Stock Index Options and Currency Options: Practice Problems

Practice problems on currency and stock index options — lower bounds, put-call parity, Black-Scholes puts, and hedging a portfolio with index puts.

Prob 15.9

Foreign currency is worth $1.5 today. Domestic risk-free rate 5%, foreign 9%. Find the lower bound on a 6-month call with strike 1.40.

Oh ho.

So normally the lower-bound formula is

But this is a currency option, so we have to tweak the current “stock” price a bit. The fix looks like this:

Plug that in and we’re golden.

Ugh… now I actually have to crunch the numbers;;

Done!

b.) What about the American version??????

For an American option, we just need it to be the case that you can’t make instant profit by buying and exercising right away. So — no present value, no discounting, none of that machinery is needed.

That’s our lower bound.

Which means… 0.1 (T_T)

Prob 15.10

Stock index is at 250. Dividend yield 4% per year, risk-free rate 6% per year, maturity 3 months, and a European call with strike 245 is priced at 10.

What’s the value of the 3-month put on this index (k = 245)?

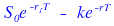

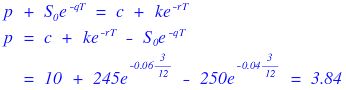

This is just “yank the put price out using Put-Call Parity.”

But it’s not the plain no-dividend stock case — it’s a stock index option, so the put-call parity looks like this:

Prob 15.11

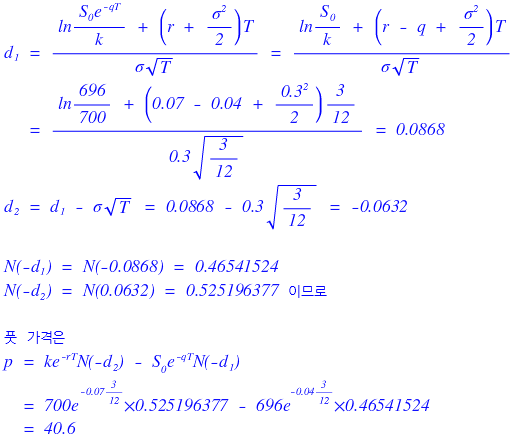

S&P 500 is at 696, index volatility is 30% per year. Risk-free rate 7% per year, dividend yield 4% per year. Find the value of a 3-month European put with strike 700.

The time has finally come.

Time to whip out the BS formula.

Prob 15.16

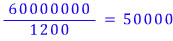

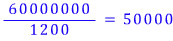

Portfolio is worth $60M, S&P 500 is at 1200. Assume the portfolio tracks the index. To keep the portfolio from dropping below $54M over the next year — what option do we buy? (Type, strike, number of contracts.)

First, the number of options:

Index options have 100× the index as the underlying, so we need 500 index option contracts.

The problem says β = 1 (a portfolio that “tracks the index well” basically means β = 1). So when $60M falls 10% to $54M, the index also drops 10%, right?

The fallen index would be 1200 − 120 = 1080, and that becomes the strike of our index option. And since we’re scared of the price falling below $54M and want the right to sell at an agreed price — yeah, put option.

So: put option, k = 1080, 500 contracts. Solved!

Prob 15.17

Portfolio worth $60M, S&P 500 at 1200. Portfolio's beta β = 2, risk-free rate 5%, portfolio dividend yield 3%, index dividend yield 3%. Keep the portfolio above $54M for the next year. (Type, strike, number of contracts.)

Still a put option, obviously.

Now let’s figure out the strike and the count.

Number of contracts:

…and we multiply that by beta. So 1000 contracts.

Now for the strike. If the index moves by x%, we tack on a year of dividends at 3%: x + 3 [%]

Subtract a year of the risk-free rate at 5%: x + 3 − 5 = x − 2 [%]

That’s the excess return, so multiply by β: β(x − 2) = 2(x − 2) = 2x − 4 [%]

Add back a year of the risk-free rate: 2x − 4 + 5 = 2x + 1 [%]

Subtract a year of the portfolio’s dividend yield: 2x + 1 − 3 = 2x − 2 [%]

Now find the x that drives the portfolio to −10%:

$$2x - 2 = -10$$$$x = -4$$There we go!

The index level at −4% from 1200: 1200 − (1200 × 0.04) = 1152.

That’s our index option strike.

So the whole thing: put option, 1000 contracts, k = 1152.

Prob 15.18

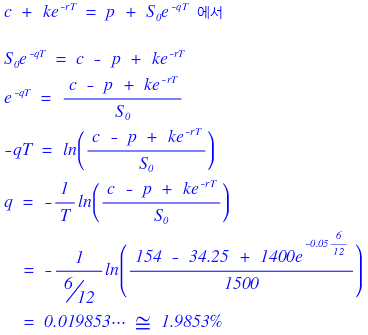

Index is at 1500. A European call and put, both strike 1400, both 6 months to maturity, are priced at 154.00 and 34.25 respectively. Risk-free rate is 5%. What’s the implied dividend yield?

This came up in the previous post.

We extracted it using Put-Call Parity. Honestly, let me just paste it in, heh.

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.