Options: Practice Problems

Working through options pricing problems — lower bounds on calls and puts, why American options always beat intrinsic value, and when put-call parity breaks down.

Quiz 10.1

Name the six factors that move the price of a stock option.

$S_0$, $K$, $r$, $\sigma$, $T$, $D$ — stock price, strike, risk-free rate, volatility, time to maturity, dividends. Boom, six.

Quiz 10.2

Lower bound on a call on a non-dividend-paying stock?

4 months to maturity, $S_0 = \$28$, $K = $25$, $r = 8%$.

Quiz 10.3

Lower bound on a European put on a non-dividend-paying stock?

1 month to maturity, $S_0 = \$12$, $K = $15$, $r = 6%$.

Quiz 10.6

Why is an American call option always worth at least its intrinsic value? And does the same thing hold for European calls?

OK so — an American call can be exercised whenever you want. If you exercise it, you pocket the intrinsic value. So obviously the option itself can’t be worth less than that — otherwise you’d just exercise and bank the difference. Done. American call $\geq$ intrinsic value.

European calls? Different story. They can trade below intrinsic value.

Here’s the classic case: the stock pays a fat dividend during the life of the option. When that dividend gets paid, the stock price drops. And because a European call can only be exercised at maturity (i.e. after the dividend), you’re stuck holding an option whose underlying is about to take a hit. So the European call’s current value can absolutely sit below its current intrinsic value.

Quiz 10.8

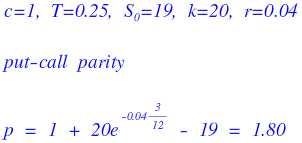

Non-dividend-paying stock at $19. A 3-month European call on it costs $1. Strike is $20, $r = 4\%$. What’s the price of the matching 3-month European put?

Prob 10.8

Why can’t we use the put-call parity argument from European options to get a similar result for American options?

OK look — for European options, both the call and the put each have exactly one moment they can be exercised: at maturity. One shot. So you can line up cash flows perfectly and the parity argument just works.

American options? Either side can be exercised whenever. We have no idea when the holder is going to pull the trigger. The cash flows don’t line up cleanly anymore, so the same proof falls apart.

That’s it. That’s all there is to say. Please don’t make me write more.

Prob 10.9

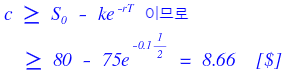

Lower bound on a call on a non-dividend-paying stock.

$S_0 = 80$, $K = 75$, $T = 6$ months, $r = 10\%$.

Prob 10.10

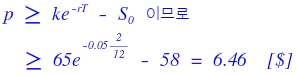

Lower bound on a European put on a non-dividend-paying stock.

$S_0 = 58$, $K = 65$, $T = 2$ months, $r = 5\%$.

Prob 10.11

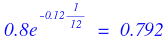

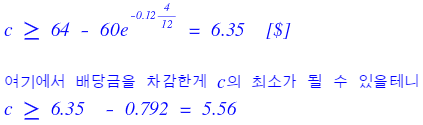

A European call on a dividend-paying stock currently trades at 5. $S_0 = 64$, $K = 60$, $T = 4$ months, $r = 12\%$. A dividend of $0.8 is expected in 1 month. What’s the arbitrage?

First, present value of that $0.8 coming in a month:

Now we also need the lower bound on the call:

Wait — the minimum the call can be is THAT, and it’s trading at 5?!?!?! The call is way undervalued!!!!

Buy the cheap call. Right now. Immediately.

So: buy one call, short the stock. My pocket goes up by $64 - 5 = 59$.

Subtract the present value of the dividend I owe in 1 month (because I’m short the stock — I have to pay it):

$59 - 0.79 = 58.21$.

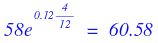

Park that at the risk-free rate for 4 months:

That’s what my pile grows to.

If at maturity the stock is above $60 — exercise the call, buy at $60, return the stock. Instant $0.58 profit, locked in.

If the stock is below $60 — even better. The more it tanks, the more I make. heh.

Prob 10.12

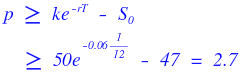

A European put on a non-dividend-paying stock costs $2.5. $S_0 = 47$, $K = 50$, $T = 1$ month, $r = 6\%$. What’s the arbitrage?

OK let’s get the lower bound of the put first:

Oh my god… the put is undervalued T_T T_T T_T T_T

So — buy the cheap put, and buy one share of the stock right now.

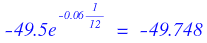

Cash out the door: $-2.5 - 47 = -49.5$. I borrowed that much to pull this off.

In 1 month I owe back:

Yeah, the loan grew T_T But — chill. I can exercise my put and sell the stock I’m holding at at. least. $K = 50$.

So worst case I clear $50 - 49.748 = 0.25$. Locked in.

And if the stock decides to moon and I can sell at the market price of $23890213890 instead of the strike of $50? Profit goes to infinity ^^

Prob 10.14

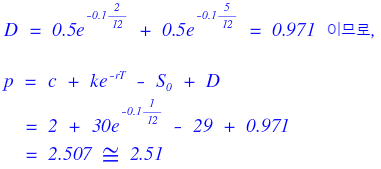

A 6-month European call with $K = 30$ trades at 2. $S_0 = 29$. Dividends of $0.5 expected in 2 months and 5 months. Yield curve is flat at $r = 10\%$. What’s the price of the 6-month European put with $K = 30$?

OK — they handed us the European call price and made a point of saying it’s European. Pretty obvious they want us to grind put-call parity.

But we’ve got dividends to deal with. And “flat yield curve” just means $r = 10\%$ no matter the maturity — one less thing to worry about.

So I’ll plug into the dividend-adjusted put-call parity. Easy. The only mildly annoying part is computing the present value of the two dividends, $D$.

Prob 10.16

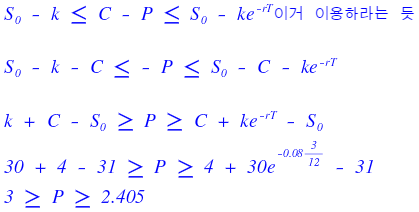

An American call on a non-dividend-paying stock costs 4. $S_0 = 31$, $K = 30$, $T = 3$ months, $r = 8\%$. What are the upper and lower bounds on the price of an American put with the same underlying, maturity, and strike?

Originally written in Korean on my Naver blog (2016-11). Translated to English for gdpark.blog.