Implied Volatility

Flip the BS formula backwards — plug in the real market price, leave σ blank, and whatever volatility makes it work? That's implied volatility, baby.

Last time we looked at historical volatility.

Why??? Because in the Black-Scholes model, “volatility” is assumed to be a constant, and we needed some reasonable way to estimate that constant and plug it into the formula.

So historical volatility was basically saying: “yo, let’s back out the volatility from past price data and just use that.”

But — there’s a problem.

Markets change. The character of volatility changes with the times. So if you just go grab 100 years of data and crunch it, and then claim “this number represents how the stock is moving right now”…

Yeah. That feels a little off, doesn’t it?

OK so then — how many years of data should you use???????

50 years? 30 years? 10? 5? 7.5? 2?

It’s… ambiguous.

So people started thinking:

“Hey!!!!!!!!!! What if we estimate the volatility that’s already baked into the current market option price?!”

The idea is that the option price trading right now has absorbed — implied — some value of volatility inside it.

That is,

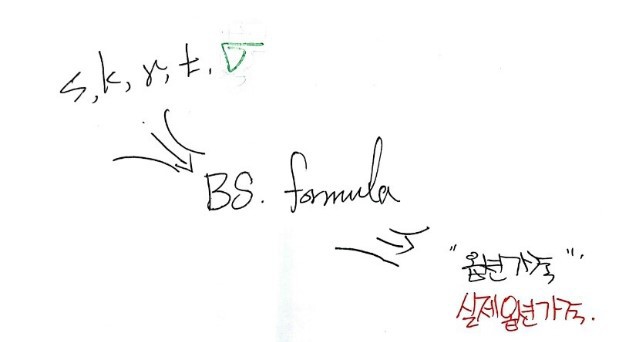

What this diagram is saying:

normally you take $S$, $K$, $r$, $T$, $\sigma$, shove them into the BS formula — boom — out pops the option price.

But now we flip it.

Leave the $\sigma$ slot blank. And in the “option price” slot, plug in the actual option price — the market price.

Then we go:

“…whatever $\sigma$ makes this equation work — whatever $\sigma$ spits out the option price the market is actually trading at — that’s the volatility of this moment!!”

That $\sigma$? That’s what we call implied volatility.

One more time, to nail it down: implied volatility is the value of $\sigma$ that, when run through the BS formula, gives you back the actual market option price.

For the record — $S$, $K$, $T$, $r$, and the option price are all easy to grab from the market.

The risk-free rate is a little ambiguous, but in Korea people mostly use the CD rate, apparently.

Haaa… but.

Unfortunately~

Unfortunately, you see… computing implied volatility by hand? Not happening.

You need a computer.

OK so how do you get a computer to do it…?

Also not trivial. There are techniques for this, see…??

That’s what we’re about to learn.

The two main ones are the Bisection Method and the Newton-Raphson Method.

We’re gonna walk through both.

I could just keep going and write them out right here, but I have a feeling I’ll be linking back to “the bisection method” and “Newton-Raphson” from future derivatives posts, so I’ll give them their own dedicated post. letsgoletsgoletsgo

Originally written in Korean on my Naver blog (2016-12). Translated to English for gdpark.blog.