Tools of Monetary Policy

Breaking down the 4 monetary policy tools the Fed uses to nail its target federal funds rate, and why it all plays out in the reserves market!

Tools of Monetary Policy (Chapter 16.) [Money & Banking, as I studied it #3]

In the previous chapter, we saw…… (the central bank FRB (Fed) releases money into the world or pulls money back in through open market operations or through loans to financial institutions……)

So now here, the question is how does it “policy”-wise adjust the money supply~~~~

Monetary policy is broadly divided into

Open market operations

Discount loan policy

Reserve requirements

Interest payments on reserves

We’re going to look at it split into these 4

What they ultimately want to do with these 4 methods is

“Adjust the interest rate to the targeted Federal fund rate (hereafter Ffr)!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!”

(Does Ffr have a huge influence on the money supply?????? huh?????)

So first let’s look at how those 4 monetary policies affect Ffr!

And then we’ll examine how Ffr going up and down affects the money supply!!!!

Now, this Ffr is determined in the reserves market, and if you don’t understand why it’s determined in the reserves market? Just keep reading!!

As you read, you’ll get it!! haha

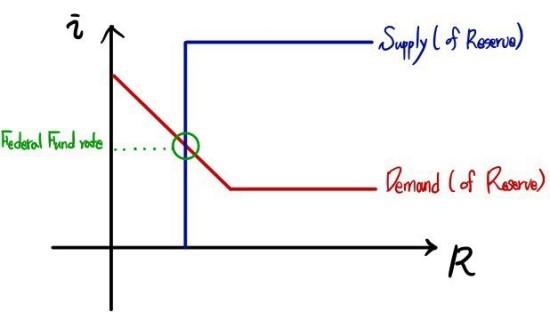

On this we’re going to draw the demand curve for reserves

and the supply curve for reserves!!

So first, let’s think about what the demand curve for reserves looks like on a coordinate plane with the basis like above!!!!

So starting with the demand curve!!!!!

Hmm, banks can borrow money from the FRB, and they can also borrow from other banks

Why???? do banks want to borrow money?!?!?!?

They might borrow to meet reserve requirements, or they borrow because they think they can lend all of it out at an interest rate higher than the interest they pay to borrow~~ haha

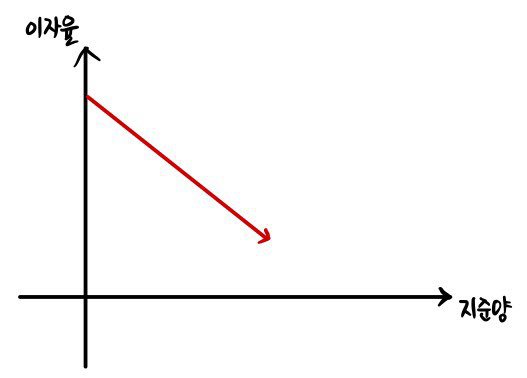

So! The lower the interest rate, the more banks say “yeah we can borrow!!! (meaning the quantity of reserves rises)”

so the graph of interest rate vs. reserves will be a downward-sloping graph on the coordinate plane

So as the interest rate drops, does the quantity of reserves keep~~ increasing

and the graph just keeps~~ plunging downward forever????

NONO!!!!!!!!

It won’t.

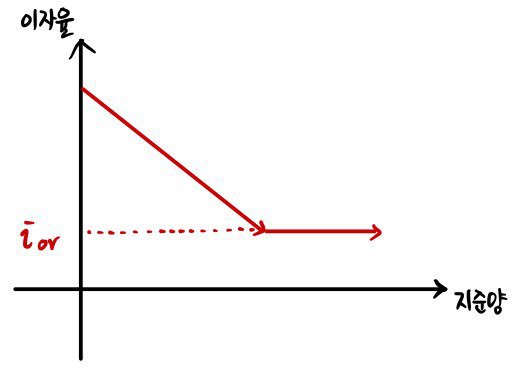

Even if banks just pile money up (in the vault), they receive interest on the reserves they’ve piled up!!!!! (

)

(???????a bit ridiculous??????but apparently this has been in effect since the ‘08 finance crisis)

So it’s correct that there’s no interest rate below that!!

That is,

the demand graph for reserves will be drawn like this!!!

Alright, now let’s look at the supply curve in the reserves market.

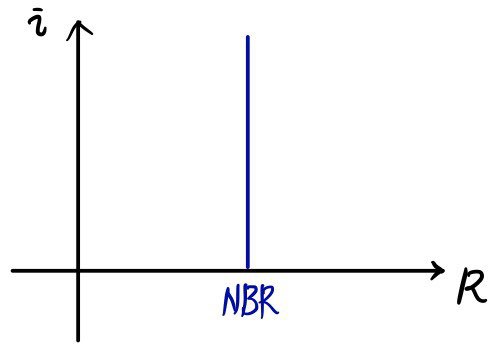

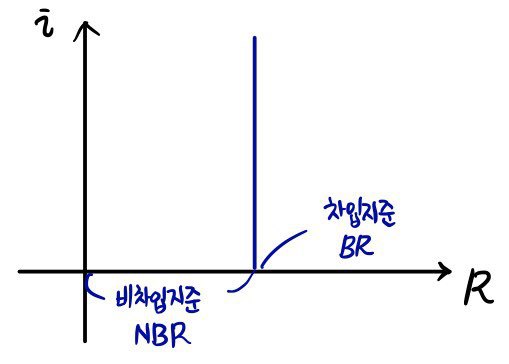

Alright, first, who supplies reserves??? Right, the Central Bank does! When they supply reserves (based on what we learned earlier), the reserves they supply could be classified into two categories!

Totally controllable reserves (Non Borrowed Reserves)

Not 100% controllable reserves (Borrowed Reserves)

Why am I bothering to bring this up!

Because on the supply curve this automatically gets categorized!!

First, let’s look at non-borrowed reserves (NBR).

From the central bank’s perspective, no matter how i changes in the market, the NBR it supplies is just “My way” — it’ll do what it decided.

From here on, the concern is this…..

At some moment, when the banks need moremoremoremoremoremoremoremore money than the money supply set by NBR,

if those banks say “Hey~ FRB~ throw us some more money~ everything we put on the open market got sold >0<”

will the FRB say “You scoundrel!!!! Step back at once!?!?!”?

no no no no no, that ain’t iiit

“Yes, customer!!~~ the interest is

and will be set as the discount rate~~~^^” is the reply, and they’ll lend more money out,

so then unexpected additional money could get released??????????????

So the supply curve graph is

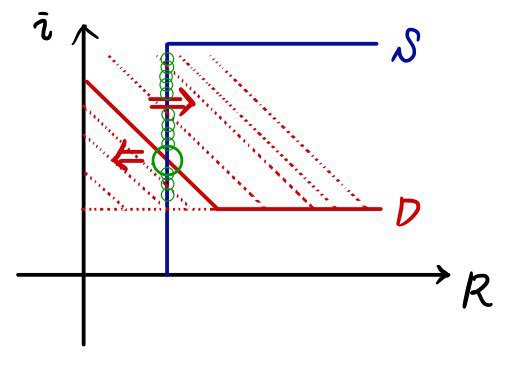

Now let’s slam the demand curve and the supply curve together!!

It ends up like this, and the gist is that ffr is determined at the equilibrium!!!!

Alright, so as we always~~~~ do in economics, let’s think about what actions cause those curves to shift!

<The point is to see how each of the 4 monetary policies mentioned earlier moves which curve and how!>

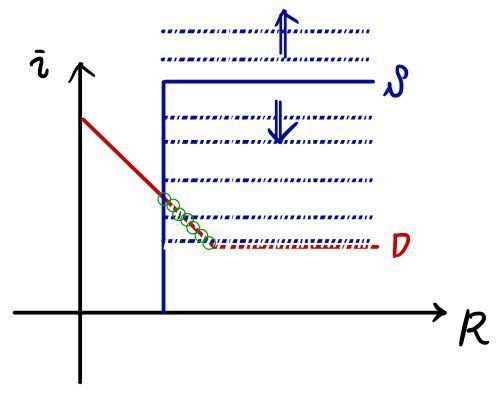

- Open market operation

Open market purchases or sales, as we learned before, mean changing NBR!! NBR changing means

the entire Supply curve moves!!

Where is the Ffr that gets determined~~~~~ if you think about it (assuming the demand curve is fixed,) it’ll be determined on the demand curve!!!!

Also, as you’ve probably already caught on, the possible range of Ffr’s movement is

in between,(no way it gets set above or below~)

Alright, so what’s the action that shifts it to the right?????? ☞ Open market purchase (direction of increasing NBR)

What’s the action that shifts it to the left??????????????? ☞ Open market sale (direction of decreasing NBR)

Therefore, open market purchases cause Ffr to fall

and open market sales cause Ffr to rise~~~~

- Changes in the discount rate (

)

The FRB has the authority to determine

, right?

Changing

should be simple, right?

The FRB isn’t an idiot, right????

The fact that it isn’t an idiot matters.

Because since they aren’t idiots, they surely won’t lower the discount rate below

0<

Okay, so the range it can move up and down is

up to this!

And another notable feature,

in a situation where

, “a change in

is not an action that will cause

to rise!”

Only in a situation where

can a change in

cause

to rise~~~ but still

will hold.. (up to a certain point)

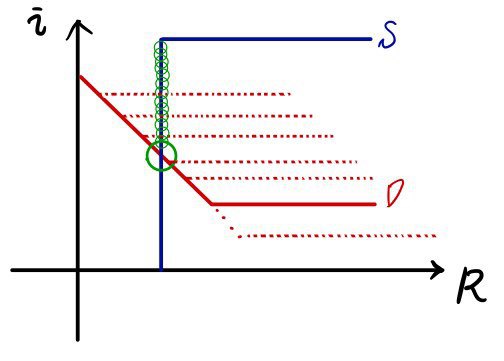

- Changes in reserve requirements

The fact that there’s a minimum reserve requirement that the central bank imposes on banks — that’s common sense??!! right… haha

Hmm~~ let’s look at what happens when this mandatory reserve requirement ratio is lowered or raised!!!

If the central bank says “Everyone raise your reserve requirement ratio!!!!!!!!

-_-+!!!!!!!!”

the banks will say “Ah F***, we’re screwed!!!!!! We have to borrow money!!!”

something like that…(was that too extreme a way to put it? haha)

This means banks now have an ‘incentive’ to borrow reserves, so it increases demand in the reserves market,

and an increase in demand means the demand curve shifts to the right!!!!!!

<Of course, the reverse situation would have the reverse result>

yeah yeah, if you look at the picture,

looking at the picture, it really is easier to understand~~><

The range over which Ffr can be moved by changing the reserve ratio is~~~

it ends up like this~~

Easy enough

Just to spout one more thing with my mouth,

raising the reserve ratio causes Ffr to rise

and lowering the reserve ratio causes Ffr to fall

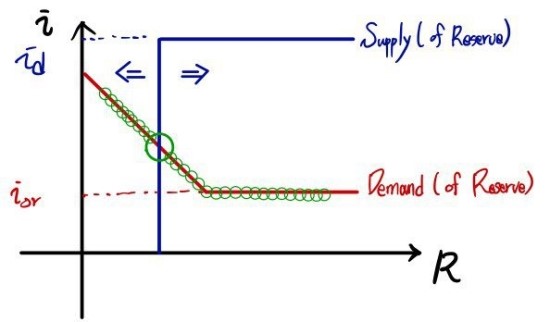

- Changes in the interest rate paid on reserves (

)

Lastly, what the central bank can arbitrarily decide:

!!

But banks piling up reserves is a kind of insurance, right??????

Insurance in preparation for a bank run situation??

“Uwaa~~T_T what do I do if people suddenly swarm in like bees wanting to withdraw money!?!?!?!??!?!” insurance against this kind of anxiety!! haha

Why should interest be given for banks stacking money for that kind of purpose? It’s not something that intuitively clicks common-sensically,

but apparently this was implemented around the time of the ‘08 financial crisis

And it actually seems to be a policy that boosts efficiency quite a bit.

First, most fundamentally, I think the biggest advantage is that it creates a range of movement for Ffr, a controllable band!

Anyway, let’s look at how changes in this

affect Ffr!

Changes in

will shift the demand curve up and down, up up up down like that

A-nyway, the important point of this Chapter is

“The FRB, by determining

and

, designates and creates the Ffr movable range

!!!!” I think!

The 4 monetary policies we’ve been looking at are called

“conventional Monetary Policy tools”

Earlier we watched how Ffr changes depending on how each tool operates through graphs, but this time let’s look at “how” they perform those actions!

- Open market operations

First, open market operations are broadly divided into two.

The open market operations that we generally know about, aiming for changes in the monetary base (MB),

and there’s also this — open market operations to offset the miscellaneous things that affect the monetary base (MB) (float, etc.)

Open market operations done with the former intent are called “dynamic open market operations,”

and those done with the latter intent are called “defensive open market operations.”

Alright, and what does the FRB buy or sell on the open market?????? just government bonds???????? to say that would lack rigor….

I want to pin it down,,, hmm,,, well there are various things,

but the most commonly used in carrying out open market operations would be more accurately called “U.S. Treasury securities.”

The reason they’re used a lot is, as we saw in Chapter 1, their liquidity is so high that the possibility of huge price swings is small,

and because liquidity is high, when you sell you can sell however you want, when you want to buy you can buy however you want!!!! That’s the reason, apparently??????

So once the FOMC (Federal Open Market Committee) sets the target Ffr and bang! bang! bang! decides,

the FRB’s open market operations trading desk in New York does the execution zip zip zip zip zip, and this isn’t done by a person,

a computer does it! A system called TRAPS (Traiding Room Automated Processing System) handles that execution lol lol lol lol

- How are discount loans done???????

The form of discount loans comes in 3 forms:

Primary credit

Secondary credit

Seasonal credit

there are these 3!!!!

As for what primary credit is, it can be used by sound banks,

and they can borrow as much as they want at an ultra-short-term (typically 1-day (overnight)) maturity!!!! that kind of thing lol lol lol

The interest rate charged here is the “discount rate,” and it’s usually set 100 basis points above the target Ffr.

Secondary credit is… something… something… for banks that are financially screwed,

and the interest rate charged on secondary credit has a penalty character of “what the hell have you been doing??????” so it’s set about 50 basis points above the discount rate.

If this weren’t set that high, all banks might drag their financial situation down to a screwed state, so the penalty character seems necessary!!!!

The 3rd one, seasonal credit… what is this? it’s a loan used by banks with seasonal patterns —

banks in resort areas, small banks in agricultural regions… those kinds of guys,

and the interest rate here, unlike the other credits, is set as the average of the Ffr and the certificate of deposit rate!!!

Hmm but this might be abolished soon? Maybe already abolished?????????????Let’s just say “there’s this~~” and move on.

Also~ among the FRB’s roles, “acting as the lender of last resort” is said to be really important,

because them acting as the lender of last resort is a really important means of overcoming a Financial Panic!!

When banks are droppin’ like flies~~~ one-by-one-by-one and no one will lend, the FRB has to supply reserves to banks to block the panic,,,

so this does,, really block it effectively~~ and it has blocked past panics well too!

But originally, apparently the FDIC (Federal Deposit Insurance Corporation) was handling that role…

So;;; is the FRB’s lender of last resort role that important?????????

—-yes yes yes

The FDIC is small in scale, so it only handles the minor stuff (?), and for really huge panics, the FRB has to do it! The FRB!

But then, if the FRB keeps stepping out and patching things up like that, banks might

“hee hee~^^* they’ll block it again anyway~~ lalala~~~”

there’s that possibility, so there are also reasons why the FRB shouldn’t step up as the lender of last resort……… haha haha haha haha

Also~~ as a role of the FRB, what to do about reserve requirements~~

The reserve ratio is a variable that affects the money multiplier, and through that, the money supply!

The FRB has had the authority to change this reserve ratio since the 1930s, and it was once a powerful tool that had a huge impact on the money supply and interest rates!!!

Now… it’s said to be a less important policy tool…

Why?

The advantages of open market operations — perfect control is possible over the scale of open market operations, and also~~ they’re quick!

Moreover, even if open market operations are mistakenly or erroneously done wrong, they can be rapidly done in the opposite direction,

and this tool also has no administrative delay so it’s just “I’m gonna do it~~”

(1 second later)

“I’m done~~~”

like this, so it’s sososososo great, apparently..

So that’s why reserve ratio changes and such aren’t really used unless necessary,

and conversely, there are of course advantages that methods other than open market operations have!!!

But since it’s not deeply related to this Chapter, it seems to have been set aside as off-topic T_T

(geez, tell us about it a bit.. T_T)

And the title of this section is “conventional monetary policy tools,” which were the tools commonly~~ mainly used before ‘08,

so going through this financial crisis, we got hit with a huge shock, and also got a lot of learning too

Back then, apparently new (?) methods that originally weren’t used were mobilized, let’s look at what those were (3 things)

- Liquidity provision

At the moment of the ‘07 financial crisis, to supply liquidity, the FRB which originally set

100 basis points above Ffr only set it 50 basis ponits above.

And in ‘08, since it wasn’t subsiding, apparently it was set only 25 basis ponts above Ffr~?

“Setting

relatively low!!!!!!!!!!(to supply liquidity!!!)”

Also at this time a new shiny new tech was the “Term Auction Facility, TAF”!!

This too was apparently implemented in the context of supplying liquidity

Because you can borrow at an interest rate lower than

!!

- Asset purchases

Hmm, another New strategy was,

in open market operations, typically short-maturity government bonds were bought, but apparently the FRB also purchased new assets!!!!! (to lower interest rates)

- Quantitative easing

Expanding the balance sheet to increase the monetary base is called quantitative easing, and the ‘08 balance sheet expansion…

Bernanke said

that it wasn’t quantitative easing, he argued it was credit easing…..;;

Credit easing “changes the composition of the FRB’s balance sheet to improve functioning in the credit market sector, so you shouldn’t call it quantitative easing!!!!!”

something like that.,,,,,,-_-,,;;that’s what he said T_T

- There’s another strategy the FRB newly used, which is a “strong commitment about future monetary policy!!”

Apparently they did that in ‘07~‘09~ by making a strong commitment to keep Ffr at 0% for an extended period,

they were able to lower the market’s expectations about future short-term interest rates, and through that lower long-term interest rates!!

So when the FRB says “ahem~,” “a certain word” being in there~ or not being in there~ and then~~ people…..haha

Anyway, taking actions to show that they’re keeping the words they uttered also becomes one method..haha?lol

So now, let’s just touch on this one thing and move on.

The reasons people are skeptical about quantitative easing!

During the ‘07~‘09 financial crisis, most of the expansion of the monetary base flowed into banks’ excess reserves and didn’t cause a large-scale increase in the money supply.

Also, at this time, since Ffr was already 0%, the expansion of the monetary base couldn’t lower Ffr any further. So it couldn’t stimulate the economy further.

Since we’ve seen the expansion of the monetary base flow into excess reserves, it’s clear that monetary base up doesn’t mean lending up!!!!

Moreover, after quantitative easing, “deflation” came…

Originally written in Korean on my Naver blog (2015-06). Translated to English for gdpark.blog.