Perfectly Competitive Markets

A casual breakdown of perfectly competitive markets — why we bother studying a model that doesn't exist, plus a walkthrough of its four core assumptions.

OK so this time we’re finally hitting the perfectly competitive market — basically the bedrock of microeconomics.

I’ve sprinkled bits and pieces about it before, but now we’re actually sitting down with it.

Let me give you the punchline up front: the perfectly competitive market does not exist in reality.

It’s a totally idealized concept. Pure fantasy.

“Then why bother studying it, gdpark???”

Because it’s not useless! Not even close.

The trick is — you strip away every variable you can possibly strip away, you sand the thing down until it’s stupidly, ridiculously simple,

you build up an intuition there,

and then you start bolting variables back on one at a time,

and suddenly monopoly, oligopoly, monopolistic competition — all that stuff starts making sense too. heh. hehe.

There’s a saying that goes something like:

“A very simple model is an approximation of reality.”

So basically — yeah, what we’re doing here is an approximation. That’s the deal.

OK enough yapping, let’s get into it.

The assumptions

First up, the “characteristics” of a perfectly competitive market.

Honestly, calling them characteristics is a stretch — they’re really more like assumptions we’re slapping onto the market we’re about to talk about.

You’ve heard these a million times since high school econ, so I’ll just rattle through them.

1. The industry is teeny tiny!

Meaning the whole thing is chopped up into super small-scale units.

The way I read this assumption: we’re shrinking the industry on purpose so we can bake in the idea that “no single demander can push around the market demand the suppliers face.”

Whether you show up as a demander or a supplier, if just one of you enters or exits — the market doesn’t budge. Not. One. Bit.

Not even a tiny ripple!!

⟨∵ because there are waaay too many demanders and suppliers relative to the size of the industry⟩

2. They produce undifferentiated products.

Shoes are shoes! Forget Adidas, Nike, Puma — just think “shoes.”

That’s the vibe.

In high school they teach it like that, but the book I’m reading uses a really nice example:

fresh roses.

You’ve bought roses at least once on Rose Day, right?

When you bought them, you weren’t standing there going “hmm, are these American roses, Korean, Gangwon-do, Chungcheong-do?” You just thought,

“yep, roses!!” Right?

3. All suppliers in the market have “perfect information about price.”

So these suppliers — who are pumping out undifferentiated products and can’t even nudge the price — they all know the exact same stuff.

Which means profit per unit is the same for everybody… and so on.

Basically, if you take “suppliers are all on the same footing” and dress it up sociology-style, you end up saying “they all share the same information.” Same idea.

4. Equal access to resources.

Anyone can copy the technology, anyone can walk into the market freely.

Same conditions for everyone, of course.

So everyone has equal access to the factors of production.

So what does all that buy us?

A market built on those four assumptions — here’s how you summarize it.

I’ll say it the econ way:

Suppliers and demanders are all price takers.

Remember how I said one of you entering or leaving doesn’t shift the market at all? Yeah — that means the price, which is one of the given conditions of the market, is something both suppliers and demanders just have to accept.

You can pull whatever stunt you want. You’re not changing the market price.

Law of one price.

The “price you have to accept” we just talked about? It’s the same price in Seoul, in Incheon, in Gangwon-do, in Chungcheong-do —

heck, even in America.

Why? Because on top of selling totally undifferentiated products, all the price info about them is completely free!

⟨Try being a maniac and selling above the market price? Nobody buys. Try being a maniac and selling below it? You go bankrupt and get kicked out of the market eventually. The market price is the only price that can exist.⟩

Free entry.

Tech can be perfectly copied, and the factors of production are wide open to anyone —

so anyone can copy the tech, grab the factors of production, and enter the market. Right???

Profit maximization

OK, now let’s see how suppliers make decisions to maximize profit under the situation we just described.

First — profit is “total revenue − total cost = total profit.”

This is more common sense than econ, honestly!

Writing profit as $\pi$:

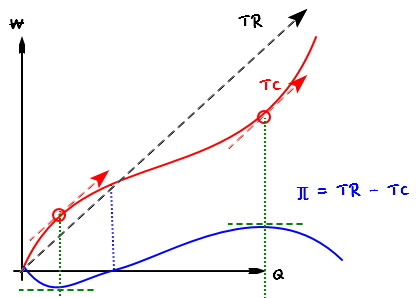

$$\pi = TR - TC$$There we go.

TR is just shorthand for total revenue,

so let’s poke at TR for a sec.

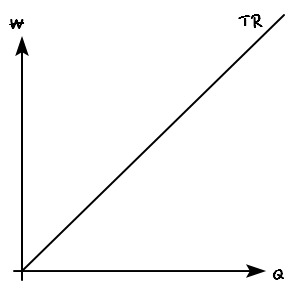

Total revenue is price × quantity sold (the transaction volume), right?

So it’s $P \times Q$.

But — in the assumptions of the perfectly competitive market, $P$ was said to be a given value.

(How it ends up being given, we’ll get to a bit later.)

So $P$ is a given constant.

Which means

it ends up drawn as a straight line like this.

Oh wait!!! Then the slope of that line is $P$!!!

$TR = PQ$, so it’s the same deal as $y = 3x$. Same idea.

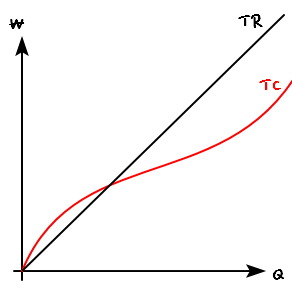

Oh wait again!!! Drawing $TC$ on the $Q$-$\$$ axes — that’s something we already covered before, right???

Let me sketch it on top in red.

Now that we’ve got both,

and remembering $\pi = TR - TC$, we can finally draw the $\pi$ function too.

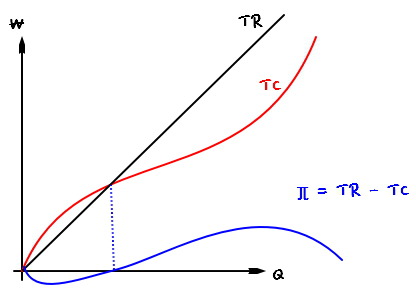

Since $\pi$ is “the difference between the two function values,” let me start by just showing that gap between them.

Oh ho??!?!

There’s a point where profit is maximized!

There’s also a local minimum where $\pi$ bottoms out, sure. But that’s not what we care about.

Let’s find where $\pi$ is maximized.

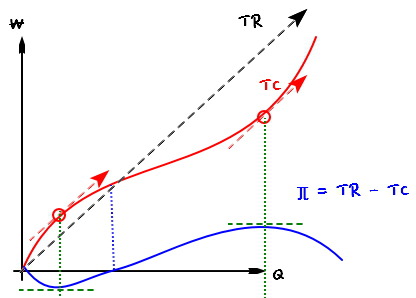

To find the max and min of $\pi(Q)$, we differentiate with respect to $Q$ and find the spot where the derivative equals zero:

$$\frac{d}{dQ}\pi(Q) \quad = \quad 0$$Let’s solve that.

Ahaaaa!!!!!

The point where profit is maximized is

$$MC \quad = \quad P$$— the spot (the point) where profit hits its peak, the very top!!!

That is, the $Q$ where the slope of $TC$ equals $P$, which is the slope of $TR$ —

at that $Q$, $\pi$ is maxed.

⟨Remember Rolle’s theorem from math class??? Rolle’s theorem is showing up here in exactly the saaame way! hehehe⟩

Originally written in Korean on my Naver blog (2016-07). Translated to English for gdpark.blog.

Comments

Discussion happens via GitHub Discussions. You'll need a GitHub account to comment.