Quantity Theory of Money, Inflation, and Money Demand — Keynes and Liquidity Preference Theory

From Irving Fisher's velocity of money to Keynes's Liquidity Preference Theory — a casual breakdown of how money supply, interest rates, and GDP all connect.

We have been learning about money supply,

how the supply is conducted, and how supplying like this and that leads to this and that,

and! money supply has an effect on the exchange rate,

so when supplying money, not only the interest rate should be watched,

but the exchange rate should also be watched while supplying~~

that seems to be the conclusion we’ve reached up to this point.

Now, this time, from yet another perspective,

it seems it will be a time to look at money and monetary policy.

Another field of economics for researching money and monetary policy,

Monetary Theory, is what we’ll be looking at~~nn

So in order, let’s dive into the classical school’s monetary theory.

That’s right, the Quantity Theory of Money!

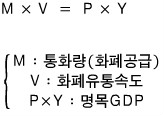

In the 19th–early 20th century, Classical economists developed something called the “Quantity Theory of Money” to study how the size of nominal GDP is determined, they say.

The Quantity Theory of Money is said to be best explained in the 1911 book ‘The Purchasing Power of Money’ by the American economist Irving Fisher~

He’s said to have explained it like this

Fisher’s contribution is said to be that V (velocity of money) right there~

“(Over the course of a year) The average number of transactions showing how many times on average money was used to purchase all the goods and services produced in that economy (called the turnover rate)”

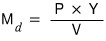

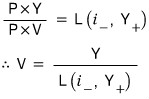

Anyway, the meaning of the equation above is that just because money supply M is high↑, nominal GDP (=P×Y) is not necessarily high.

“You have to know V!”

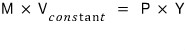

So we have to find out about the velocity V, and Fisher himself thought that velocity is determined by “individuals’ transaction customs” or “related institutions,”

so he thought those determining variables wouldn’t change drastically in the short run.

So he thought V is constant?

Alright, so “in the short run, V is constant. That is, let’s treat V as a constant” (a commitment to looking at the short run)

That is, here

this means that nominal GDP depends on (in the short run) the money quantity (money supply).

And one more assumption

※\assumption-ism※

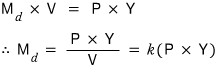

Let’s assume “supply and demand are in equilibrium in the money market.”

That assumption means

and if we substitute this into the Equation above

And so the conclusion is

in Fisher’s Quantity Theory of Money, ‘money demand’ is determined by national income (=GDP)

and what we should pay attention to here is

“it’s unrelated to the interest rate” (in the short run)

Let me add one more and more and more and more and more and more and more assumption

※\assumption-ism※

As an assumption of the classical school, they assumed “wages and prices are pureh-fectly flexible.”

Since wages and prices are perfectly flexible, real GDP Y stays at the full employment level

and Y can be viewed as a constant in the short run, so this conclusion could also be drawn.

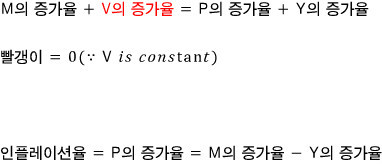

Price level P and money quantity M are (in the short run) in a proportional relationship.

So for the Inflation Fisher saw, let’s drop all the assumptions we built up coming down, and only keep V as constant.

so the above equation becomes

That is, the inflation rate as Fisher saw it is

money growth rate − real GDP growth rate (economic growth rate)

that’s exactly the inflation rate, so he viewed it~ ><

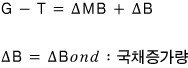

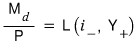

According to classical monetary theory, the money supply rate and the inflation rate are in a (+) directional relationship like that, and if we use that relationship to interpret the ‘fiscal deficit’

G is what was spent, T is what was collected!!!!

But if there’s something the government has to spend and it can’t be covered by the T that was collected, it could issue government bonds and spend G.

Or well, it could just print money~

That is

(If everything is solved by the T that was collected

right??)

Now, to talk about what this means,

‘A fiscal deficit brings about an increase in MB~ and therefore creates inflation!!’

In a word, “a continuous fiscal deficit creates a continuous inflation rate!”

Alright, now let’s leave the classical school! hahahaha

My favorite man, John Maynard Keynes, is about to appear!!!

Coming along like Fisher, there was one big change, in John M. Keynes’s

“The General Theory of Employment, Interest, and Money”

(it’s apparently counted as a mega-difficult book?)

where our guy Mr. Keynes discarded the view from the existing theory that the vel-ocity-of-sir-culation is constant

and he’s said to have said “no no, money demand is going to be related to the interest rate, it’s going to be related….heh”

In Keynes’s theory of money demand, the “liquidity preference theory”

proposes 3 motives behind money demand.

transactions motive

precautionary motive

speculative motive

These 3!

The transactions motive is the view that “payment technology” affects money demand.

He said that as technology advances, money demand will decrease relative to national income,

and the precautionary motive refers to “people hold money to prepare for unexpected expenditures~”

Of course, precautionary money demand is proportional to national income~

and the speculative motive says “people hold money as a means of wealth accumulation~”!

This one is related to the interest rate. If the interest rate is high, who would want to accumulate cash!!

(Keynes’s definition of money: cash is 0% interest rate)

That is, if the nominal interest rate i rises, speculative money demand decreases, is what he’s saying!

<Other Keynesian economists (Tobin, etc.) are said to have explained that the transactions motive and precautionary motive are also in a negative relationship with the interest rate i>

All three move in the opposite direction from the interest rate i~haha

Combining the 3 motives to make a ‘money demand function’, it was

named the “liquidity preference function”!!

he defined it like this~

According to the classical school

so,

Keynes is saying that because the fluctuations in the interest rate are large, the fluctuations in velocity V are also large!!!haha

Also related to Keynes’s theory of money demand,

there’s “The Theory of Portfolio selection”

and the reason it’s mentioned here is

because this is research on “how much money will people hold as a part of their total assets~~~”

on that!!

So what does that research say? Well,

it lets us mention a few more other variables that affect money demand.

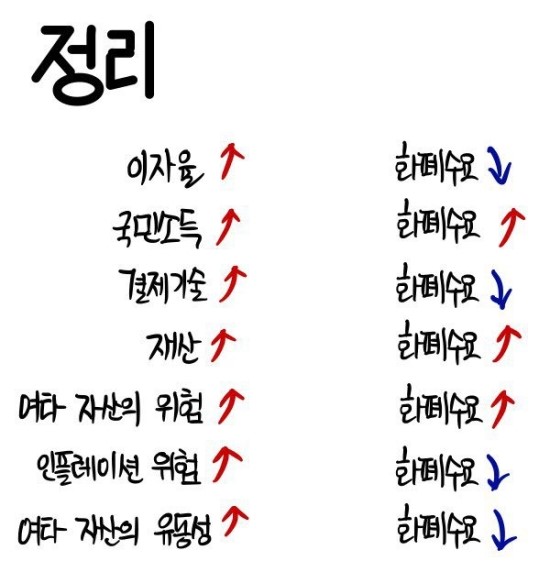

Since income and wealth move in the same direction, we can say that wealth and money demand are proportional!!

Also, for instance, when the stock market fluctuates a lot, or when risk increases in other markets,

money demand will naturally increase,

that is, the risk of other assets and money demand are proportional!

- If signs of inflation risk appear domestically, the real value of money will fall~~

this means money demand will fall~

(rather than money, people would go to real assets like gold or oil, right?) so it’s inversely proportional to inflation risk.

- If the liquidity of other assets increases (MMF, home mortgages, credit extensions, etc.), money demand will decrease.

Originally written in Korean on my Naver blog (2015-06). Translated to English for gdpark.blog.