Stock Index Options and Currency Options

Extending Black-Scholes to handle dividends, stock index options, and currency options — turns out it's basically the same trick each time.

Using the Black-Scholes formula (now with dividends, indices, and currencies)

Last time, the underlying was a stock, and that stock was non-dividend-paying.

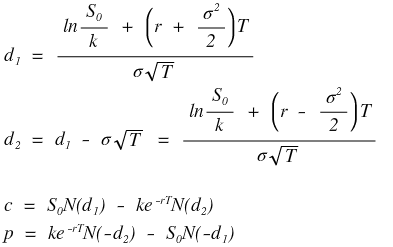

For that case, we had:

Now we’re going to push on three more cases: stocks with dividends, stock index options, and currency options. And honestly? All three run on the exact same idea (which was kind of mentioned before… so there isn’t really that much new content, heh).

OK, dividends first.

Way, waaaaaay back in some earlier chapter, we said that the exchange adjusts option contracts for stock dividends and stock splits — but not for cash dividends ;;

So what did we do about that? We said “the stock price drops by the present value of the dividend.”

Anyway — option prices get set by supply and demand too, and the equilibrium price coming out of that supply-and-demand dance has already been discounted for the dividend. So we just take that idea and plug it into the BS formula above.

Concretely: the $S_0$ from the no-dividend case,

gets adjusted to a new $S_0'$ for the with-dividend case:

Since

is the current value of the stock, “subtracting the dividend’s effect from this” means: take the dividend, pull it back to present value, and then subtract it from

So:

(D = present value of the dividends.)

With that one swap, we just use the formula exactly the way we’ve been using it. Done.

Quick example to feel it out:

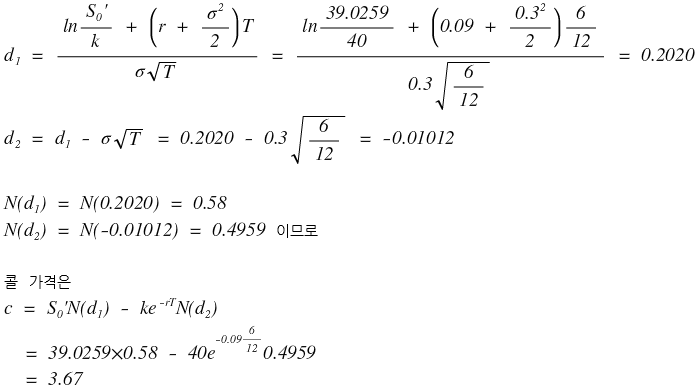

Ex. 13.6 European call on a stock with ex-dividend dates 2 months and 5 months from now. Each ex-dividend date pays $0.5. Current stock price 40, strike 40, vol 30%/year, risk-free rate 9%/year, maturity 6 months.

The present value of the dividends looks like this:

and the adjustment is:

That is,

OK, stock index options.

One contract of a stock index option is a contract on 100 times the index. The index might be S&P 100, S&P 500, Dow Jones, NASDAQ… (for the Dow it’s 0.01 × the Dow index). So if a call gets exercised you receive $(S - K) \times 100$, and a put pays you $(K - S) \times 100$. That kind of thing.

What are these good for? Insurance for your portfolio!!!

Why?????????????????????????????????????????????????????

This is something I’m planning to cover soon in the “Financial Management I Studied” series, but in portfolio theory there’s this idea that the stock index can be treated as the market portfolio. For details I’ll attach a link when I write up CAPM (Capital Asset Pricing Model) over in the Financial Management series… which I have not written yet.

Anyway, let’s go.

Say my portfolio has $\beta = 1$ and is well-diversified. $\beta = 1$ means it moves exactly with the index.

So while I’m holding my $\beta = 1$ portfolio, if I also hold a stock index put option at the same time —

then to the extent my portfolio drops and I lose money, the put cashes in and offsets the loss!!! That’s how it works as “insurance”!!!!

What if $\beta \neq 1$? Then I just hold a different number of contracts and they balance things out by the same amount, right?!?!?!!

OK, the idea is roughly clear, but let’s go quantitative with an example to nail it down.

Ex. 15.1 A manager runs a $500,000 portfolio, worried the market drops hard over the next 3 months, and wants index options so the portfolio doesn’t fall below $450,000. The portfolio tracks the S&P 500, currently at 1000.

→ My portfolio is 500,000 and the index is 1000, so my portfolio is 500× the index. So I need 5 contracts as portfolio insurance!!!!

→ Worrying about 500,000 falling below 450,000 — i.e. a 10% drop — is (because $\beta = 1$) the same as worrying about the S&P 500 falling 10%, from 1000 down to 900. So I just hold five index puts with $K = 900$!!!

→ Set up like that, let’s see what happens when my portfolio drops to 440,000. Portfolio went from 500,000 to 440,000 → so the index went from 1000 to 880.

When the index hits 880: $(20 \text{ each} \times 100) \times 5 \text{ contracts} = 10{,}000$.

The put pays out 10,000. Portfolio is at 440,000, plus 10,000 from the put = 450,000!!!!!! Floor held.

That’s the kind of thing that’s going on.

Now let’s also do the $\beta = 2$ case real quick.

I’m running a 500,000 portfolio with $\beta = 2$, current index is 1000.

I want insurance pinning my portfolio value at 450,000 in 3 months.

Risk-free rate 12%, index dividend yield 4%, portfolio dividend yield 4%.

Now we’ve got dividends in the mix, so it’s a little hairier… (T_T) Anyway, the way to think about it: what we need is — at the moment my $\beta = 2$ portfolio hits 450,000, what is the index doing~~~~~~~~~~~~~~~~~~~~~

Because that index value is what we use as the strike!!!

So: if the index moves $x\%$ → what % does my $\beta = 2$ portfolio land at? (= when does my portfolio move $-10\%$?)

We’re going to answer that. Via CAPM, naturally!!!!

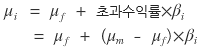

CAPM says

$\mu$ is return, subscript $f$ is risk-free, $m$ is market portfolio. Going through the whole thing here would take forever, so see the Financial Management series.

Suppose the index is up $x\%$. There’s also the 3-month chunk of the index dividend yield of 4%, which is 1%, so we use $(x+1)\%$:

From $(x+1)\%$, subtract the 3-month chunk of the risk-free rate, which is 3%. So $x + 1 - 3 = x - 2$ is the excess return. Multiply by $\beta = 2$: $2(x-2)$. Add the risk-free back: $2(x-2) + 3 = 2x - 1$. Then subtract the 3-month portion of the portfolio dividend yield (4% → 1%):

Result: $2x - 2$.

That’s exactly what my $\beta = 2$ portfolio does when the index moves $x\%$.

We want $2x - 2 = -10\%$, so:

$$2x - 2 = -10 \quad\therefore\quad x = -4\,[\%]$$So we set the strike at 960 — the index at 1000 minus 4% — and buy that option.

Options on stocks paying a dividend yield

Earlier with the cash-dividend case we subtracted the present value $D$ from the current stock price, and replaced every $S_0$ with $S_0'$.

This time it’s even easier — instead of a dividend amount, the stock pays dividends as a yield, and we assume we know that yield.

<cf. The dividend yield isn’t actually a fixed number… it’s hard to pin down even for one company, and way harder to pin down for an index that smushes a bunch of companies together. But — we just assume we know the yield $q$.>

So:

Since we’re netting out dividends paid at a continuous compounding rate $q$, the $\exp(-qt)$ feels right.

So in everything we’ve been using — Put-Call Parity, BS formula, all of it — we just swap $S_0$ for the $S_0'$ above and keep moving.

Now — why did we pivot from stock indices to “options on stocks paying a dividend yield” so abruptly?

Because back in Chapter 5 we saw that a stock index can be treated as a stock that pays a dividend yield.

So the price of a stock index option can be priced super easily by just thinking of it as “a stock paying a dividend yield.” kyahkyahkyahkyah

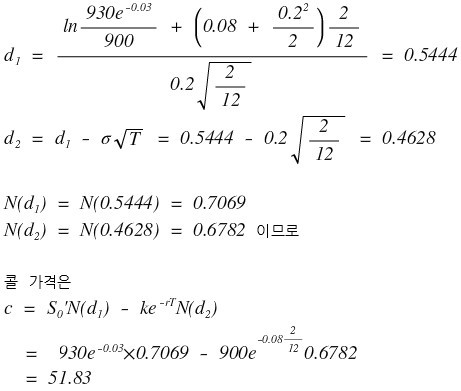

Ex. 15.3 European call on the S&P 500, maturity 2 months. Current index 930, strike 900, risk-free rate 8%, expected dividend yield 0.2% over the next 1 month and 0.3% over the month after.

So $S_0 = 930$, $K = 900$, $r = 0.08$, $\sigma = 0.2$, $T = 2/12$.

Total dividend yield over the period is 0.5%, which annualizes to 3% — so $q = 0.03$.

(Ahh… it should be $930 \exp(-0.03 \times (2/12))$, the $2/12$ is missing… (T_T) please forgive me >_< )

But… isn’t it kind of wild to just assume we know the dividend yield $q$????

There’s a trick that lets us use the same formula above without needing that wild assumption!!!!

The index forward price

has $q$ baked into it, right?????? This was also done somewhere in Chapter 5, but the forward price of an asset with no intermediate income is

and the forward price of an asset with intermediate income is

Ahh, so this is treating $q$ through the lens of “expected income.”

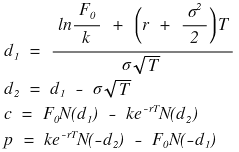

If we use this $F_0$ properly:

Plugging it in this way collapses right back to the formula we did above. So without having to assume anything about what $q$ is, we can use the BS formula (and friends) by just reading the forward price off the market — that’s the move.

OK, this “embedded $q$” — wanna try expressing it in terms of other variables?

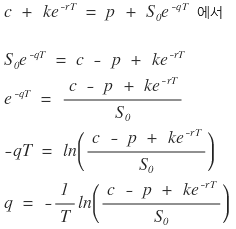

We can yank it straight out of Put-Call Parity:

Work backwards and we can track the unknown $q$ in terms of $c$, $p$, $K$, $S_0$, $T$…

Currency options

Now currency options, which were in… what chapter was that again, whatever.

If a stock index was a stock that automatically pays $q$, then a currency is something that automatically pays the foreign risk-free interest rate

— so can’t we view it as a “stock(?)” that automatically pays

as some kind of “thing” that automatically spits that out????

So in the formula we just did, drop in

in place of $q$, and boom — we’re done for currency options too…………(T_T)…………

This isn’t a cop-out… it really is that simple (T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T)(T_T) lol lol lol lol lol lol lol lol lol lol lol lol

OK. Let’s bang out a few problems and wrap up. Or… should I save those for the next post… Hmm……

Yeah — next post! lol lol lol lol lol

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.