The Greeks: Practice Problems

Working through Greeks practice problems — stop-loss strategies, futures option deltas, and hedging a short call position on silver futures.

Problem 17.9

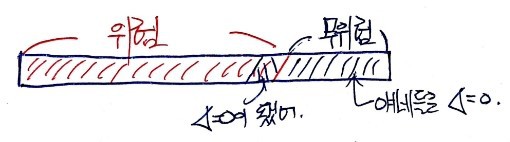

The Black-Scholes price of an out-of-the-money call with $K=40$ is $4$. The writer wants to use a stop-loss strategy — buy at $40.10, sell at $39.90. How many times is the writer expected to buy or sell?

OK so this stop-loss thing… is basically the strategy I called the least manly in a previous post. The third entry on our dumb-hedging list, lol.

Anyway — there’s a $0.10 margin built around $K$, which means every single time this person triggers a hedge, they bleed $0.10. (Try drawing it out, you’ll see.) Even with zero commissions and zero transaction costs, that 0.10 timing gap eats them alive each cycle.

Now — would anyone keep hedging once cumulative losses already wiped out the call premium they collected? You’d have to be a fool, right?

So they hedge until $0.1 \times (\text{number of times}) = \$4$. Which gives:

40 times. Done.

Problem 17.11

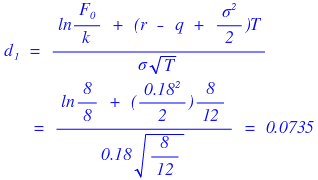

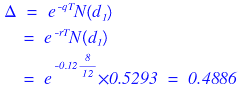

What’s the $\Delta$ for a short position of 1000 European calls on silver futures? Option expires in 8 months, futures in 9 months. The 9-month futures price is $8/oz, $K=8$, $r=12%/\text{yr}$, $\sigma=18%/\text{yr}$.

First thing to flag — this is NOT a no-dividend setup. It’s a futures!!!

Hmm. So we want the BS formula, but the dividend version. And here’s the trick: since the underlying is a futures, we stick $r$ into the slot where $q$ usually goes.

Why? Because a non-income-paying futures satisfies

$$F = S e^{rT}$$right. So treating the futures like a dividend-paying stock with $q = r$ is the move.

The dividend-case call delta is

The underlying is “the futures” now, not the stock — so I’ll just plug it in like that, heh.

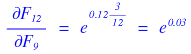

Also — the maturity that goes in here is the option’s maturity, not the futures’. So $8/12$ goes in, naturally.

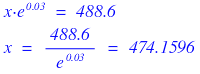

That’s the delta if you bought the call. Times 1000 → 488.6. Flip the sign for the short:

$-488.6$.

Problem 17.12

Same setup as 17.11. To delta-hedge, what initial position do we need:

- in the 9-month silver futures?

- in physical silver itself?

- in 1-year silver futures?

Why is every sub-question “if” “if” “if” lol.

Anyway — the underlying right now is a futures (not the stock we’re used to), so I’m gonna stick $F$ wherever $S$ would normally go. T_T T_T T_T

In other words — the delta of the futures with respect to itself is $1$.

So delta-hedging with the 9-month futures: go long 488.6 contracts to cancel out $-488.6$. Boom.

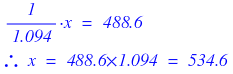

Now — if we want to hedge with physical silver instead, we need the spot delta. Our option’s underlying is the futures, so let me think about it like this:

That’d be it. And since the spot delta is the delta with respect to changes in the spot price — like this?

How many of these spot-deltas do we need to cancel $-488.6$ and produce $+488.6$?

That many.

If 1 contract = 1 oz, then 534.6 ounces of spot silver does it. If a contract is 2 oz, then $2 \times 534.6$, obviously.

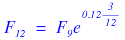

For the 1-year futures: our current underlying is the 9-month futures, so the underlying needs to be written as

heh.

The relationship between the 1-year futures and our 9-month underlying is

right?

So the delta of the 1-year futures comes out to

and the number we need is

You can just grind through it like that.

Problem 17.13

A company delta-hedges a portfolio of long currency calls and long currency puts. When does it do best?

- a. Spot rate barely moves

- b. Spot rate moves a lot

OK so they bought a call and a put… no strikes given, so I can’t tell you exactly whether it’s a straddle or a strangle. But either way — these strategies make money when the underlying (the exchange rate) swings hard. So gut answer: b.

But that’s probably not the framing the question wants. Let’s do it properly.

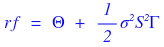

From the Black-Scholes PDE, portfolio value satisfies

In Greeks:

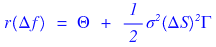

Now — they said it’s delta-hedged. So $\Delta = 0$, right?

The portfolio reduces to

Let me rewrite that in terms of changes:

Like that? And — call or put — gamma is positive, right???

So if their gamma is positive, then whatever direction $\Delta S$ goes, the $(\Delta S)^2$ term is always pumping the portfolio up. Massively, when the move is big.

→ b. Done!

Problem 17.15

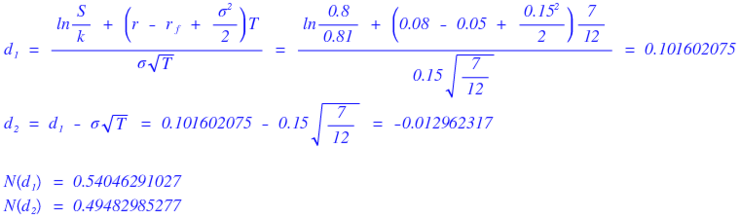

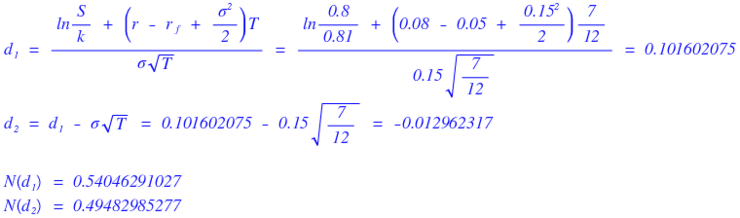

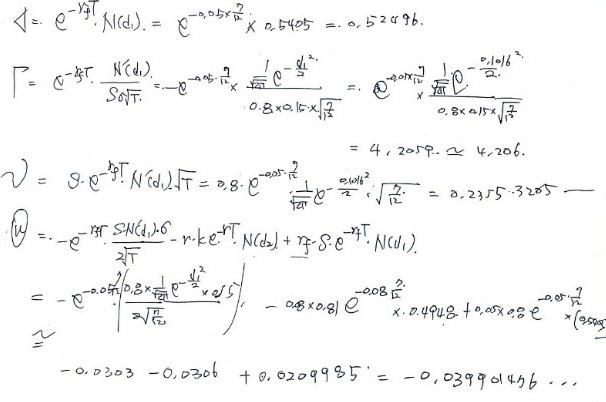

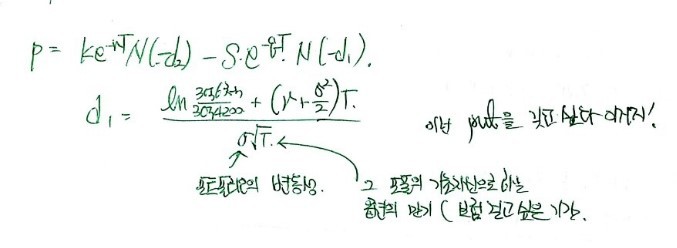

A financial institution sold 1000 European calls on Japanese yen, 7-month maturity. Spot is $0.8$ cents/¥, $K=0.81$ cents/¥, US risk-free rate is $8\%$, Japanese risk-free rate is $5\%/\text{yr}$, yen vol is $15\%$. Compute and interpret delta, gamma, vega, and theta of the institution’s position.

OK — “domestic” here is the US (the rate is quoted per yen, i.e. per unit of foreign currency, and the foreign currency is yen → domestic is the US side). The yen is the underlying.

So: $S=0.8$, $K=0.81$, $r=0.08$, $r_f=0.05$, $\sigma=0.15$, $T=7/12$.

Just plug into the formulas.

First $d_1$ and $d_2$:

I was gonna type all of this out by hand but… yeah no. T_T sorry sorry sorry.

Photo-substituting, here we go:

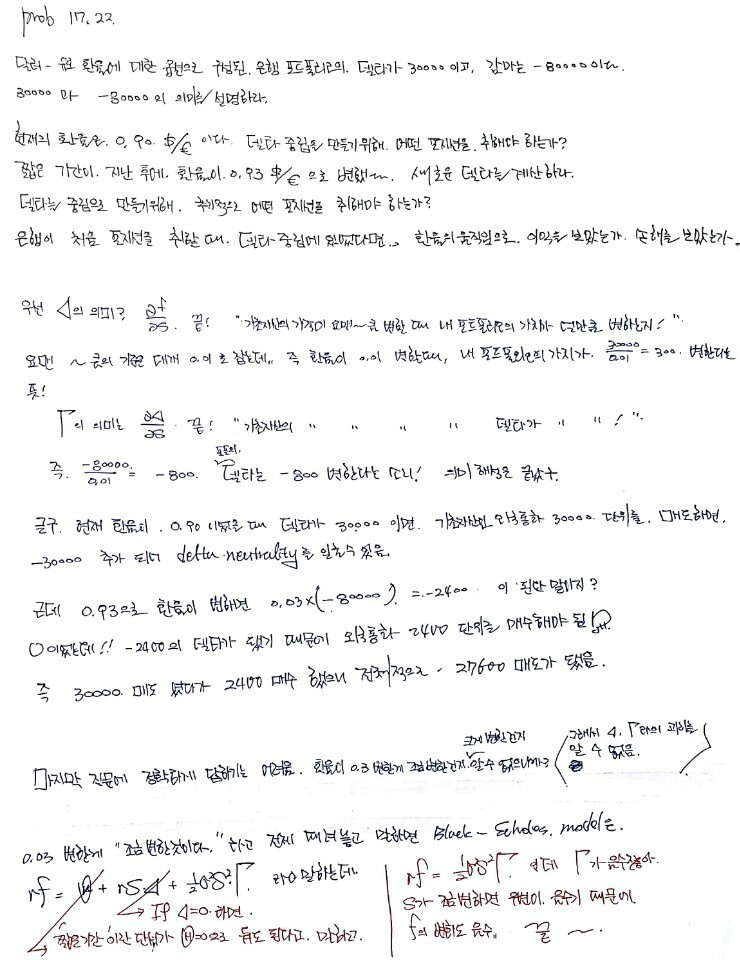

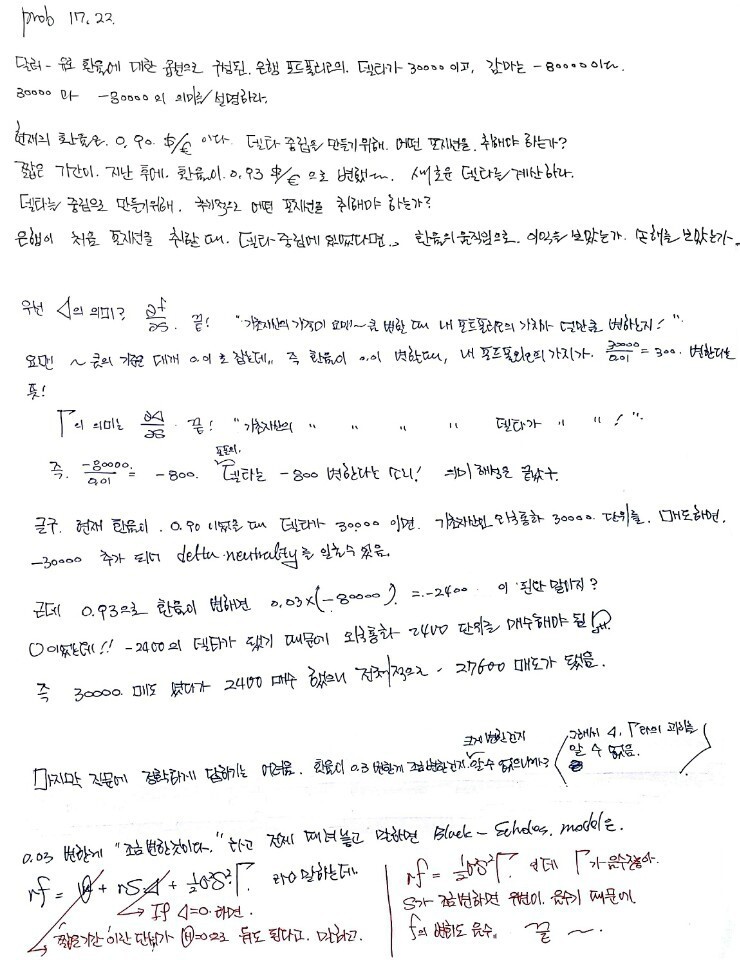

Problem 17.17

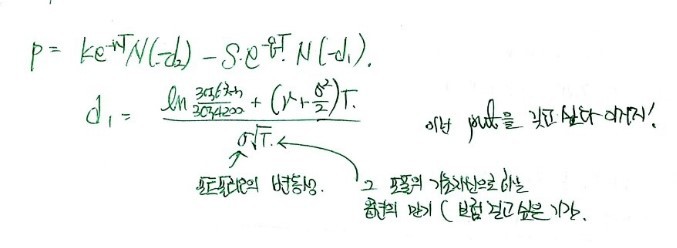

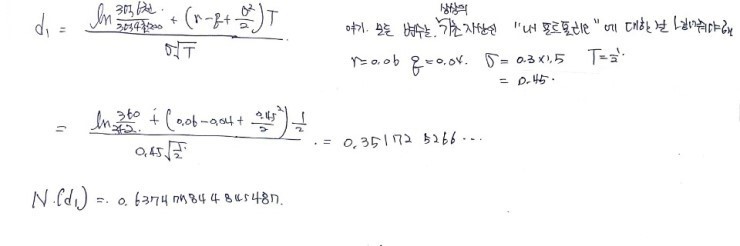

A fund manager runs a $360M well-diversified portfolio that mimics the S&P 500. The S&P is at 1200. The manager wants to keep portfolio value from dropping more than 5% over the next 6 months, using a portfolio-insurance strategy. $r=6%$, portfolio dividend yield $3%$, S&P dividend yield $3%$, index vol $30%$.

a. If the manager buys European puts, how much does it cost?

Variables first:

$T = 6/12 = 1/2$, $q = 0.03$ (index dividend), $\sigma = 0.3$, $r = 0.06$, $S = 1200$, $\beta = 1$ (well-diversified).

Cool, that’s enough.

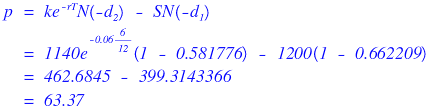

For (a) we want the put strike that prevents the portfolio from falling more than 5%. Since $\beta = 1$ and the index and portfolio dividends are equal, the portfolio hits $-5\%$ at exactly the same moment the index hits $-5\%$. That’s $1200 \times 0.95 = 1140$.

So we want puts with $K = 1140$. Pricing:

Each put costs 63.37. How many do we need?

So $63.37 \times 300{,}000 = \$19{,}011{,}000$ goes up in smoke.

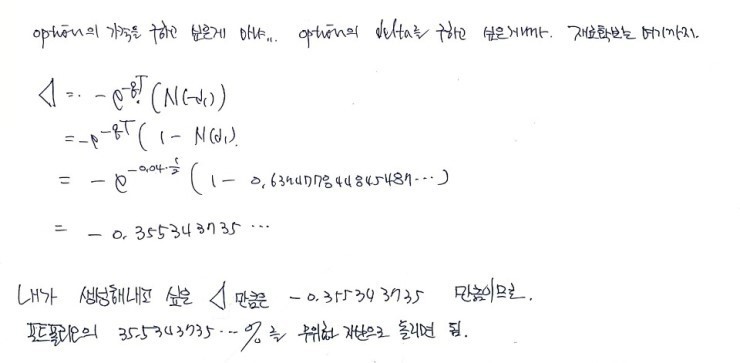

b. Replicate this with European calls.

They want the call-based strategy to behave identically to the put. Basically — turn the call into a covered call, exactly equivalent to that put.

We can do it!! Because they’re European, put-call parity straight up gives it to us!

(Honestly I don’t get why something this easy is sub-question (b). Did I miss something? T_T)

c. Use risk-free assets instead of options.

Ah, this is something we haven’t covered before. Let me sketch it briefly so we walk away with “ohh, there’s also this kind of insurance”.

The portfolio’s delta is the weighted sum of the asset-level deltas, weighted by the investment ratios of each asset. That’s how the total portfolio delta is determined, right?

In other words:

Now, this portfolio has both risky and risk-free pieces — and I’m gonna split it cleanly into exactly those two buckets. Risky and risk-free.

Risk-free assets — as the name says — are risk-free, so $\Delta = 0$, right?

Now, picture the current allocation. Suppose we suddenly move 1% of the risky bucket into the risk-free bucket:

Like turning a sliver of red into blue!

The original portfolio’s $\Delta$ was the weighted sum over the red (risky) assets’ deltas. If you move 1% of red over to risk-free… what happens?

You strip away $1/100$ of the original delta.

Whoa!! We can generate negative delta!!!

So if you move $k\%$ to risk-free, you generate a delta of $-0.0k$. Move $33.22761947\%$ to risk-free, and you’ve generated a delta of $-0.3322761947$. Wild.

But — why would we want to generate a delta of $-0.3322761947$, you ask?

OK OK OK OK OK.

Back in (a), the purpose of buying index puts was to recover losses when the portfolio takes a hit, right?

But the thing is — what this manager truly wants is not an index put. It’s a put with the portfolio itself as the underlying. With:

- portfolio current value $= 360{,}000{,}000$

- strike (the value they want to insure) $= 342{,}000{,}000$ (i.e. $-5\%$ from $360$M)

That option is

That’s the option they actually want.

But… such an option doesn’t exist. T_T T_T

(The “imaginary option” I just dreamed up actually ends up identical to the option in (a) and (d), because $\beta = 1$. We’ll deal with $\beta \neq 1$ shortly, and to keep the logic consistent there I think we need to frame it this way here too. So I’m framing it this way. T_T)

But!!! We can do something with similar effect.

We synthesize the $\Delta$ of that imagined option inside the portfolio itself — using the move-to-risk-free trick from before.

How much do we need to generate?

Which is exactly why I said what I said earlier… heh heh.

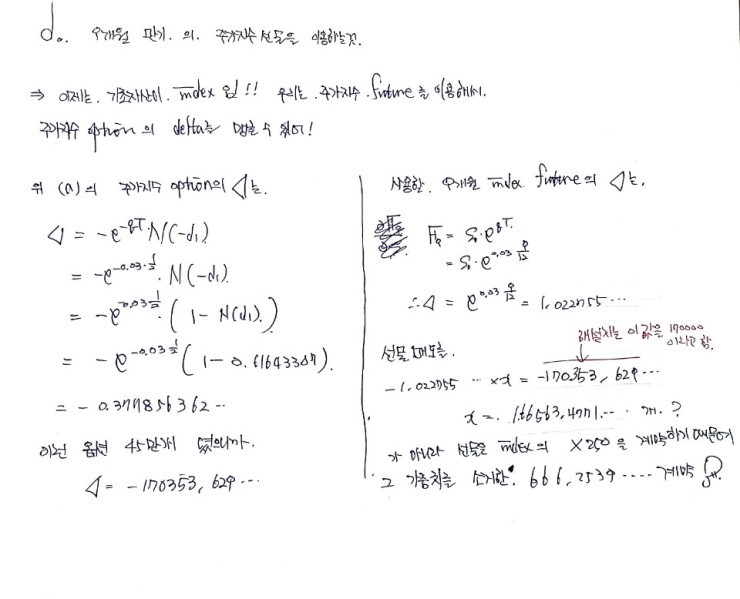

d. Use 9-month stock index futures. What’s the initial position?

Brain refresh. Now the underlying is back to being the index.

Same line of thinking. A 9-month index futures is itself a derivative, so it has a $\Delta$:

Since the futures-spot relationship is

the futures has delta:

In other words, selling one futures generates delta $-1.022755$. And how much delta do we need to generate?

As much as the options in (a) generated: $-0.3322761947 \times 300{,}000 = -99{,}828.5841$.

The number $X$ of $F_9$ contracts that gets us there:

$$-1.022755 \times X = -99{,}828.5841$$$$X = 97{,}607.52487$$So instead of 300,000 put options, we use 97,607 nine-month futures???

No no no no no.

One futures contract is on the index $\times 250$, so we have to peel out that 250 multiplier:

$$97{,}607.52487 / 250 = 390.43 \approx \mathbf{390 \text{ contracts}}.$$Problem 17.18

Same problem, but the portfolio has $\beta = 1.5$ and portfolio dividend yield = $4\%/\text{yr}$. Redo it.

So the deltas vs. 17.17 are: $\beta = 1.5$, and portfolio dividend $= 4\%$.

Variables:

$T = 1/2$, $q = 0.03$, $\sigma = 0.3$, $r = 0.06$, $S = 1200$, $\beta = 1.5$.

Let’s roll.

a.

We need the put strike. With $\beta = 1.5$, expect a very different answer than before.

I’m gonna compute the CAPM-predicted return on the $\beta=1.5$ portfolio when the index changes by $x\%$.

Take an index change of $x$. Add 6 months of the index’s $3\%$ dividend, i.e. $1.5\%$: $\;x + 1.5$.

Subtract 6 months of risk-free: $\;x + 1.5 - 3 = x - 1.5$.

Multiply by $\beta$: $\;1.5(x - 1.5)$.

Add back 6 months of risk-free, subtract 6 months of portfolio dividend ($4\%/\text{yr} \to 2\%$ over half a year): $\;1.5(x - 1.5) + 3 - 2 = 1.5(x - 1.5) + 1$.

That’s exactly the portfolio’s % change when the index changes by $x\%$.

We want this to equal $-5\%$:

$$1.5(x - 1.5) + 3 - 2 = -5$$$$x = -2.5$$There you go.

So when the $\beta=1.5$ portfolio is at $-5\%$, the index is at $-2.5\%$.

$$1200 - 1200 \times 0.025 = 1170.$$If we want to insure using index options, we want index puts with $K = 1170$.

Pricing the put with $K=1170$:

Suddenly hit by an avalanche of laziness… ugh. T_T T_T

I’ll type it up later. T_T

c.

The most ideal strategy was the put on the portfolio itself, and we synthesized something with similar effect by tweaking the portfolio’s own composition.

So let’s find the delta of that imaginary option:

Quick aside: the delta of the option from (a) is $0.377856362$.

So is the delta we actually need $0.377856362$? Or $0.355303735$?

→ To make the total assets-in-the-portfolio’s delta equal to 1, we shifted all perspectives onto the portfolio itself. If you instead anchor at the index, “delta” really means delta with respect to index changes.

In 17.17 with $\beta = 1$, both perspectives coincide. But here, with $\beta \neq 1$, I think it’s cleaner — both logically and mentally — to anchor at the portfolio and reason from the portfolio’s perspective. Even though it gets a bit fiddly… T_T

That’s how I went about it.

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.