Call Options & Put Options

A casual dive into call and put options — what they actually mean, why Black–Scholes blew the market wide open, and yes, there's a dropped-class backstory involved.

This semester I’m taking “Financial Engineering Programming.”

More precisely — it’s a class built around a book called Financial Engineering Programming Made Easy with VBA.

Actually… there’s a sad story here.

The truth is I took this class back in 2015. I’d done fine on the midterm. I even had draft blog posts written up at the time…

Back then…

Something rough hit me out of nowhere, and I just couldn’t keep my head together. I had to drop a course.

(What kind of risk do I even call this lol — I think I failed at love-risk management lololol. And now I’m taking a risk management course on top of it, so apparently I need to manage every possible kind of risk that could ever happen to me lol.)

I figured dropping it would at least save my GPA a little… so, dropped.

So the reason this first post is going up kind of fast is — yeah. It’s stuff I already studied last year.,,,

Anyway!!! Let’s get into it.

I thought the Derivatives Investment Advisor cert I casually picked up in the military would be a huge help here.

It was zero help. Absolutely zero. So I made up my mind to organize this stuff properly, and I’m going to lay it all out in writing.

Chapter 1 — please just read it on your own, however you want.

We’re starting from Chapter 2: The Value of Options.

Let me transcribe a bit of what’s in the book first, then we’ll dig in.

“Why do we need to find the (option’s) theoretical price?”

Even before this theory existed (back in like the 19th century), option trading was clearly already a thing. People back then traded options without knowing a single thing about theoretical prices.

Answer:

Back then the market was tiny. After Black–Scholes dropped, the option market exploded — it grew huuuuugely. And from then on people started using theoretical prices as guidelines when they traded.

So! That’s the historical reason we need to know the theoretical price (guideline). And honestly, the reason the Black–Scholes formula even came to exist was — well, the people actually trading options were sitting there going:

“OK, the option only activates later, but what I want to know right now is not its book value at maturity — I want to know its present value, right now, at this exact moment????”

“What do I do about thiiiis~~~”

And while everyone was stuck on that, Black and Scholes came along like:

“Booop~~ how about we do it like this~?” (with a lot of underlying assumptions, of course.)

And that, apparently, is how it was born.

OK so options come in two flavors — call options and put options. What on earth are they, exactly?

Let’s think of it this way.

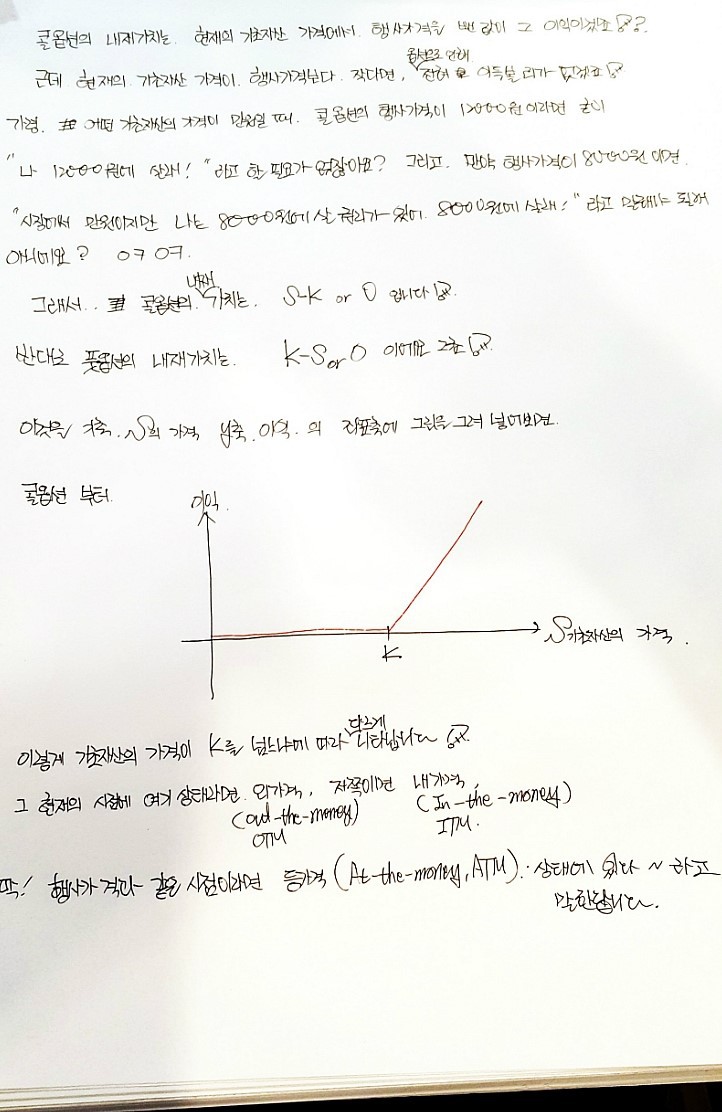

Call options and put options are rights. They’re rights — but rights to do what? They’re rights to say something.

A call option says: “Hey! I’m gonna buy this at the agreed price!”

A put option says: “Hey, sell it at the agreed price!!!!!!”

The right to say each of those things, respectively. That’s what they are.

The thing the right is about is called the underlying asset, and the agreed price is called the exercise price (or strike).

lololol

If you’re holding a call option, you don’t have to worry no matter how high the underlying asset’s price climbs. Because you can just exercise the call option (the right) and buy at the agreed price!

(The one who rules the price at which you buy!!!!!!!!!!!!!!!!!!!!!!!! seems like you could just shout that and trigger it.)

The other way around, if you’re holding a put option, you don’t have to worry even if the price keeps dropping and dropping. Even if it absolutely tanks — exercise the put option (the right), sell the underlying asset at the agreed price, and you don’t have to sell at the dropped price. Right???

So when the underlying price goes up, the call option’s value goes up and the put option’s value goes down.

And when the underlying price goes down, the call option’s value drops and the put option’s value rises!

And —

Let’s look at the other factors that determine the value of an option.

What we just covered was the price of the underlying asset.

Second, let’s pull out the exercise price.

For a call option, if the exercise price is too high there’s a strong chance the option becomes meaningless. Because the probability that you’ll ever be in a situation where you actually want to exercise gets small.

For a put option, if the exercise price is too low there’s a strong chance the option becomes meaningless. The probability that you’ll ever be in a situation where you actually want to exercise the put and sell the asset gets small, right???

Third: volatility and time to maturity.

Volatility is an indicator we’ll get into properly later. A large volatility means the price has a large chance of moving up or down by that much. And since the chance you’ll want to exercise gets bigger (options have no downside risk!!!), the value of the option goes up. That’s what they say.

Also — maturity!!!

The longer the time left to maturity, the greater the chance the price moves around by that much. So the option’s value goes up. (The intrinsic value of a put is an exception.)

The fourth and final factor is the interest rate.

In practice though, the interest rate is supposedly a not-very-important variable.

The interest rate, simply put, is the “value of money.”

Two people sign a contract: one says, “I’ll buy it at this price at maturity!” — locked in. Then suddenly the interest rate spikes.

Now the present value of that promised future payment isn’t very much. So the value of the call option goes up.

And for the put option — the value of the future sale amount they’ll receive at maturity becomes smaller. So the value of the put option goes down. That’s the story.

(Let’s say the interest rate is insanely high. You deposit 1 million won and after 1 year it’s 1 trillion won. But you locked in a call option contract at the old 1 million won price,,, whoa, the value of 1 million won at maturity = 1 trillion won but…..

Flip it around — you locked in a put option contract at the old 1 million won price. The value of 1 million won at maturity = 0.00000001 won…..

If you’d locked that in,,, whoa…… the bleeding would be brutal.)

After this, we’re going to think about the value of an option by splitting it into intrinsic value and extrinsic value (time value).

Plus a few more concepts. We’ll go through them lightly, and then based on those concepts we’ll use VBA to actually compute option values. That kind of….. lecture it’ll be…..

Hmm… right now this is the easy theory so I can explain it. But the further in we go, the absurdly more difficult the theory gets — and they compress all of it into just a few sheets of A4 with a quick whoosh — so there’s the downside that you can’t really understand the theory accurately,,,,,,

But I’ll try my best, to the extent of my strength…

Fighting!!!! lololol

Originally written in Korean on my Naver blog (2016-09). Translated to English for gdpark.blog.