The International Financial System

We're diving into how central banks intervene in the forex market — buying or selling foreign reserves to move the monetary base, interest rates, and ultimately the exchange rate.

If the previous chapters covered

“This is the foreign exchange market! In the foreign exchange market, the demand curves shift due to such-and-such variables (changes), and so the equilibrium exchange rate changes!~”, getting up to that point,

then this chapter is going to look at exactly “what kinds of actions” bring about changes in those variables, and how the demand curve then moves to where, and how the exchange rate then changes~

That seems to be what we’ll be looking at!

First, the central bank can intervene in the foreign exchange market,

so let’s take a look at what methods the central bank uses to intervene in the foreign exchange market

and in what direction it’s trying to move the exchange rate!

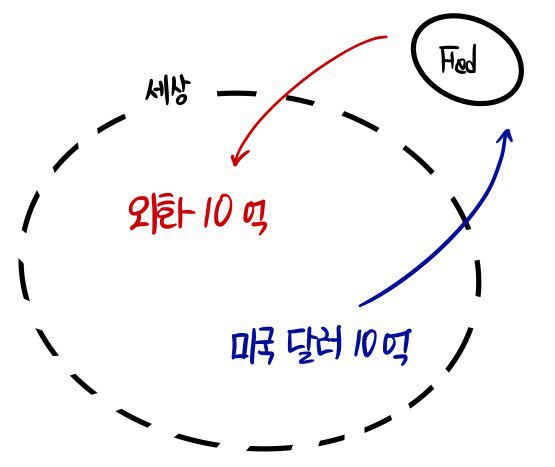

They say the central bank can influence the exchange rate of its own currency by selling or buying “international reserves (foreign reserve assets)” that they hold,

so let’s suppose the Fed sells $1 billion worth of foreign assets from its foreign reserves in order to buy $1 billion worth of U.S. currency.

(I tried interpreting the T-account like this~)

Since it means that people buy foreign currency with U.S. dollars,

mm~ first the foreign reserves ‘decrease’ by $1 billion

and the $1 billion U.S. dollars that were out in the world come to the Fed, so

MB (Monetary base) decreases by $1 billion!!!!

Now if we write this out as a T-account

Fed

Assets

Liabilities

Foreign assets -$1 billion

Currency -$1 billion

It seems to be saying that MB decreased by the same amount as the reduction in foreign reserves.

So if the Fed wanted to increase its foreign reserves, it might also buy foreign currency with U.S. dollars from people in the world.

In that case the T-account would be

Fed

Assets

Liabilities

Foreign assets +$1 billion

Currency +$1 billion

So the conclusion is that a central bank’s sale or purchase of foreign assets is no different from open-market sales or purchases of government bonds.

Selling or buying domestic currency like this to affect the monetary base and adjust foreign reserves

is called unsterilized foreign exchange intervention.

You could say “So what!!!! what am I supposed to do about it!!!!”,

but because the quantity of the monetary base determines the domestic interest rate, the quantity of the monetary base has to be handled carefully~

Okay, now let’s bring in what we learned before!

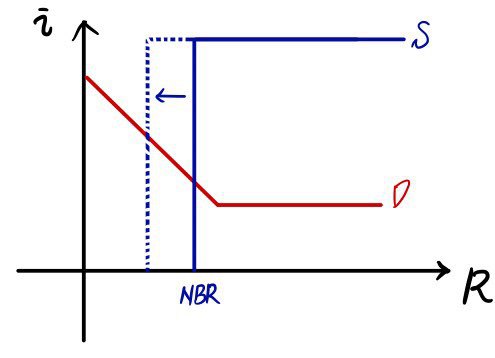

A decrease in the quantity of the monetary base would mean this picture.

Then the domestic interest rate rises.

And~ in chapter 18, we learned that a rise in the domestic interest rate means the demand curve in the foreign exchange market shifts to the right!!!!

As a result, the exchange rate rises. That is, the value of the domestic currency appreciates!

The opposite case, where foreign reserves are increased and the monetary base rises, and the effects afterwards — they’d all be the opposite of this, right!?

There may be cases where you don’t want this kind of fluctuation in domestic currency value.

Let’s think about wanting to adjust foreign reserves without affecting the monetary base (= without causing exchange rate fluctuations).

First, the situation of selling foreign currency and buying U.S. dollars to reduce foreign reserves gives the T-account

Fed

Assets

Liabilities

Foreign assets -$1 billion

Currency -$1 billion

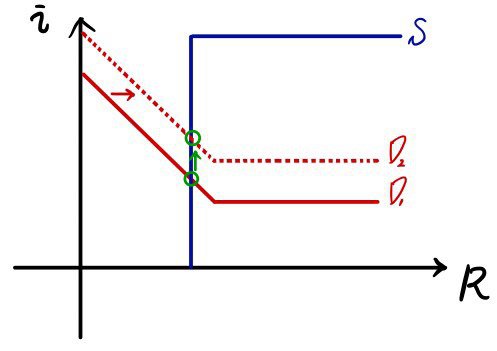

Now right here, let’s suppose the Fed immediately purchases government bonds.

When the Fed purchases government bonds, money gets sprinkled back out into the world!~

Then

Fed

Assets

Liabilities

Foreign assets -$1 billion

Government bonds +$1 billion

And like this there is no effect on the money supply at all, so there is no interest rate change due to the money supply, and therefore no exchange rate change resulting from that~

This is called sterilized foreign exchange intervention~

cf.) Sterilized foreign exchange intervention is said to produce what’s called a portfolio balance effect by changing the relative holdings of domestic and foreign securities held by the private sector.

Because of this effect, it may ultimately produce an interest rate differential and affect the exchange rate, but there is not yet evidence presented that this effect is ’large’ enough to take into account~

However, when you look at a central bank conducting sterilized foreign exchange intervention, you can see what that central bank intends and wants for the future, so you can get a signal about policy — that’s the important point!! (Well, these discussions seem to be continuously ongoing!)

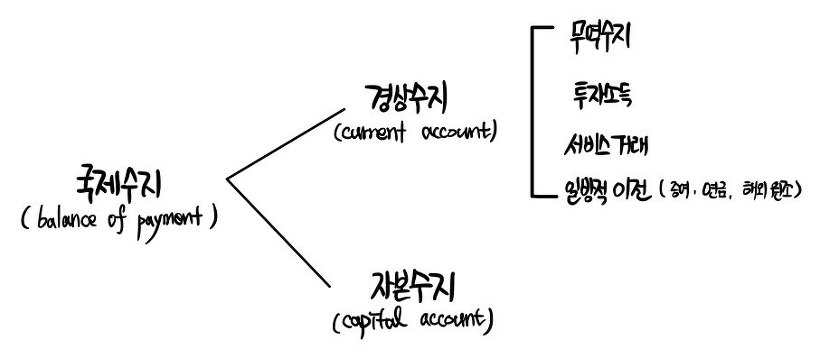

As we’ve seen above, because international financial transactions have a big impact on monetary policy, we’ve learned that we need to know the ‘measurement’ of international financial transactions very well.

So the need has arisen to know the accounting system that records everything about the movement of funds between one country and other countries — which is that measurement!!

We need to know the Balance of Payments, that’s what.

First, if we draw out the categories aggregated into the balance of payments as a tree diagram!!

If we wanted to divide further we could, and there are parts that should strictly be examined more carefully~

But our goal is to look at the main items of the balance of payments, so let’s stop around here and move on!!!

Trade balance: net receipts arising from merchandise trade

Investment income: net receipts of what was invested and income earned from the investment (not a capital transaction)

Capital account: net receipts arising from capital transactions (stocks, bonds, bank loans, etc.)

Yeah yeah, so the ‘foreign reserves…’ that we’ve been talking about since earlier —

changes in those foreign reserves are changes caused by these kinds of trade transactions,

so we very well~~ need to record them!!

Exchange rate regimes of the international financial system

Earlier we saw the effect on the exchange rate according to monetary policy,

but what I was curious about when I first started studying here was,

just as in a small market where the price moves to the equilibrium price by an invisible hand,

I thought the exchange rate was determined within some system by some invisible hand,

and I asked the professor if that was right,

and they said the exchange rate is set by people….

(If you say “by the invisible hand that person will ultimately determine the equilibrium exchange rate~”, then there’s nothing I can say back, but still this was a bit of a fresh shock to me haha)

Then by what rules that exchange rate is determined —

this time will be the time to learn those rules~

First, the exchange rate regimes of the world financial system are classified into basically 2 types~

fixed exchange rate regime

floating exchange rate regime

As the name suggests, what is fixed in the fixed exchange rate regime is that

the value of currency x is fixed to be based on another currency y!

That is, the value of currency x is relatively pegged to the value of another currency y,

and the floating exchange rate regime is allowed to fluctuate freely without being bound, without any other reference currency.

Then let’s find out when this thing called an exchange rate regime was established and what it looks like now.

To do that, let’s very briefly look at the history of exchange rates,

(It’d probably be better to read related books to know it in detail and more meaningfully~ this is too super-brief…. T_T)

Gold standard

This is a story about WWI.

Before WWI most countries adopted the gold standard, and a country’s currency could be directly converted into gold at a fixed ratio.

So it could be said to be a fixed exchange rate regime where the exchange rates between each country’s currencies were fixed,

and fixed exchange rates under the gold standard had the advantage of promoting trade by removing the uncertainty that occurs when exchange rates fluctuate,

but on the other hand, because the money supply is determined by the movement of gold between countries, it meant losing control over monetary policy,,,, so the disadvantages stood out.

And another problem was that the speed at which gold came out of gold mines and the speed of economic development were not in harmony,

so there were times when they actually experienced deflation

and times when they experienced inflation, apparently.

And one big change was right after WWII, in Bretton Woods, New Hampshire, U.S.A.

In 1944 the WWII victor nations created a certain ‘fixed exchange rate regime’ at Bretton Woods.

Its name was the Bretton Woods System,

and as this system was created, the International Monetary Fund (IMF) was established,

and the IMF was effectively given the mission of setting rules to maintain fixed exchange rates and promoting world trade by lending to countries in difficulty.

It also carries out the work of monitoring whether member countries comply with the rules set by the IMF, and it produces international economic statistical data.

And it’s not just these things that were established by the Bretton Woods negotiations.

World Bank (WB)

International Bank for Reconstruction and Develope

General Agreement on Tariff and Trade (GATT ☞ later changed to the WTO)

But the reason the Bretton Woods System is important isn’t this.

It’s that it was through this system that the U.S. became the reserve currency country.

The U.S., which went through WWI and WWII and became a super-duper-mega-ton super-rich country —

at that time well over half of the world’s manufacturing capacity was already in U.S. hands, and the U.S. also held a considerable amount of the world’s gold, so

the Bretton Woods System was built on the ‘convertibility’ of the U.S. dollar at $35 per ounce of gold.

But the time was the early 70s, and France brought thi~~is much dollars and said

“Exchange it a~~~ll for gold~~~~~”

and U.S. President Nixon at the time went “Hey lolol get lost lol we got none, buddy!!!! Screw off!!!!”

With this statement by the U.S. president, so-called Nixon Shock, the Bretton Woods System collapsed!

<Before the Nixon Shock, U.S. dollars had “Always exchangeable for gold^^*” written on them, but today’s dollars don’t~~ do~~~ that, nooope>

But the funny thing is, even after the Bretton Woods System collapsed….

the dollar didn’t…….lose its power,,,,,,, and still hasn’t…

How?!?!?!?!?! → http://gdpresent.blog.me/220599450593 go go go go go

Then how did the fixed exchange rate regime work at that time????????????????????

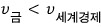

The value of the domestic currency is fixed to

(hereafter E.par),

and if the foreign interest rate rises, demand curve D will shift to the left.

Then the fixed exchange rate

becomes overvalued.

At this time, the domestic central bank ‘must’ sell foreign assets and buy its own currency to reduce foreign reserves, so as to raise the domestic interest rate.

Then the demand curve in the foreign exchange market shifts back to the right, reaching the fixed exchange rate, and it has to be aligned with the exchange rate like this.

Once again,

when it’s overvalued, the central bank has to sell foreign currency and buy domestic currency to fix the exchange rate,

and conversely,

when it’s undervalued, it has to buy foreign currency and sell domestic currency to fix the exchange rate!

But what if

is overvalued, and it keeps selling foreign currency

and keeps buying domestic currency and despite all that

there’s no sign of aligning, and keeps,,,, not aligning,,,,

and despite still continuing, the foreign currency to sell runs out …….then what???

At this time, devaluation must take place!!

In other words,

has no choice but to be reset downward…

Conversely,

is undervalued, so that country should buy foreign currency and sell domestic currency,

but rather than that method,

there’s also the method of resetting by revaluing

upward!

Ri~~ght, this was the problem.

Mm, so the exchange rate (

) could only be changed when experiencing continuous large-scale deficits or surpluses in the balance of payments,

and how large a surplus or deficit did it have to be,,, when it couldn’t be resolved within the limit that the IMF could lend….

So the IMF could pressure deficit countries to devalue their currency or pursue contractionary policies,

but it couldn’t pressure surplus countries to revalue their exchange rate to a higher level or to pursue expansionary policies..

Well anyway, now that the Bretton Woods System has gone bust, how are they doing it????????

The answer to that is ‘managed float regime’, which says “Mm~ it’s a mix of the fixed exchange rate regime and the floating exchange rate regime^^*”… haha

The reason we say it’s a mix of the two methods is because we don’t want the exchange rate to fluctuate greatly, but we allow it to be able to fluctuate daily in response to current market conditions!!!! so we can say that?~ haha

<The book doesn’t cover more detailed content… I’m curious though… haha>

Okay, so what is the IMF now?

Originally under the Bretton Woods System, the IMF’s goal was to resolve balance of payments problems among member countries and to lend to countries with balance of payments deficits,

’to fix fixed exchange rates’,

but in 1971 the Bretton Woods System collapsed~~ and the promise to set exchange rates as fixed was broken, so then has the IMF disappeared????

From what you see here and there in newspapers and news reports, it hasn’t disappeared… so has what it does changed???

They say the IMF’s main role has indeed changed since 1971.

It continues data collection and statistical compilation work as usual, but doesn’t do lending work to promote fixed exchange rates,

and “The IMF does lending that helps countries facing crisis recover from financial crises, and prevents financial crises from spreading”

that’s the kind of work it does <just like the FRB’s lender-of-last-resort role!>

The issues raised about the IMF acting as the lender of last resort are exactly the sa~~me as the issues raised about the Fed acting as the lender of last resort (they have to be)

““It’s~~ okay~~ the IMF will lend money~~~”

like when we listed the problems with the Fed’s lender-of-last-resort role earlier,

‘adverse selection’ and ‘moral hazard’ can be listed as problems,

but if not the IMF, what country, what bank could prevent another country’s financial crisis T_T

but if they don’t prevent it, everyone could be screwed together???

Sigh… no answer this way, no answer that way… just hardcore no-answer….haha

There was a time when this problem was really visible.

When Russia’s financial condition was bad, the IMF demanded appropriate financial reforms, but Russia didn’t follow them…

But the IMF still lent money to Russia anyway.. (some IMF critics’ criticism)

While they did that for Russia, on the other hand they forced Asian countries into an austerity program focused on strict macroeconomic policies…

Sigh… really damn makes me cry.. T_T T_T T_T our country was one of the victims too…T_T

Another problem to list for the IMF is that the lender role isn’t immediate!!!!

Because it contrasts with the Fed, which swoosh-swoosh-swoosh loans within 1 day, it’s different from the advantages of the Fed’s lender-of-last-resort role..!?

Also, one method for preventing large fluctuations in the exchange rate —

“Hey, block the money from leaving -_-”

is fixed, while on the other hand the foreign country’s interest rate has risen and the domestic currency is about to leak out to foreign countries, let’s suppose.

You have to raise the domestic interest rate through foreign currency sales and domestic currency purchases, but there’s no foreign exchange to sell…. T_T

At the end of ‘98, Malaysia’s Prime Minister Mahathir said that

‘Hey, block the money from leaving -_-’ (sorry for the historical distortion)

But the result was apparently pretty okay????

But if you look at Mishkin’s listed disadvantages of “capital controls”

- According to practical evidence, capital outflow controls are never effective during the progress of a crisis.

Because money that’s going to leave will leave by some method.

- Money leaves when it’s going to leave, and all that does is lose trust in the government.

It only makes even money that wouldn’t have left, leave because of the lost trust.

- Capital controls only end up producing corruption.

They’ll clearly help money go out and get rewarded for it.

So is that how Mishkin interprets that Malaysia made a bad choice?????????????????

No, I mean -- I don’t know if this book is an argument piece or an explanation piece, going back and forth like this continuously really -- ugh frustrating

-#talking to myself, #venting

Originally written in Korean on my Naver blog (2015-06). Translated to English for gdpark.blog.