Short-Run and Medium-Run Analysis with the Real Interest Rate

We patch up the IS-LM model to use r instead of i, then show why the medium-run always lands at Wicksell's natural real interest rate r(n).

Now that we’ve got the real interest rate down, the first thing we need to do is patch up the IS-LM model.

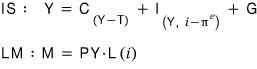

The IS curve — the one that says “goods market in equilibrium” — we derived back in Chapter 5 like this:

That’s how we got it.

Now, strictly speaking,

this is wrong.

Because — this is the goods market, right?

When people are deciding whether to invest, they’re not staring at the nominal rate $i$.

This is the goods market. It makes way more sense to say they’re looking at $r$.

<When you’re deciding how much to invest, you’re absolutely going to be thinking about how prices are changing too. Saying you make that call based on the nominal rate alone is a bit of a stretch.

I think it’s cleaner to put it that way.>

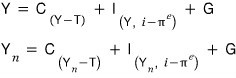

So let’s fix it up:

OK, now the LM side.

Each point on the LM curve meant “equilibrium in the financial market,” and the equation was:

This is the financial market, so saying people decide how much money to hold by looking at $i$ — that’s totally fine, right?!?!

OK, moving on.

So now our two equations look like this:

Wait — there’s literally nothing to this.

If we assume expected inflation is constant, the conclusions are exactly the same as in Chapter 5.!!!

And even if expected inflation moves around a little, it kinda feels like we could handle that without freaking out, right?

OK, let’s leave the short-run model here and move on.

Does anything change in the medium-run model?

The big takeaway from the medium-run chapter was

that the short-run change in $Y$ comes back to the potential output $Y(n)$ in the medium run — that was the punchline.

The equation above is what gives us $Y(n)$,

and to make this a little more concrete, let’s just suppose $T$ and $G$ don’t change.

Then the variables that determine $Y(n)$ collapse down to exactly~! one.

Namely, the real interest rate $r$.

And so — an early-20th-century Swedish economist named Wicksell called the real interest rate when $Y = Y(n)$ “$r(n)$,” the natural real interest rate. Apparently — that’s what the book said anyway.

Saying $Y$ adjusts to $Y(n)$ in the medium run is the same as saying the real interest rate $r$ adjusts to $r(n)$!!!!

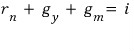

That is — what we’re saying is this:

and from there:

Also, in the medium run,

so therefore,

since we can say that’s the situation,

Written out like this, it doesn’t really click intuitively.

So let me pull in the equation we derived back in Chapter 9 and use it.

Plug this in and write it all out~~!!~~!!~

I’ll set the growth rate of the economy to zero.

“A change in $i$ in the medium run shows up as an increase in the money supply.”

Originally written in Korean on my Naver blog (2016-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.