Medium-Term Analysis: Labor Market

We're done with the short-term goods and financial markets — now we crack open the medium term, which means the labor market and figuring out how wages actually get determined.

OK so the short term — done. Wrapped. Finished.

We did the goods market and the financial market in the short term, and the reason we had to keep things short-term was…

honestly? Because there’s one variable that keeps moving on us.

It keeps moving, which makes life hard, but the flip side is — over a short enough horizon, that variable basically doesn’t move. So we just lock it down and go.

That variable is the price level.

(Stretch the timeline out and yeah, prices change. But today? Tomorrow? Pretty much the same number, right?)

So that’s the deal — goods market and financial market, both analyzed in the short term.

Now what’s coming up is

Chapter 6 — The Medium Term.

Let me spoil the ending first.

What market is “the medium term”?!?!

Or wait, are we just gonna re-analyze the same markets but at a medium-term horizon???

Nope. The market we look at in the medium term is neither the goods market nor the financial market — it’s the labor market.

And the reason we’re calling it medium term instead of short term is

because we’re going to loosen one of the assumptions we used in the short-term setup.

(There’s a reason we have to loosen it… scroll, scroll… heh.)

But hold on — why don’t we just go short-term → long-term and skip this whole “medium term” thing??!?!

If you’re asking that, the reason…

The reason we bother with the medium term is

because we’re going to use the medium term as a stepping stone to get to the long term. That’s why we need it.

Alright, in we go.

The short-term assumption — “the price level is fixed, and firms can produce any quantity of output at any moment” —

we’re throwing that out!!!!

The justification for tossing it: unless you really do squint at things over a short horizon, there’s no way prices stay constant.

And firms also can’t just produce any amount they feel like.

There are constraints — population, technology, all that.

So how do we even start with the labor market?

We’re going to figure out the mechanism by which wages get determined.

First thing — how wages get determined varies wildly country to country.

Some places, wages come out of collective bargaining.

Some places, the employer just decides.

Some places, wages get negotiated worker by worker, individually —

and that’s just within the US. That many ways already.

Look at the whole world and how many more would there be?!! Look firm by firm and it gets even-even-even more varied.

But — despite all that variety, apparently you can still build a “general theory” of wage determination.

Why? Because how wages get set is going to determine the prices of products.

Yeah yeah, so then how exactly do product prices get determined —

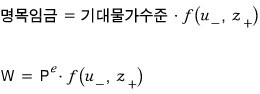

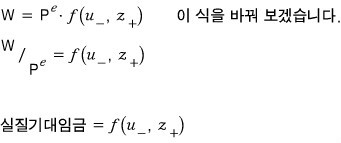

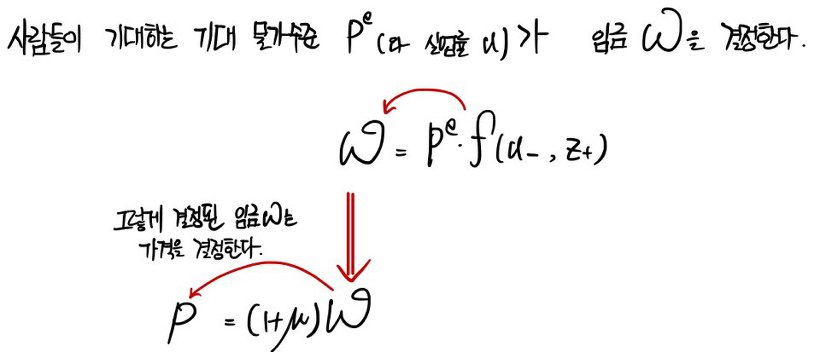

OK so let’s walk through the causal chain — why the expected price level and the unemployment rate ($u$) feed into nominal wages the way they do.

(That $z$ is a catch-all for every variable other than unemployment that affects the labor market. We just call it $z$.)

First — why are the expected price level and nominal wages in a proportional relationship??!?!?!

Hold everything else fixed, and imagine people just collectively lose it and go

“Aaaah!! Prices are about to double!!!”

Naturally those same people are gonna think:

“Uh… I’d like my paycheck to double too, thanks.”

In other words — wages get set based on the price number workers have in their heads at the exact moment~~~! the exact moment when the wage ($W$) is locked in.

So what wage determination depends on isn’t simply the price level — it’s the expected price level.

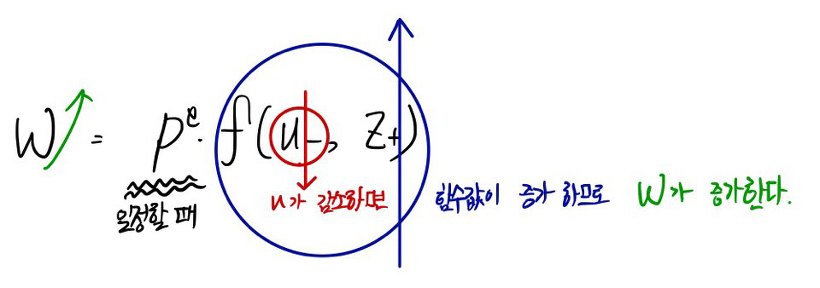

Now let’s look at the unemployment rate ($u$) in the equation above.

Why is it that when $u$ goes up, $f(\sim)$ drops, and so $W$ drops too~~~

Let me walk through why this makes sense.

Picture a wage negotiation happening when unemployment is high.

From the worker’s side — unemployment’s high, and if they don’t lock in this job they’re cooked,

so even if the firm lowballs them they kinda have to take it.

That just hollows out the worker’s bargaining power.

In other words, when unemployment goes up, it makes total sense that firms will quote lower wages — that’s just them doing what firms do, chasing profit.

(Makes sense. Also a bummer. That’s reality.)

The reverse case — you get it without me spelling it out, right?

The figure is a rough sketch of what happens when unemployment falls.

Like I said, $z$ is a catch-all for every other variable besides unemployment.

If you broke it apart and went one by one, there’d be a huge number of them,

and some would be in a $(+)$ relationship with the function, some in a $(-)$ relationship.

By convention we just define it as a $(+)$ relationship, apparently.

What kinds of things go in there — the $(+)$ side includes: unemployment insurance, the minimum wage, dismissal regulations, the political situation, etc.,

but we’re not going at this quantitatively so let’s just move on.

Unemployment is our main character!!!!!

OK OK OK OK OK.

We’ve got wage determination down.

We pinned down the variables firms use to set wages, and we pinned down whether each one moves with $W$ proportionally, $(+)$, or $(-)$.

So now, building on this — let’s think about how firms set the price of a product.

The reason we do wage determination first and price determination after is

because, apparently, the wage that gets set → has a massive influence on the price that gets set.

Let’s get into the firm’s head.

Picture us as the execs at GD Corp.

We need to set the price of our product, and obviously we’re not going to just pick a number out of a hat — at minimum we want to leave a Margin!!!!!

So at the absolute floor, we set it higher than what we paid to make the thing. (Gotta eat.)

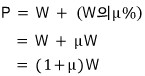

In other words, price ($P$) depends on cost. That’s the punchline.

And “cost” can be rephrased as: how much labor went into making this thing~~~~ right?

And “how many did we make!!!” — that’s the quantity produced.

Which means quantity produced is going to be proportional to labor hired.

That is,

The proportionality constant $A$ means “how many units does 1 unit of labor crank out.”

If your team is sharp, $A$ is big. If your team is, uh, not so sharp, $A$ is small.

Anyway $A$ has that kind of meaning, but let’s just assume $A = 1$.

This is the assumption that the labor a firm adds (or sheds) and the output that comes out of it are directly proportional.

In other words!!! The assumption is: the extra cost a firm eats when it bumps output up by one unit is exactly the wage of 1 unit of labor.

(Implicit assumption… raw materials… and every other cost like that, we’re just deciding to ignore.)

Which means the wage $W$ is the marginal cost of the product, right!!?

OK OK, from microeconomics, (in a perfectly competitive market) the price $P$ equals the marginal cost of one unit of output.

So $P = W$, like that.

But firms are gonna stack juuuust a liiiittle margin on top of that.

We’ll express that margin as “what percentage of marginal cost it is.”

That whole long ramble was just to land on writing it like this. (crying) (sob sob) This is hard.

Yep — that $\mu$ is called the Mark-up.

Everyone’s heard the word. It’s all over the place.

It shows up not just in macro but in plenty of other corners too, so file it away.

So with that, we’ve covered how firms set the price $P$.

And turns out — it depends on the wage $W$!!!! heh

Let me wrap up what we’ve done so far.

Originally written in Korean on my Naver blog (2016-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.