at expiration if doing so is in the customer’s interest. And many exchange rules apparently stipulate that all in-the-money options are auto-exercised at expiration.>

Warrants

Options issued by financial institutions or corporations.

ex. In the case of a corporation, they apparently attach a “right to purchase stock: call warrants” to bonds.

Employee Stock Options

A call option paid out to employees as an incentive to bust their butts for shareholder benefit.

<Employees get a call where k=S, work like crazy to push the stock price up, then trigger the call, and bam — big gain, right?>

Convertible Bonds

Honestly, how many times have I had to write this thing (T_T) — pulling it over…

A convertible bond is a bond, but with a right attached letting the investor convert it into common stock at their discretion.

Convertible preferred stock is preferred stock, but can be converted into common stock at the investor’s discretion.

The interest rate on convertible bonds is generally lower than on plain bonds — because of that conversion right.

The corporation benefits because they can raise funds at a lower interest rate, and when the conversion right gets exercised they don’t have to repay principal and interest, which is also nice.

(It does mean existing shareholders’ control gets diluted, so caution needed.)

(from here)

OK problem time, let’s wrap.

Quiz 9.1

An investor bought 1 European put option for $3. Current stock price = $42, exercise price = $40. Under what circumstances does the investor make a profit?

If the stock price at maturity is below $37, the investor profits. Because the gain from exercising exceeds $3.

If the stock price at maturity is below $40, the option should be exercised.

The investor’s profit, varying with the investment, is:

Quiz 9.2

An investor sold 1 European call option for $4. Current stock price = $47, exercise price = $50. Under what circumstances does the investor make a profit?

Honestly; why would I bother putting this into words….

I’ll just explain with a single picture….

Quiz 9.3

An investor sells a European call with maturity T and exercise price k, and buys a put with the same maturity and exercise price. Describe the investor’s position.

The investor’s profit is $-\max(S_T-k,0) + \max(k-S_T,0)$.

This always equals $k - S_T$.

The investor’s position is equivalent to a forward contract with k as the delivery price.

(If you actually draw the picture, it’s a straight line of slope 1 passing through the x-intercept at x=k. But rather than going into it here, since I’m planning to hammer this in the next chapter relentlessly, I think it’s fine to just absorb “oh, you can replicate a futures contract using options!” and move on.)

Quiz 9.4

Explain why a broker requires margin from an investor who has written an option but does not require margin from an investor who has purchased an option.

Already covered above.

An investor buying an option pays the purchase cost up front.

But since they have absolutely no possibility of any future obligation, no margin is needed.

On the flip side, an investor writing an option does have a possible future obligation. So margin is required as protection against default risk.

Quiz 9.6

A 2-for-1 stock split is announced. Explain how the terms of a call option with exercise price $50 change.

The exercise price becomes $25, and the option holder gets the right to buy twice as many shares.

Prob 9.9

A European call to buy 1 share at $100 costs $5. The investor holds it to maturity. Under what conditions is the option exercised? Draw a diagram showing how the option holder’s profit varies with the stock price at maturity.

Prob 9.12

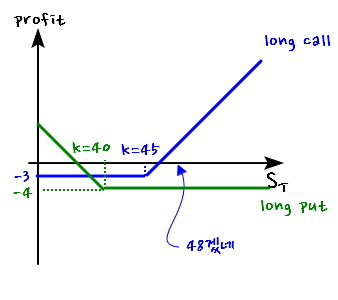

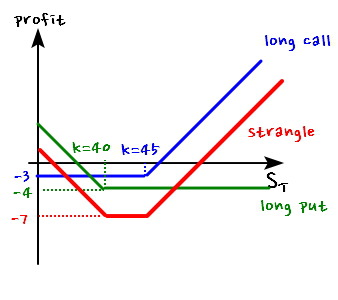

A trader buys a call with strike $45 and a put with strike $40. Same maturity. Call costs $3, put costs $4. Draw a graph of the trader’s profit vs. underlying price.

Buying a call and a put with different strikes but same maturity and underlying — that’s a strangle, and I have no idea why it’s showing up at this point in the chapter,

Anyway, the point is to add these two together:

Done;

Prob 9.13

Explain why an American option’s value is always ≥ a European option’s value when the underlying, maturity, and exercise price are the same.

Simply: the worth of having more chances to exercise (vs. a European) gets priced in.

Or putting it differently — suppose an American option were cheaper than a European one?

Then you’d just sell the European and buy the American. (Already in profit (+) before the game even starts.)

The problem? You just got the American — which already contains the European — basically for free.

So the floor for an American option’s price has to be the price of a European option with the same S, T, k;

Prob 9.14

Explain why an American option’s value is always ≥ its intrinsic value.

Isn’t this the same vibe as above?

If the time value were negative, it’d be to your advantage to exercise right now and lock in the intrinsic value.

i.e., you’d buy it cheap, exercise immediately, instant profit, right?

But if such a thing existed, the legions of arbitrageurs would’ve already cleaned it out,

so an American option with negative time value that I could buy doesn’t exist in this world.

i.e., you don’t get one either~^^

Prob 9.16

A company’s finance manager wants to choose between options and forward contracts to hedge FX risk. Explain the advantages and disadvantages of each.

Once you sign a futures contract, no backing out.

You just trade at the contracted price, end of story.

Meaning — yes, it does give you a “certain future” against an uncertain one (so financially, things become definite — like nailed-down monetary commitments).

But when you compare that contract against the uncertain world out there, the relative profit/loss can be… infinite.

An option is less of a “certain future” and more like insurance. Insurance.

If things go sideways, you just throw it away,

so there’s no downside risk — but in exchange you have to pay a premium.

Prob 9.17

Consider an exchange-traded call option contract to buy 500 shares. Exercise price = $40, expiration in 4 months. Explain how the option terms change in each case.

a. A 10% stock dividend is paid.

: A 10% stock dividend is basically a 110:100, i.e. an 11:10 split.

So the contract for 500 shares expands to (11/10)×500 = 550 shares,

and the exercise price has to change to (10/11)×40 = 36.3636.

b. A 10% cash dividend is paid.

: In most ordinary cases, no option adjustment for cash dividends, apparently.

c. 4-for-1 stock split.

: Since 1 share becomes 4 shares,

the contract size goes from 500 → 2000 shares,

and the exercise price drops from $40 to 1/4 of that, which is $10~~~~

Prob 9.22

A U.S. investor has issued 5 naked call option contracts. Each option costs $3.5. Exercise price = $60, current stock price = $57. How much initial margin is required??

Calculation #1 is the larger one, so set the initial margin to that — done!

Originally written in Korean on my Naver blog (2016-11). Translated to English for gdpark.blog.