The Money Supply Process

A casual rundown of Chapter 15 — breaking down the Fed's balance sheet, monetary base, reserves, and how open market operations move the money supply!!!

Since the course is called Money and Banking, I think we go straight through~~ from Chapter 15 for a whole semester!!!

I just followed along with the school’s syllabus

so I’m posting in that order lololol and I want to read through it again later~~~ hehehe

Alright then, heading innnnn to Chapter 15

First off, who are the characters in money supply~~~

So let’s understand money supply by looking at the Fed’s balance sheet!!!!

They say we only need to look at 4 items that are important in understanding the money supply process

Assets

Liabilities

Securities

Loans to financial institutions

Currency in circulation

Reserves

Red guys: the sum of securities + loans of these guys changes the monetary base, and thereby changes the money supply.

Blue guys: an increase in these guys means an increase in the money supply.

*** Currency in circulation + reserves = monetary liabilities, and the sum of these is called the “Monetary Base”!!!! It’s a concept that keeps coming up

Then let’s look at the blue guys first! The Fed’s liabilities.

(* Liabilities: financial obligations owed to a third party)

* Currency in circulation:

The amount of money held by the private sector, and the Fed issues this money (Federal Reserve notes)!!

Money held by deposit-taking institutions (banks) is an ‘asset’, but to the Fed, money is a liability.

“Federal Reserve notes” are the Fed’s debt certificates to the holder, and therefore, a liability.

* Reserves:

An increase in reserves increases deposits, and accordingly the money supply increases.

Red guys! The Fed’s assets.

The Fed’s assets change reserves, which changes the monetary base. So the money supply changes.

* Securities:

US Treasury securities & other securities held by the Fed

The first way the Fed supplies bank reserves is by buying bank securities.

* Loans to financial institutions:

The second way the Fed supplies bank reserves is by making loans! (borrowed reserves)

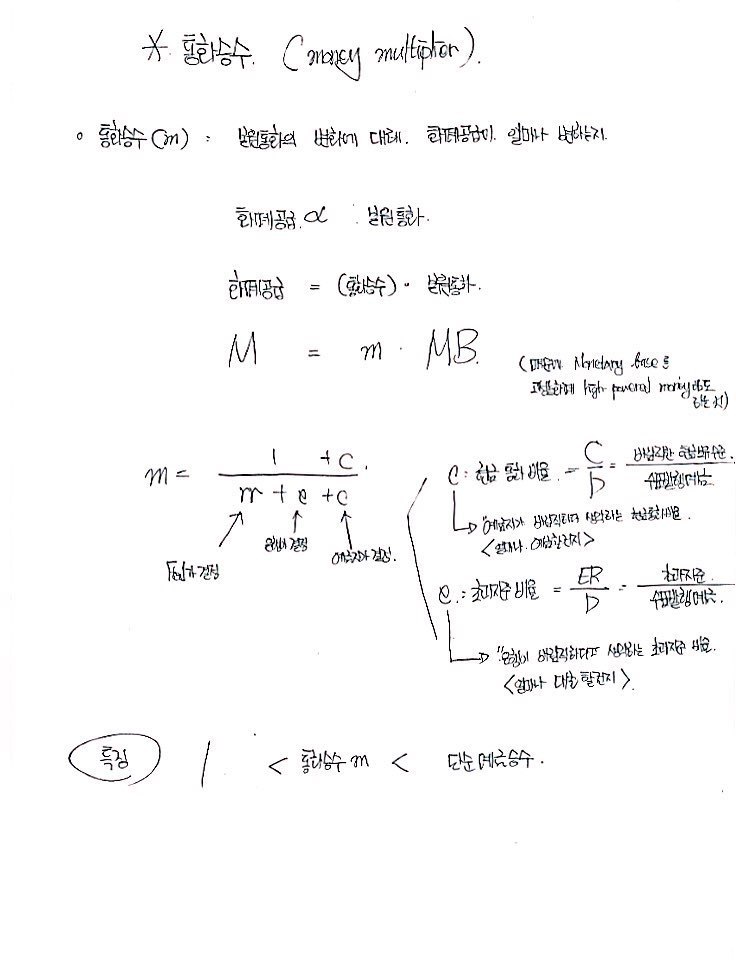

(Important) star star star: Monetary Base (also called high powered money)

C + R = {Federal Reserve notes + US Treasury money} + {Total reserves}

cf.) The US Treasury issues coins rather than bills, but because this amount is so small compared to the bills, they say we won’t worry about it going forward

Open market operation:

The Fed’s primary method of changing the monetary base — open market purchase or open market sale

I’ll handle it case by case and then draw a conclusion afterwards.

Let’s say the Fed purchases $100 million of bonds from a bank and pays by check.

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Securities -$100M

(the bank sells the securities)

Reserves +$100M

(and receives the money)

Securities +$100M

(the purchased securities came to the Fed)

Reserves +$100M

(goes up (+) by the amount paid — since we have to give the money back later! but to them, that’s a liability)

Let’s say a bank purchases a bond from an individual (institution), and the individual (institution) who sold it deposits the Fed’s check at the bank.

And let’s say the bank in turn deposits it at the Fed.

Individual

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Assets

Liabilities

Securities -$100M

(sold the bond)

Deposits +$100M

(that amount went into the bank account)

Reserves +$100M

(since it went into the bank account)

Deposits +$100M

(but that’s a liability! ‘a financial obligation’)

Securities +$100M

(that bond went to the Fed)

Reserves +$100M

(the money to be paid someday increases)

Then what if the seller who sold the bond to the Fed doesn’t go through a bank at all and just cashes the Fed’s check?????

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Securities -$100M

(sold the bond)

Currency in circulation +$100M

(receives the money directly!)

Securities +$100M

(took that bond)

Currency in circulation +$100M

(currency in circulation goes up like this on the T-account)

☞ Implication: whether it becomes a deposit or not changes the amount of ‘reserves’, but the amount of the monetary base is the same!!!!!!!

*** Let’s just see what happens to the monetary base when ‘withdrawing money’

Individual

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Assets

Liabilities

Deposits -$100M

(account balance goes negative)

Currency in circulation +$100M

(got cash!)

Reserves -$100M

(money leaves the bank’s vault..)

Deposits -$100M

(the financial obligation also goes minus ~)

Reserves -$100M

(money to be paid later ~)

Currency in circulation +$100M

(money gets sprinkled into the world)

☞ Implication: reserves change, whereas the monetary base stays constant. [The variable ‘monetary base’ can be considered a more stable variable.]

What if the Fed extends a $100M loan to a financial institution?

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Reserves +$100M

Loans +$100M

Loans +$100M

Reserves +$100M

Now when this bank pays it back!!!!

Bank

Fed

Assets

Liabilities

Assets

Liabilities

Reserves -$100M

Loans -$100M

Loans -$100M

Reserves -$100M

(I don’t think I need to write an explanation. I’ve got the hang of it now >0<)

☞ Conclusion: the Fed’s loans to financial institutions!!! have a 1:1 relationship with changes in the monetary base! hehe

* Other variables that cause changes in the amount of the monetary base

float: temporary changes in total reserves arising in the check clearing process

Treasury deposit at the Fed

Intervention in the foreign exchange market (we’ll learn why later^^)

Cf.) float and the Treasury deposit at the Fed complicate control of the monetary base in the short run,

but they don’t prevent the Fed from precisely controlling the monetary base.!!

● The Fed’s ability to control the monetary base

Earlier the methods of controlling the monetary base were open market operations (open market purchases, open market sales) and loans to financial institutions.

Open market operations can def!!!initely control changes in the monetary base (since the choice is with the Fed)

For loans to financial institutions, since it’s not the Fed but the financial institution that decides whether to take out a loan, it’s hard to say they can control it for sure.

The Fed merely adjusts the ‘discount rate’ (interest)!

That is, the monetary base can be split into two types: the monetary base that is controlled for sure, and the monetary base that isn’t completely controlled.

Let’s give these two different names!

All three mean the same thing hehe

Originally written in Korean on my Naver blog (2015-06). Translated to English for gdpark.blog.