The Greeks

A casual walkthrough of why hedging exists and a few 'dumb' strategies before the real stuff — delta hedging — explained like chatting with someone in the field.

What we’re covering today: hedging.

Hey!!! You did it, didn’t you?!?!

Nope~~~ I didn’t~~~

Not that kind of “did it.” I mean hedge, hedging. Sorry.

OK so~~~ here’s something I heard from someone actually working in the field.

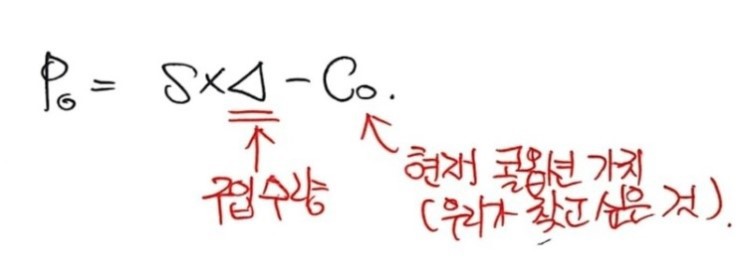

Say you sold an option for 100,000 won.

Now using whatever conditions are currently floating around — stock price, volatility, risk-free rate, expected return, etc. (apparently each company has its own manual for pulling these numbers out) — using those, you calculate the theoretical value of the option you just sold and it comes out to 80,000 won.

So from the company’s point of view, congrats, you just made 20,000 won of profit.

Except… that 20,000 won isn’t realized yet. It’s profit that only actually lands once expiry hits.

So from this point on, the financial engineer’s whole job becomes: protect that 20,000 won.

How??? “By hedging.”

OK so that’s the context we’re learning hedging in, and the most basic flavor is delta hedging. That’s what I really want to dig into. But before that, let’s run through a few dumb hedging methods first.

Dumb hedge, Episode 1: do absolutely nothing

You just go ahead and do absolutely nothing. Fiercely.

But surprisingly this has its merits. Hedging cost? Zero. Zero!!!

May the energy of the entire universe come to me~~~ may the gain at expiry be maximized~~~ and to maximize it further, I shall bear precisely zero hedging cost~~~~

That’s dumb hedge #1.

Dumb hedge, Episode 2: full scaredy-cat mode

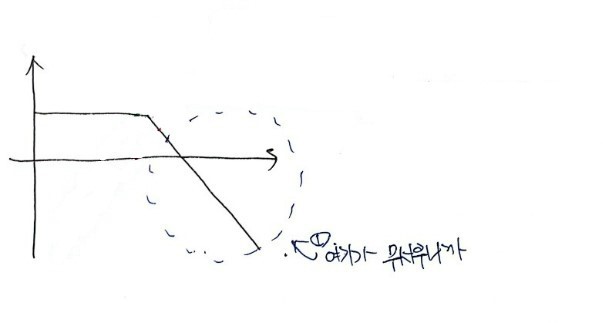

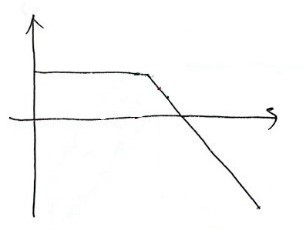

If you sold a Call option, you’re on the hook to deliver the stock at expiry, right?

So just buy the stock. In advance.

Wait, but… selling a Call and then buying the underlying — what is this;; isn’t this just synthesizing a protective put???

A picture makes it obvious.

Because this zone here, where you can take a loss, is scary —

Sure, you’d reach for this when you think the price is likely to rise~~~. In the “scary part” you’ve blocked the losses. But — in the part that wasn’t scary, you’ve now turned it into a place where you have to eat risk. lol

Anyway, that was method #2.

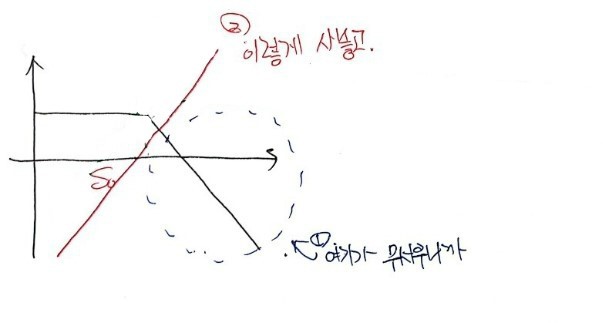

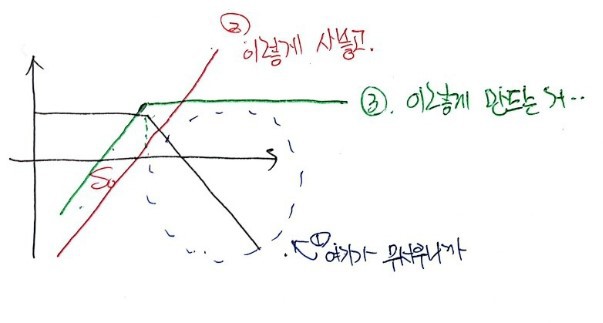

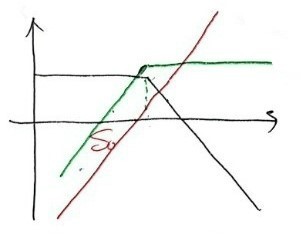

Dumb hedge, Episode 3: chase the price across k

Buy the stock only when the current price has crossed above k.

Stock price crosses above k — boom, you swiftly buy.

Swiftly turn things into the green line.

Then while the stock price keeps wandering~~~, boing!! — if it drops back below k, you swiftly sell again,

and now it looks like this.

This guy can ultimately flatten the profit curve into a horizontal line… probably the most scaredy-cat strategy of them all. lol lol

The big drawback: if the stock price goes back and forth and back and forth and back and forth around k, transaction costs alone will probably bankrupt you long before you ever “protect that 20,000 won.”

OK so what’s delta hedging then?!?!

Not dumb. Somewhat clever?!?!

Hmm. Actually it doesn’t need to be that clever. You only need to know one thing: differentiation.

These days the entire nation knows differentiation!!!!

The definition:

$$\lim_{\Delta x \to 0} \frac{f(x + \Delta x) - f(x)}{\Delta x}$$this!!!!

Ahhh I really want to ramble about differentiation for ages, but I already rambled about it once before:

http://gdpresent.blog.me/220884464906

My study of financial engineering programming #16. FDM (Finite Difference Method…

To summarize the content up to the previous post, using a roughly hacky approach to option pricing via the Black-Scholes model…

blog.naver.com

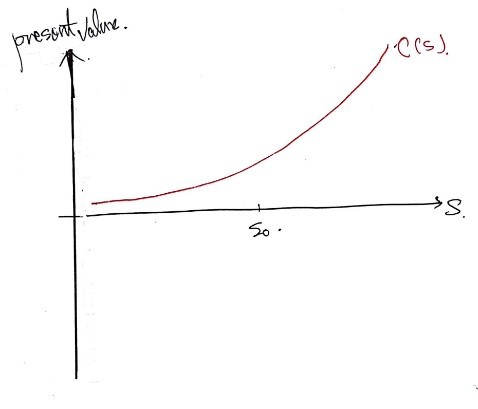

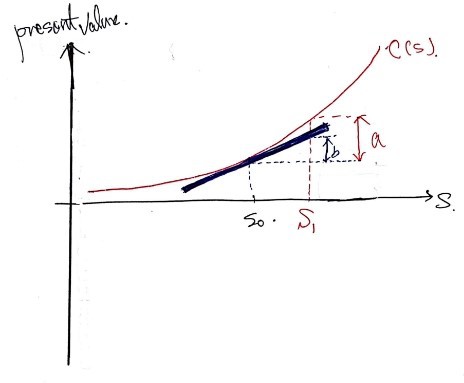

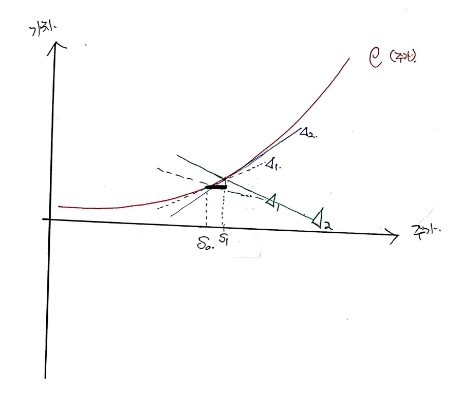

So. x-axis is S, y-axis is “value.” Function name… let’s call it $c(s)$.

$c(s)$ = current value of a call option. And let’s say the current stock price is $S_0$.

Then great — from the definition above, the rate of change of my call option’s value with respect to S, at the current price, is:

$$\lim_{\Delta S \to 0} \frac{c(S_0 + \Delta S) - c(S_0)}{\Delta S}$$What this is saying: from the current state where the price is $S_0$, when it moves by this much~~~, how much does the value of my call option move? That’s the ratio.

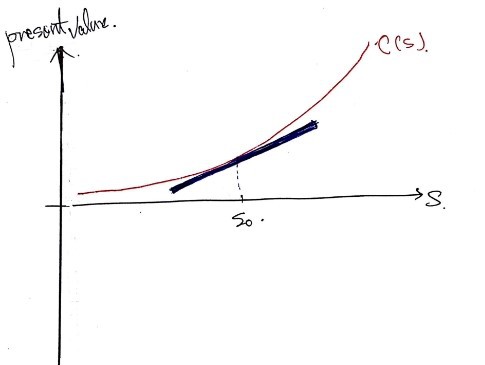

Phew… honestly this stuff is a pain to say in words. Let me switch to pictures.

Differentiation: I think it’s better to come at this with the “instantaneous rate of change” mental picture loaded up.

This diagram. (It’s the intrinsic + time value curve of a call option. I’m using the call as the example. heh)

What “ratio” is the formula above talking about?

It’s — yes yes yes yes yes yes —

the slope of this line. That’s the ratio.

So if the stock price is sitting at $S_0$ and a movement of this much~~~!~!!~~!!!!! happens, the option price moves at a ratio equal to that slope. Right???

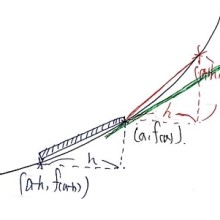

But because the option value is non-linear (i.e., it’s not a line), there’s an error.

Meaning,

when it jumps!!! to $S_1$, the actual value change is $a$ — the real change in option value. But the prediction from the first derivative says it should change by $b$ (which is almost equal to $a$).

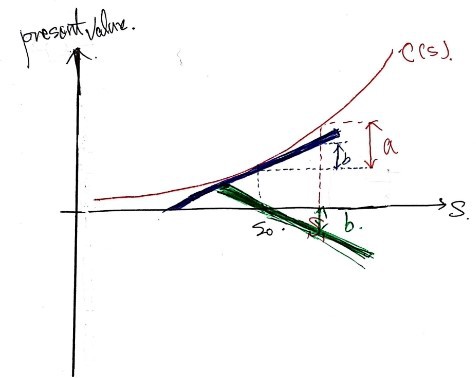

OK but now suppose we don’t want things to budge from where we were at $S_0$ (the whole “protect the 20,000 won” thing)!!!

We want to keep $C(S_0)$ right where it is. And let’s say we know the first-derivative coefficient $C'(S_0)$.

What do we do~~~ We sell stock in a quantity equal to that slope.

Why?

If we draw a graph for “selling the stock at the current price $S_0$ at minus that slope” — i.e., a line passing through the x-intercept $S_0$ at price $S_0$ — for 1 unit it’d have slope 1, but since we’re scaling by “the amount of the slope,” if we draw the line through $S_0$ with that negative slope, we get exactly what’s in the picture above!!!!

So what does this mean —

We hold option $c$. We’ve also (short-)sold the stock. Now if the price jumps from $S_0$ to $S_1$:

- the call we hold changes by $b$ (≈ $a$)

- the stock changes by $-b$

Total change in portfolio value: 0.

And of course if the stock price falls, by the same logic the portfolio value still doesn’t move.

When we built a risk-free portfolio with $c$ before — that was over here: http://gdpresent.blog.me/220885841088,

— in this kind of setup, we wrote the share quantity using the Greek letter delta, didn’t we?

Δ was the hedge ratio.

OK OK OK OK OK OK.

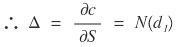

Differentiate both sides with respect to S:

$$\frac{\partial \Pi}{\partial S} = \frac{\partial c}{\partial S} - \Delta = 0$$A risk-free portfolio is, well, risk-free — so it’s gotta be insensitive to changes in S, right????

$$\Delta = \frac{\partial c}{\partial S}$$Now you can feel why we wrote that quantity as Δ back then.

So: the first-derivative coefficient is what we call delta, and delta hedging means taking a position in the underlying stock equal to that first-derivative coefficient — and boom, you’re hedged.

That’s delta hedging. And what we just walked through was delta hedging.

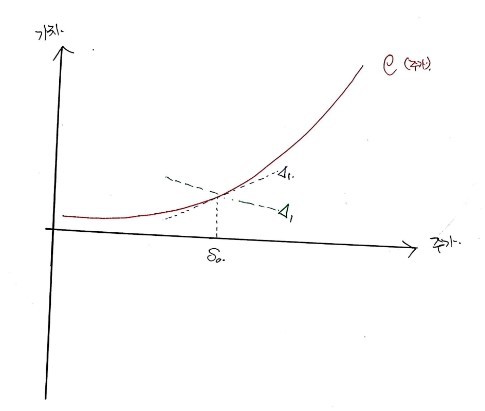

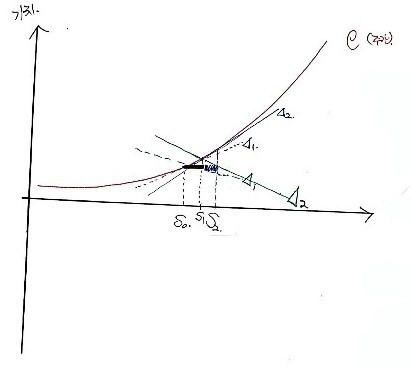

Now let’s look at it as a continuous process.

Holding $c$, the stock price was

$$S_0$$then it changes to

$$S_1$$,

$$S_2$$,

$$S_3$$,

…and so on.

While the price is hopping around like that, the question is: how do we actually do delta hedging?

First, when the price is

$$S_0$$,

we’ve sold

$$\Delta_0$$worth of stock.

When the price moves to $S_1$,

still no problem. Like the thick black line in the middle, my value stays put. (The gain on the call is offset by the loss on the stock.)

And since the price is now at $S_1$, I quickly rebalance — change the number of shares I’ve shorted from

$$\Delta_0$$to

$$\Delta_1$$.

Now even if the price wanders again from $S_1$, no worries. Wherever it goes from $S_1$, my value stays roughly fixed. Hence the extra lines next to the black one!!!!!

So in other words: we keep computing the option’s delta, keep adding $-\Delta$ shares of stock to the portfolio, and keep~~~ pinning the portfolio’s overall delta to 0.

(That is — delta hedging means making the portfolio’s delta 0. People say it’s “delta neutral.”)

Every asset has a delta. They each have a value you can get by first-differentiating with respect to S, so they each have a delta.

For stocks or futures, the profit curve is linear, so the delta is constant everywhere. The slope just doesn’t change.

But for derivatives, the value is non-linear, so the delta keeps shifting.

Since what we’re dealing with here is options, let’s actually compute the delta of an option.

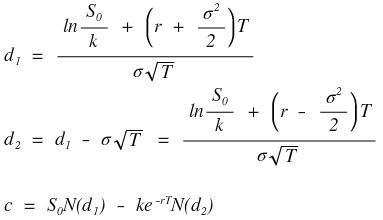

Say the red curve up there is “the current value of a European call option.” That can be written down as a number with the BS formula:

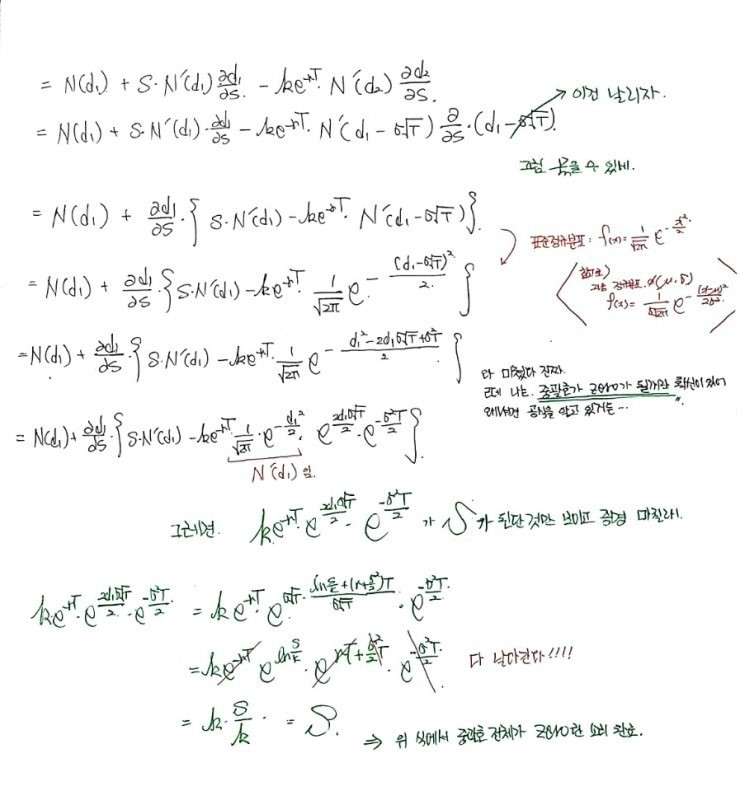

this guy — and we want its derivative. Differentiate with respect to S.

Call option’s delta:

$$\Delta = N(d_1)$$I’m sorry lol T_T T_T T_T

Using the equation editor is going to absolutely wreck my personality. lol ugh ugh ugh ugh ugh

I’ll just upload it as a picture.

But as we saw in the diagram earlier — hedging with just the first derivative can’t be perfect. Well, unless the stock only ever moves in very tiny increments, but that’s not reality.

So approximating a curve with a first-order line is kind of a stretch, and apparently sometimes people pull in the second-derivative coefficient to do hedging too.

Just like the first-derivative coefficient of the portfolio value was Δ, the second-derivative coefficient — you can also think of it as the first derivative of Δ.

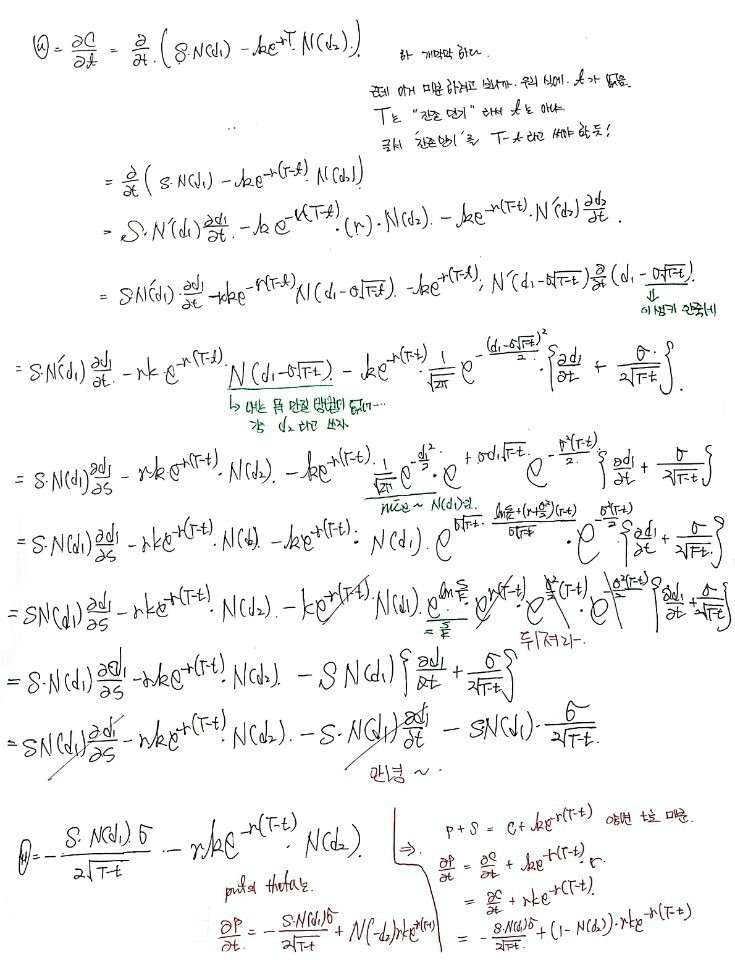

$$\Gamma = \frac{\partial^2 c}{\partial S^2} = \frac{\partial \Delta}{\partial S}$$People write this as the capital letter Γ (Gamma)!!!!!

$$\Gamma = \frac{\partial \Delta}{\partial S}$$The gamma of a call is

$$\Gamma_{call} = \frac{N'(d_1)}{S_0 \sigma \sqrt{T}}$$And, fun fact — the gamma of a call equals the gamma of a put??? Easy to verify. heh heh heh

$$\Gamma_{call} = \Gamma_{put}$$So just like we set the portfolio’s Δ to 0, we now also want to make the portfolio’s Γ neutral.

Let’s assume we’ve already gone through the procedure above to make it delta neutral, and start from there.

Right now, when we compute things: delta = 0, gamma = -3000.

Suppose there’s a call option on the market with delta 0.65 and gamma 1.5.

Its gamma is 1.5, so we deploy 2000 of those to push Γ to 0. But then this call has its own delta, which throws off the delta-neutral state we had.

0.65 × 2000 = 1240 worth of delta drift just got introduced. So to re-neutralize that 1240 of delta, just sell 1240 shares of the underlying.

Ah — and since stocks (unlike derivatives) are linear, their gamma is 0. So apparently people say stocks “have no gamma.”

Anyway, the point is: we can neutralize both Δ and Γ. That’s the story. heh heh hehehehe

But wait, S isn’t the only thing that moves

The portfolio value doesn’t only change because of S.

For options, of the 5 inputs that determine the price — S, k, σ, T, r — everything except k is moving around, so my portfolio value is wobbling on multiple fronts.

OK OK, we’ve got it covered.

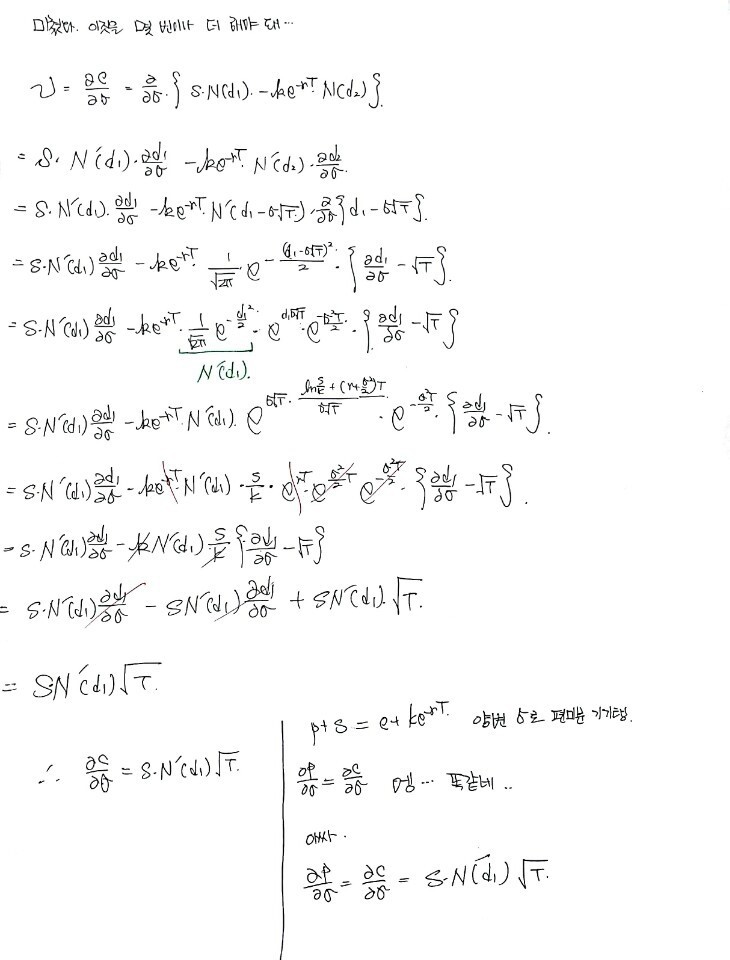

$$\frac{dV}{d\sigma} = \text{Vega}, \quad \frac{dV}{dt} = \Theta \text{ (Theta)}, \quad \frac{dV}{dr} = \rho \text{ (Rho)}$$So the full Greeks roster comes to five: Delta, Gamma, Theta, Vega, Rho.

And how do we derive the formulas for those??? Just differentiate the BS formula. lol

It’s incredibly tedious… but doable. heh

heh heh heh — all 5 Greeks confirmed.

But what I just confirmed assumes “no dividends.”

If there’s a dividend yield $q$, then like in earlier posts, you can’t just swap $S_0$ for $S \cdot e^{-qt}$ and call it done. heh heh heh heh heh heh heh

You have to take the BS formula with $S_0$ replaced by $S \cdot e^{-qt}$ and re-differentiate it with respect to S, redoing the Greek derivations from scratch.

Try it yourself ^^ It’s basically the same thing, you’ll be fine.

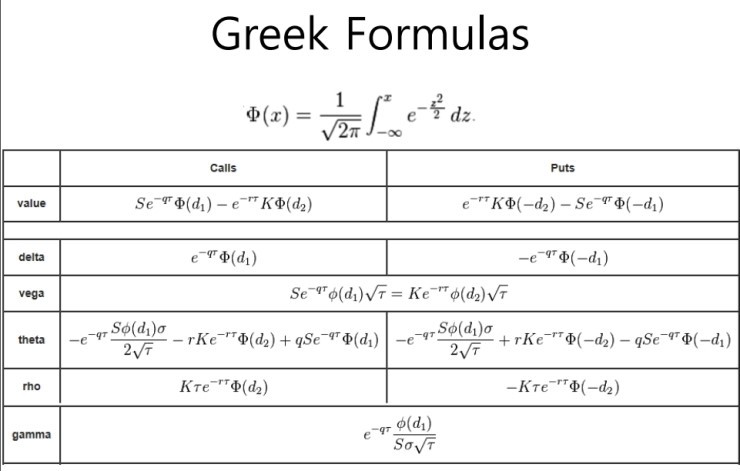

Anyway, I’ll dump the versions with those formulas written out below.

So then — does a portfolio manager have to neutralize all five Greeks?????

Probably not. Probably impossible anyway. And even if it were possible, instead of paying that hedging cost, it’d probably be cheaper to just quit your job.

So in practice at a firm, roughly:

- delta neutrality — almost always

- gamma neutrality — from time to time

- vega neutrality (for σ moves) — occasionally

- rho neutrality (for r moves) — only when the government is about to step in and start fiddling with rates

- theta neutrality — almost never… once in a blue moon??? apparently.

Bottom line, Δ and Γ are the main characters. (Since exchanges do daily settlement, neutralizing things at each moment is actually a meaningful action.)

The book has more after this, but I think reading through it once is plenty. Don’t really feel the need to summarize.

And with that — I’m wrapping up the derivatives series.

Time to crawl back to my actual major. lol This really doesn’t seem like a field I should be dipping my toes into. lol

You’ve worked hard…

I’ll just toss up a few problem solutions after this, and then bye-bye.

Zàijiàn!

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.