Black-Scholes Formula: Practice Problems

Working through Chapter 13 Black-Scholes practice problems — from log-normal returns and Geometric Brownian Motion to actually pricing European call options.

Time to work through some problems from Chapter 13.

But before I dive in, there’s one thing I want to nail down first.

Remember when I said Black and Scholes baked a bunch of assumptions into their model? Stock returns following a normal distribution. Constant volatility. Constant risk-free rate. Constant dividends. No transaction costs. The whole list.

What are those assumptions actually saying, though?

I covered this back in my Monte Carlo post (Financial Engineering Programming #9 — “the more you do it, the closer you get to the average,” basically the Law of Large Numbers in disguise). Let me put it like this.

People were tearing their hair out trying to come up with a model for how stock prices move. The thing they eventually landed on — borrowed straight from physics (Brownian motion), then beaten into shape with a bunch of back-and-forth tweaking until it fit the stock market — is Geometric Brownian Motion.

Now, technically I should be talking about the Wiener process, Itô’s lemma, all that. But that’s not the point right now.

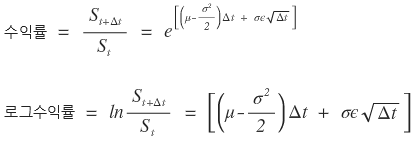

The thing to notice: that epsilon ($\varepsilon$) sitting in there is a random number drawn from a Gaussian distribution. Which means — automatically, no extra work — the log return is normally distributed.

That is,

is what it actually means!

I’m bringing this up because we’re going to need it for some of the problems below. OK, on to Chapter 13.

Prob 13.8

Current stock price is 40. Expected return on the stock is 15% per year, volatility is 25%. What’s the probability distribution of the continuously compounded return over one year?

Mean of the return distribution:

Variance:

So the standard deviation is just 0.25, right.

Prob 13.9

Current stock price 38, expected return 16%, volatility 35%.

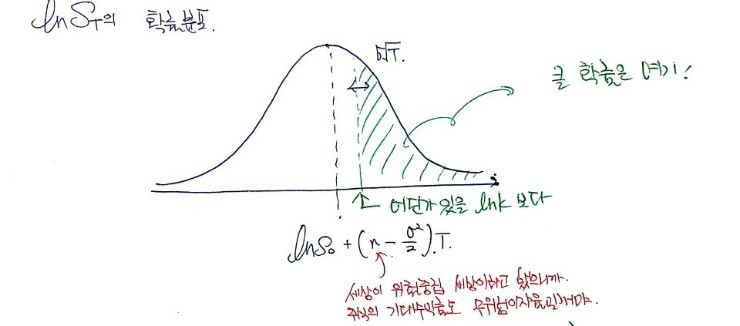

(a) What’s the probability that a European call option with 6 months to maturity and a strike of $40 gets exercised?

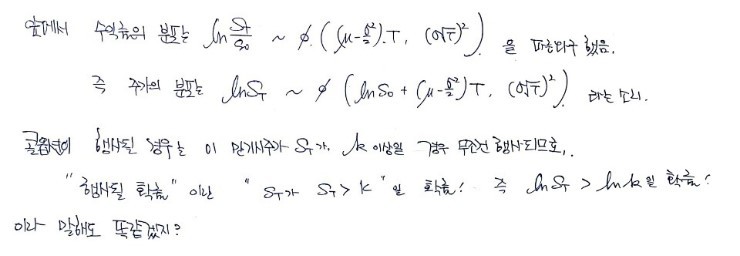

The call gets exercised when, at maturity, $S_T$ comes in higher than the strike of 40. Right?

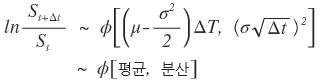

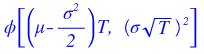

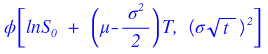

But — the distribution of $\ln(S_T/S_0)$ follows

So we can say the distribution of

is

right?

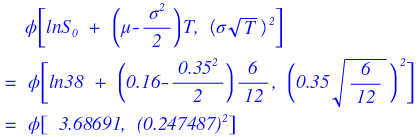

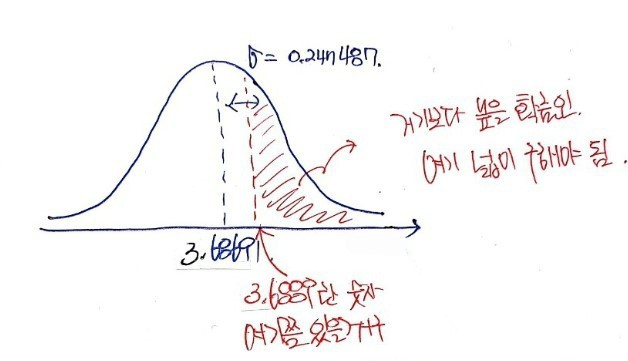

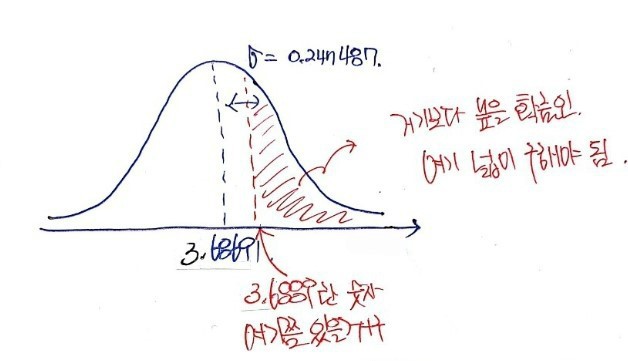

Crunching it out:

What we actually want is the probability that

is at least $\ln 40$, yeah? And $\ln 40 = 3.6889$.

From here I’m just going to drop in the photos.

Done.

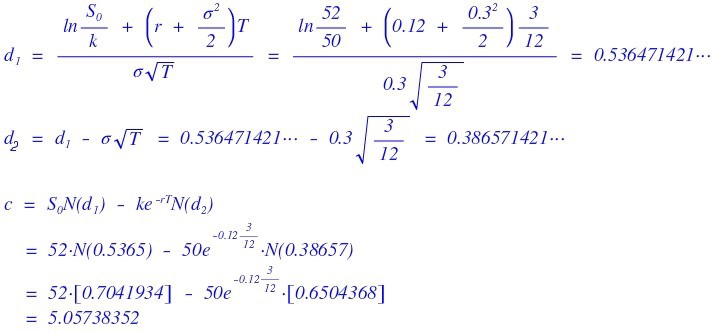

Prob 13.13

Current stock price $52, strike $50, risk-free rate 12%, volatility 30%, maturity 3 months. What’s the price of a European call on a non-dividend-paying stock?

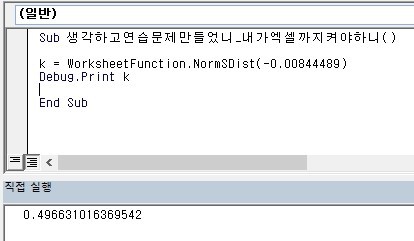

Just hit it with the BS formula!!!!

For the area under the normal distribution, I used the VBA sub I wrote a while back — you know, the did_the_textbook_author_seriously_think_I'd_crack_open_Excel_for_this() sub.

Prob 13.14

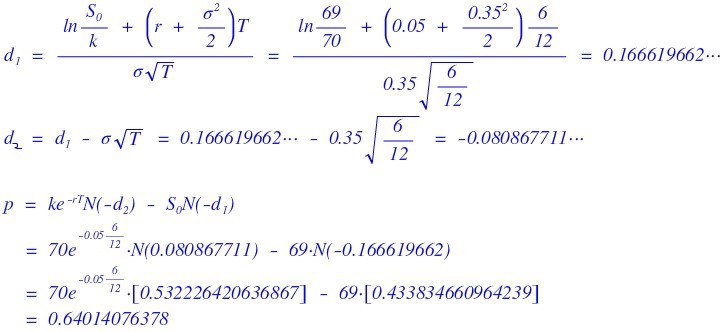

Current stock price $69, strike 70, risk-free rate 5% per year, volatility 35% per year, maturity 6 months. Price of the European put on a non-dividend-paying stock?

Prob 13.15

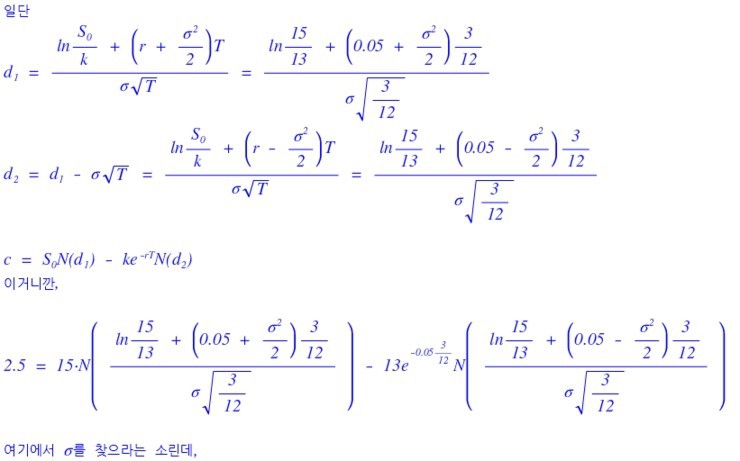

Price of a call on a non-dividend-paying stock is $2.50. Current stock price 15, strike 13, maturity 3 months, risk-free rate 5%. Find the implied volatility.

Look at it. There is no way to solve this by hand. T_T T_T T_T

That is just a fact. T_T T_T T_T T_T T_T

Go ahead, try it by hand. I genuinely respect anyone who would even attempt it…

But I’m gonna have to call it impossible. heh heh heh

So — VBA it is. Specifically, I’m going to extract the implied vol using the Newton-Raphson method, which is reputed to be the best-in-class for this.

(I wrote up the details in Financial Engineering Programming #15 — “I’m in the middle of finding implied vol, and after one round with the bisection method…” That one. Go look there for the full breakdown.)

After running it: 39.6435528596290%. heh heh heh heh heh

Prob 13.20

Show that the Black-Scholes formula for call and put values satisfies Put-Call Parity.

Already did this in a previous post!!!!

Prob 13.21

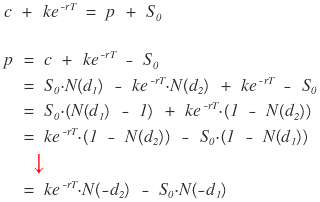

Show that the probability a European call gets exercised in a risk-neutral world is $N(d_2)$.

At time $T$, if the stock price ends up above $K$, $100 gets paid out. How do we express the value of this derivative?

Can I… just sub in photos for this one too..? T_T

So — the probability that $S_T > K$ is $N(d_2)$, and multiplying by the payout amount of 100 gives us the expected value of the derivative.

Take the present value of that expected value, and there you have it — the present value of the derivative.

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.