Expected Present Discounted Value

So what's a future stream of payments actually worth right now? We walk through present value, discount factors, and interest rates — the stuff you kinda already know.

The expected present discounted value of a future flow answers a single question: what’s that expected stream of payments worth right now?

“You compute the expected present discounted value using info about the expected payment stream and the interest rate.”

Honestly… this is the kind of thing we all learned back in high school, right?

Converting future money into present value!

Yeah yeah, it’s obvious, I kinda want to just skip it — but that’d be rude, so let’s actually walk through it.

OK. Say you’ve got $P$ won right now.

If you just leave it sitting in the bank as-is,

the money grows by this interest rate.

(Strictly speaking the “nominal interest rate” should really be the rate on bonds, but I’ll just say “bank” because it’s easier to picture.)

So $P$ won becomes

won after 1 year.

Now flip it around.

If a friend is gonna pay me

won 1 year from now, then right now… how much do I effectively have??

Yeah… same as having $P$ won today.

Then if a friend’s gonna pay me $P$ won 1 year from now instead, that’s currently worth the same as having

won.

So this guy,

is called the discount factor, apparently.

It’s the thing that discounts you back to present value.

So sometimes

people don’t even call the nominal interest rate “nominal interest rate” — they just call it the discount rate~!!

OK now let’s try 2 years.

If you just hold $P$ won as-is,

that’s how it goes in general.

And if a friend pays you $P$ won 2 years out, that’s worth the same right now as

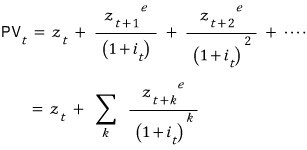

Now — what if today you get a bond coupon $z(t)$, then 1 year later $z(t+1)$, 2 years later $z(t+2)$, … and $n$ years later $z(t+n)$?!

Then the present-value equivalent works out to

!!!! (Writing this with a sigma is a little ambiguous, btw.)

OK and here’s the cool part — instead of thinking of $z(t), z(t+1), \ldots$ as bond coupons,

you can also think of them as a firm’s profits.

So: profit 1 year from now, profit 2 years from now, …

The other difference is there’s no way to actually know the interest rate 1 year from now.

So,

we end up writing it like this, and there are apparently 2 things we’re supposed to feel from this equation.

1.

The bigger this gets, the bigger PV (present value) gets.

2.

The bigger this gets, the smaller PV gets.

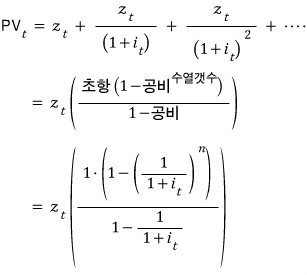

Alright, let’s keep it simple.

i) The case where the interest rate is constant at

ii) The case where both the interest rate and the payment are constant

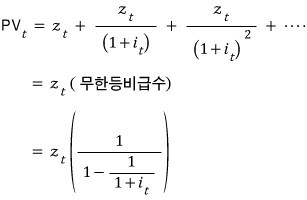

iii) The case where both are constant forever

OK, here’s something interesting.

Let me write the most general equation one more time.

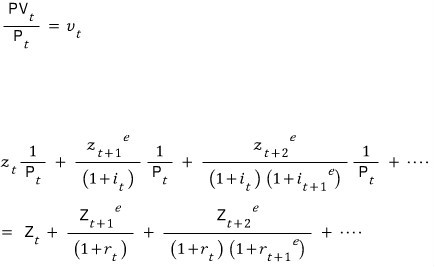

Now — the future payment doesn’t have to be money, does it!!!!

It can also be goods. Using the real interest rate (the interest rate in units of goods), the present value also gets written like this:

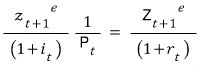

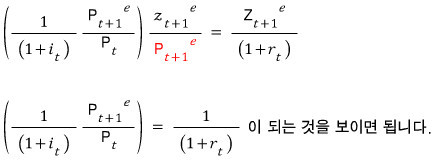

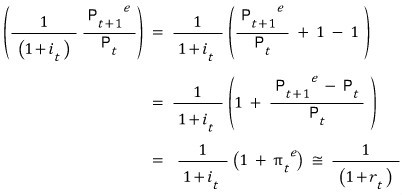

OK so the most basic nominal-vs-real relationship is “divide by the price level”:

Divide by the price level at that point in time and you get the real present value in units of goods — does this same kind of relationship hold here too??????

Apparently it works out, kinda nicely.

Let me try to prove it.

Matching up the first terms:

Way too obvious, skipping.

Matching up the second terms:

I’ll just pull one tiny trick on the left-hand side.

QED.

Originally written in Korean on my Naver blog (2016-01). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.